After two years of recession, the worst may be over for Russia's economy, but not for its leaders. As the year approaches its final quarter, the Russian government is still trying to finalize its 2016 federal budget. Though the budget has long been a point of contention in the Kremlin, this year's budget battle has been especially divisive amid dwindling funds and disappearing options for spending cuts. To make matters worse, just weeks before September's parliamentary elections — a bellwether for the ruling United Russia party ahead of the 2018 presidential vote — Russians are protesting their economic straits in droves. Facing an unhappy public and a $31 billion shortfall in the current budget drafts, Prime Minister Dmitri Medvedev has been given a tall order: plug the gaping hole in the budget while also allowing for billions more in social spending.

A Slow Recovery

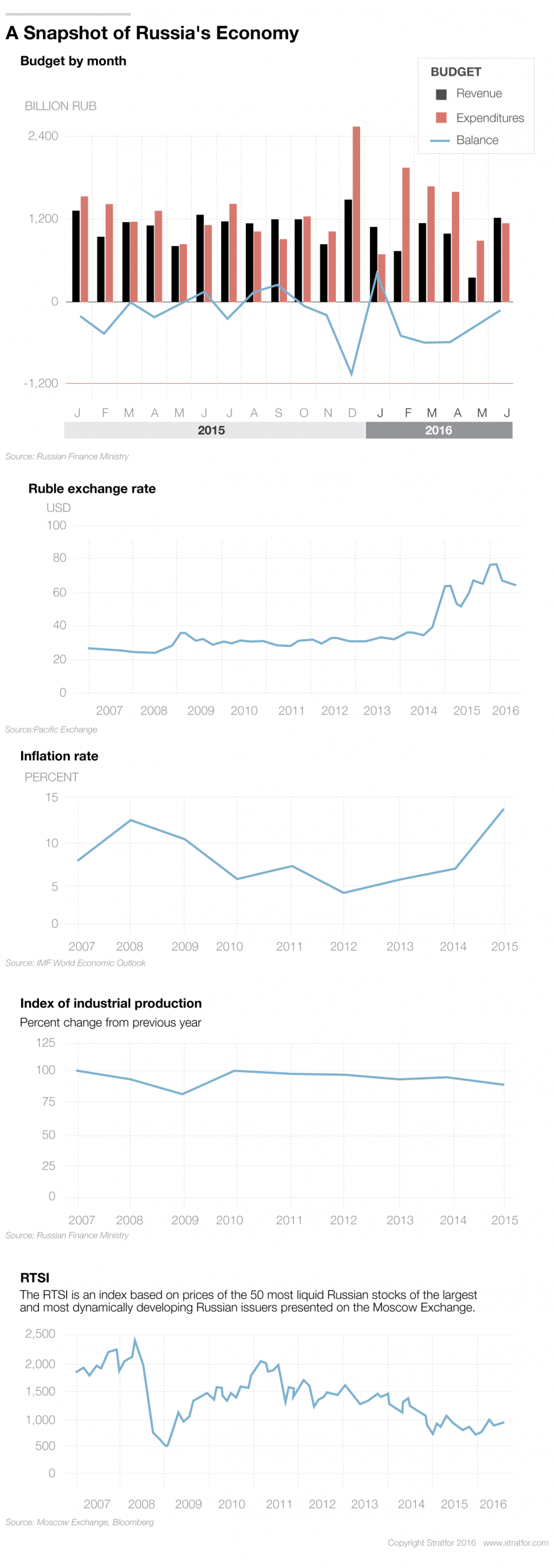

Despite the Kremlin's trouble, the Russian economy has started to show small signs of recovery this year, contracting at a slower rate since January. In June, the Central Bank of Russia described the economy as stable, and inflation has dropped from 13.4 percent in 2015 (a 15-year high) to 7 percent today. The ruble is also regaining its strength, rising 14 percent against the dollar this year. At the same time, the currency remains low enough to create a competitive exchange rate, a boon for agricultural, pharmaceutical and petrochemical industries. After two years of shrinking, industrial production may actually resume growth by the end of the year. Russian credit organizations, meanwhile, posted their first net profit ($460 billion) in two years, and during the week of Aug. 15, Russian stocks traded at their highest point in history.

Russia's citizens, however, are not faring as well. Over the past year, the average Russian's monthly wage fell 9.5 percent, slipping below $450 dollars — less than in China, Serbia and Romania. According to state statistics, 50 percent of that income goes toward food, a figure on par with many African countries. What's more, 13.4 percent of all Russians now live below the poverty line ($139 a month), a proportion that is expected to grow at its fastest rate since the 1998 economic crisis.

Easing Social Tension

Many Russians are fed up with the situation and with the government's handling of it. In a rare unscripted moment in May, a crowd of poor retirees confronted Medvedev, yelling, "You're wiping your feet on us." The prime minister responded by explaining that the country's finances were tight and by wishing the retirees well. Since retirees make up one-third of the Russian population — and since most of the remaining two-thirds have family members in the system — the pension system has become a flashpoint in Russian politics. In 1998, when then-President Boris Yeltsin cut pensions to muddle through a financial crisis, retirees and their family members staged a multigenerational mass protest against the government. Medvedev's response similarly fueled protests across the country, leaving the government to look for ways to ease public discontent ahead of September's elections. The upcoming vote will serve as a litmus test for the long-standing United Russia government, determining whether President Vladimir Putin will stand for a fourth term in office in 2018.

