A worker moves soil containing rare earth minerals at a port in China.

Editor’s Note: This is part of an occasional series exploring the geopolitical implications of climate change. Part one explored how the radical physical transformation of the Arctic is altering Russia’s strategic perceptions and realities. In this analysis, we explore how climate change is also altering the perceived relative significance of certain geographic areas by shifting demand for critical natural resources.

Not all strategic implications of climate change are driven by immediate physical impacts. Political and social responses to future risks are also driving the acceleration of research and development of alternative energy systems. And these, in turn, are influenced by economic and technological factors that enable or constrain future deployment. In the race to reduce dependence on carbon-producing fossil fuels as the primary energy source, a specific set of minerals are emerging as the key determinants of success. And like oil and gas, viable deposits of these new energy minerals are not evenly distributed across the globe.

The Historic Role of Resources

Great power competition has long centered on critical resources and routes, whether they be spices from the East, silver and gold from the New World, or oil from the Middle East. Changing perceptions of the value of particular commodities, often shaped by technological developments, fundamentally alter the perceived value of place, at least in the sense of power competition. Resource-rich areas fought over in one generation may be backwaters in the next.

The Arabian Peninsula and the modern Middle East played a shifting role in the Silk Road linking China to Europe from the first through 14th centuries. The expansion of European maritime routes in the 16th century, facilitated by combining technologies to allow regular long-distance sailing, bypassed many of the land links and the earlier Arab-dominated maritime links, undercutting the region’s role as a transit route. In the early 20th century, the discovery of oil and the rapid expansion of internal combustion engines brought new significance to the Middle East, transforming the wealth and influence of Saudi Arabia and other countries on the Arabian Peninsula. But as the world looks to transition away from hydrocarbons, Arab Gulf governments are now scrambling to redefine their economic basis and significance — recognizing that their dependence on oil revenues may not last.

While this may appear to be a Euro-centric or U.S.-centric view of “significance,” the strategic issue is not the value of a space to the people who live there, but the perceived value that drives a more global pattern of competition and cooperation. Whether we like it or not, wars are fought over critical resources or the routes to the resources, and even in the more “enlightened” modern times, economic and political warfare remains a common tool to secure necessary resources and markets. The acceptance of traditional imperialistic patterns may be gone, but the desire of nations to ensure their own economic future has not faded.

