A combination of elevated global interest rates and increasing economic risk, especially outside the United States, will leave vulnerable, low-income economies at heightened risk of distress, although high-income emerging economies will be more protected. Following the 2008 global financial crisis, emerging and developing economies attracted significant private capital inflows amid low global interest rates. China also provided significant capital, particularly to low-income and lower-middle-income countries. However, the global monetary tightening cycle began raising debt servicing costs in subsequent years, increasing the financial burdens on vulnerable economies. While the beginning of the COVID-19 crisis in 2020 cut this tightening cycle short, the pandemic's economic shock pushed several mostly low-income countries into severe financial distress and even default. In addition, the United States' rapid post-COVID-19 recovery led to a substantial spike in global interest rates and a stronger dollar, which further weakened many low-income countries' financial positions. As a result, many lower-income countries are and will remain under financial pressure amid increased global economic uncertainty. Meanwhile, emerging markets, faced with the same macro backdrop, will avoid systemic financial instability despite the continued increase in government debt and economic uncertainty over the next 12-24 months.

- In the past five years, Argentina, Belarus, Belize, Ecuador, Ghana, Lebanon, Sri Lanka, Russia, Ukraine and Zambia have defaulted on and/or were forced to restructure their sovereign international debt. Other countries, such as Pakistan, have only managed to avoid a default because they received support from the International Monetary Fund.

- The amount of debt that low-income countries owe to commercial creditors is not large enough to become a source of broader global financial distress as it did in the 1980s and, less so, in the late 1990s. According to the Bank of England's Sovereign Default Database, 10 countries account for 75% of the U.S. dollar value of debt currently in default globally (mainly Russia and Venezuela). Emerging economies owe most of the commercial debt in default, as opposed to developing, low-income economies. The level of global public debt in default has averaged between 0.3% and 0.6% over the past decade and currently stands at 0.5%.

The United States' recent shift in economic policy and China's uncertain economic outlook will further challenge highly indebted, low-income countries, increasing economic and political risks. The administration of U.S. President Donald Trump looks set to pursue an inflationary and expansionary macroeconomic and trade policy, which will raise U.S. interest rates and strengthen the dollar, making it more onerous for low-income countries to service their debt. Meanwhile, China's move away from real estate- and infrastructure-intensive growth will lower Chinese demand for commodities, reducing prices on which commodity-exporting, low-income countries rely for revenue. China's uncertain economic outlook amid competition with the United States is also reducing Beijing's willingness to provide financing to low-income countries, which will further hurt their economic and financial outlook. These financial conditions mean that low-income countries at a heightened risk of debt distress will likely face increasing domestic political instability in 2025, regardless of whether they implement significant policy adjustments or default on their debt. On one hand, policy adjustments in the form of a tighter monetary policy, currency devaluation and fiscal adjustment (including subsidy cuts) tend to be deeply unpopular against the backdrop of weak economic growth and high inflation. On the other hand, an external debt default is typically even more economically and politically destabilizing, as it sharply limits a country's access to external financing (including long-term investment) and forces a precipitous contraction of imports.

- U.S. interest rates will decline only very modestly, if at all, in 2025, meaning international borrowing costs for developing and emerging economies will remain elevated.

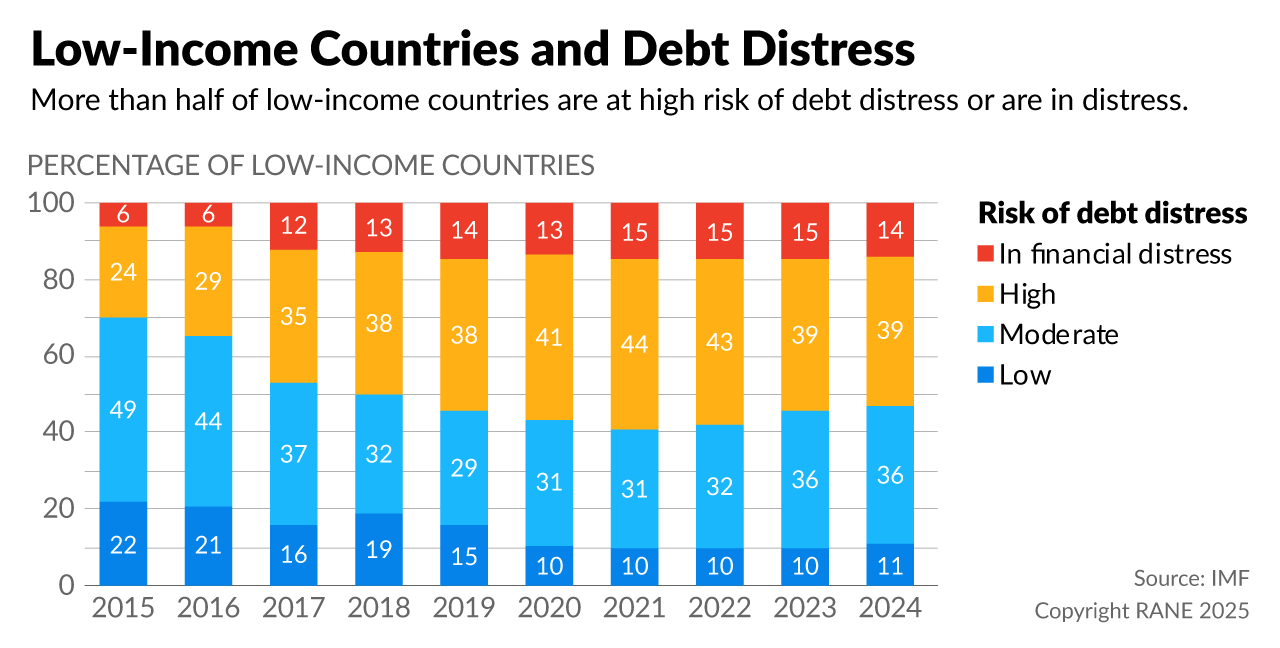

- About 14% of the world's low-income countries are in debt distress, and an additional 39% are at high risk of debt distress. While some of these low-income countries are undergoing IMF-supervised policy changes and/or have emerged from a debt restructuring, risks remain elevated, particularly given the worsening global macro environment.

- The IMF estimates that 50% of developing economies (including countries already in distress) are at high risk of facing ''default-like'' spreads on their sovereign debt, severely curtailing their ability to raise (or refinance) international debt.

- Ghana, Sri Lanka and Zambia have restructured their debt and continue to make progress on broader economic adjustment with a fair prospect of regaining market access at the end of their IMF programs.

By comparison, emerging economies have generally solid economic fundamentals and sufficiently flexible policy regimes to limit the risk of severe distress. Emerging economies typically have lower dollar-denominated debt, flexible exchange rates and more independent central banks. They also often benefit from a larger domestic investor base and stronger institutions. These advantages will help emerging economies survive the current adverse global macro environment despite disadvantageous policies from the United States and China. Among emerging markets, Argentina, Ecuador and Pakistan face more significant financial challenges. But they also stand to benefit from IMF support, which means that if they follow IMF-prescribed policies in the context of an IMF program, they should be able to avoid another round of severe financial distress. While countries like Brazil, Mexico, South Africa and Turkey will encounter tougher financial conditions, they are unlikely to face sovereign distress or external payment defaults in the coming years. As a result, these countries will have fewer economic triggers for political instability.

- Argentina, Ukraine, Egypt, Ecuador and Pakistan are the largest recipients of IMF loans, largely on account of their economic size.