To appease the angry pensioners, the government will discuss whether to index pensions by 8.6 percent or to make an immediate, one-time payment to retirees. Either way, this year's budget draft does not include leeway for heightened social spending (indexing would add some $2.2 billion to the budget and increase the base for future indexing). Having cut spending across all sectors and ministries by 10 percent this year, the government is still $31 billion shy of hitting its target of a 3 percent budget deficit — the first deficit since Putin came to power. Because the new parliament must vote on the budget within 30 days of the Sept. 18 elections, time is running out for the Kremlin to suss out its budgetary problems. Medvedev has his work cut out for him.

Falling Short

Initially, the prime minister tried to cut the country's massive defense spending, since nearly every other ministry is already running on bare bones. At a June 28 meeting of the Cabinet, president and Military-Industrial Commission, Medvedev and Finance Minister Anton Siluanov called for slashing the country's arms procurement program. An argument ensued when Defense Minister Sergei Shoigu and Vice Premier Dmitri Rogozin countered that the program's funding should be doubled to 24 trillion rubles ($368 billion) instead. After another week of haggling, the parties compromised. Medvedev announced July 7 that spending for six of the program's sectors would stay the same, while the rest would be cut. Even so, as Putin continues to push for increased defense spending, the struggle is probably far from over.

With nothing much left to cut, the Kremlin has turned instead to fundraising. In late July, Putin held a meeting with 30 of the country's wealthiest oligarchs and silovarchs in Sochi. Though the Kremlin downplayed the meeting, Russian media revealed that Putin pressed the wealthy businessmen to donate funds to various projects around Russia, something he has done twice before in times of economic need. During the 2008-09 financial crisis, Russia's wealthy elite pumped large sums of cash directly into the financial system; in 2014, the Kremlin persuaded them to finance construction for the Winter Olympics in Sochi. Now, Putin has entreated the billionaires to fund projects across the country — from schools to infrastructure — in his government's stead. Unlike in the previous incidents, it is not clear this time how much the oligarchs and silovarchs can afford to fork over. But Putin has already demonstrated that he is not afraid to topple the country's elite for noncompliance.

Another focus of the Kremlin's fundraising efforts is the drive to privatize state assets. In July, the government raked in $813 million for a 10.9 percent float of shares in its diamond company, Alrosa. Next, the Kremlin planned to privatize 50 percent of Bashneft, Russia's sixth-largest oil firm, to the tune of $4.6 billion, but a political scuffle derailed the project. Putin barred Rosneft chief Igor Sechin — arguably Russia's second-most powerful man — from bidding on the stake, which would have expanded the power base of Rosneft and its leader even further. When Rosneft disregarded Putin's orders, the Kremlin shelved all Bashneft privatization plans until 2017, at the expense of the budget.

The feud could also complicate the Kremlin's plans to privatize 19.7 percent of Rosneft (against Sechin's wishes) before the end of the year. Regardless of whether Putin and Sechin can come to terms over the deal, the government has recently moved forward with plans for the $11.4 billion sale. Still, the transaction may not come through in time to help the Kremlin meet its budgetary needs: On Aug. 8, the front-running buyer, the China National Petroleum Corp., said it had not received any proposals.

A Last Resort

This leaves one other option for filling the budget gap: reserve funds. The state holds $38 billion in its Reserve Fund, enough to cover the budget deficit even with the surge in social spending. To weather the recession, the government has already had to draw on that fund, burning through half of it since the start of 2015. The remaining $38 billion, however, was earmarked for emergency spending and stimulus in 2017. If the government uses the money to patch up this year's budget, next year's financial situation will be even more uncertain, and the 2017 budget battle more contentious. Although Russia has an additional $72 billion in another account, the National Welfare Fund, that money is intended for use only in the pension system or in case of a government emergency. Since Putin came to power, the Kremlin has tapped the fund just once, to keep the pension system afloat (and the financial crisis under wraps) in 2008-09. Considering the discontent already rampant among retirees and the parliamentary elections' swift approach, Moscow will be reluctant to dip back into the fund.

Furthermore, the reserve funds would offer a stopgap solution at best. Putin's most trusted economic adviser, Alexei Kudrin, believes both funds will be drained by the end of 2017. Though Kudrin is working on a plan for structural reform that could stimulate economic growth by 4 percent annually by 2018, it would likely involve large spending cuts to defense and other highly politicized sectors. On the other hand, he has warned that if the Kremlin does not adopt his plan next year, then its only option will be to raise taxes and increase the pension age — both disastrous moves in an election season. Kudrin's proposal highlights a larger problem facing the Kremlin: The government has many options for bridging its budget gap, but each comes with a cost.