The Next Race Takes Shape

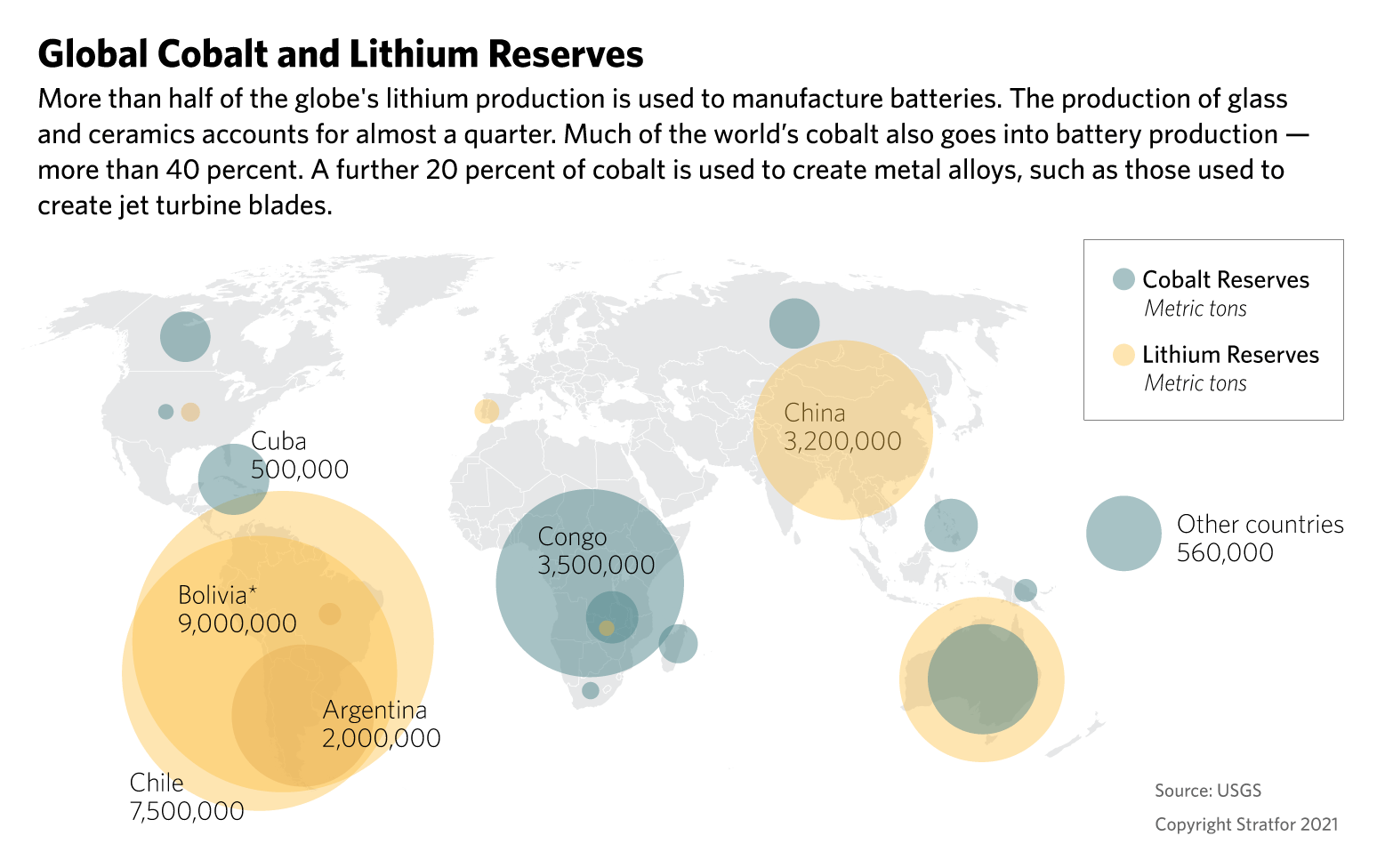

New energy forms do not eliminate the old — we still use coal, water and wind, for example. But they do open new areas to competition, as resources are unevenly spread across the planet. In the place of oil or natural gas, demand is steadily increasing for lithium, cobalt, manganese, nickel and graphite, as well as several rare earth elements (REEs) — all of which are critical minerals for electric vehicles and batteries, wind and solar power generation, and electricity transmission. Further electrification of transportation infrastructure and connectivity of expanded grids also requires a lot more copper. While these minerals may be found around the world, there are key concentrations in South America, Africa and Australia, as well as potentials in the deep sea and Arctic.

Australia is a key producer of lithium and nickel, but there is increasing investment in lithium extraction and refining in South America, where Argentina, Bolivia and Chile account for more than half of the global lithium reserves. This places Latin America once again as a critical geographic region for resource competition. As China expands its investments in South America, the United States is likely to see risks of attendant political influence, a challenge to the still active tenets of the Monroe Doctrine. The United States, after years of general neglect of its southern neighbors, is once again awakening to both the economic potential of greater engagement in South and Central America, and the growing risk of Chinese involvement in the U.S. backyard. Rising strategic competition poses risks to Latin American countries, including exploitation, foreign interference and the exacerbation of intra-regional disputes. But it also presents an opportunity to play the great powers against one another for local political and economic gain.

Similar patterns are likely to emerge in Africa and in parts of Southeast Asia, as well as non-traditional geographies including the Arctic, the deep sea and eventually even space. The melting Arctic ice not only opens new routes, but also provides greater access to resources. While Russia has a head start, China has also expanded its Arctic diplomacy, exploration and investments. Economic and strategic frictions will converge in places like Greenland and Scandinavia, and along the Russian Arctic frontier, though the latter is more likely to involve China and Russia instead of China and the West. China, Japan and other nations have already begun exploring the ocean floors for economically viable concentrations of polymetallic nodules (a source of strategic minerals) and methane hydrate (an alternative energy source). And where explorers go, competing maritime claims and naval presence often follow.

China’s Dominance

But the location of the minerals in the ground is only one piece of the strategic puzzle. The other is processing capacity. China holds a dominant role in the global supply chain of lithium-ion (or Li-ion) batteries that will power electric vehicles (EVs) around the globe. According to the BloombergNEF 2020 ranking of the global Li-Ion supply chain, China maintains 80% global raw material refining capacity for critical battery minerals. China’s large domestic consumer base and government-mandated push toward EVs, combined with its developed automotive industry, position Beijing to set the standards for future EV battery design and licensing, and remain critical to international manufacturing supply chains. This dominance helps Beijing take advantage of Western countries’ climate change initiatives, at least in the near term, to try and delay or discourage any form of economic decoupling that could leave China isolated from major international markets.

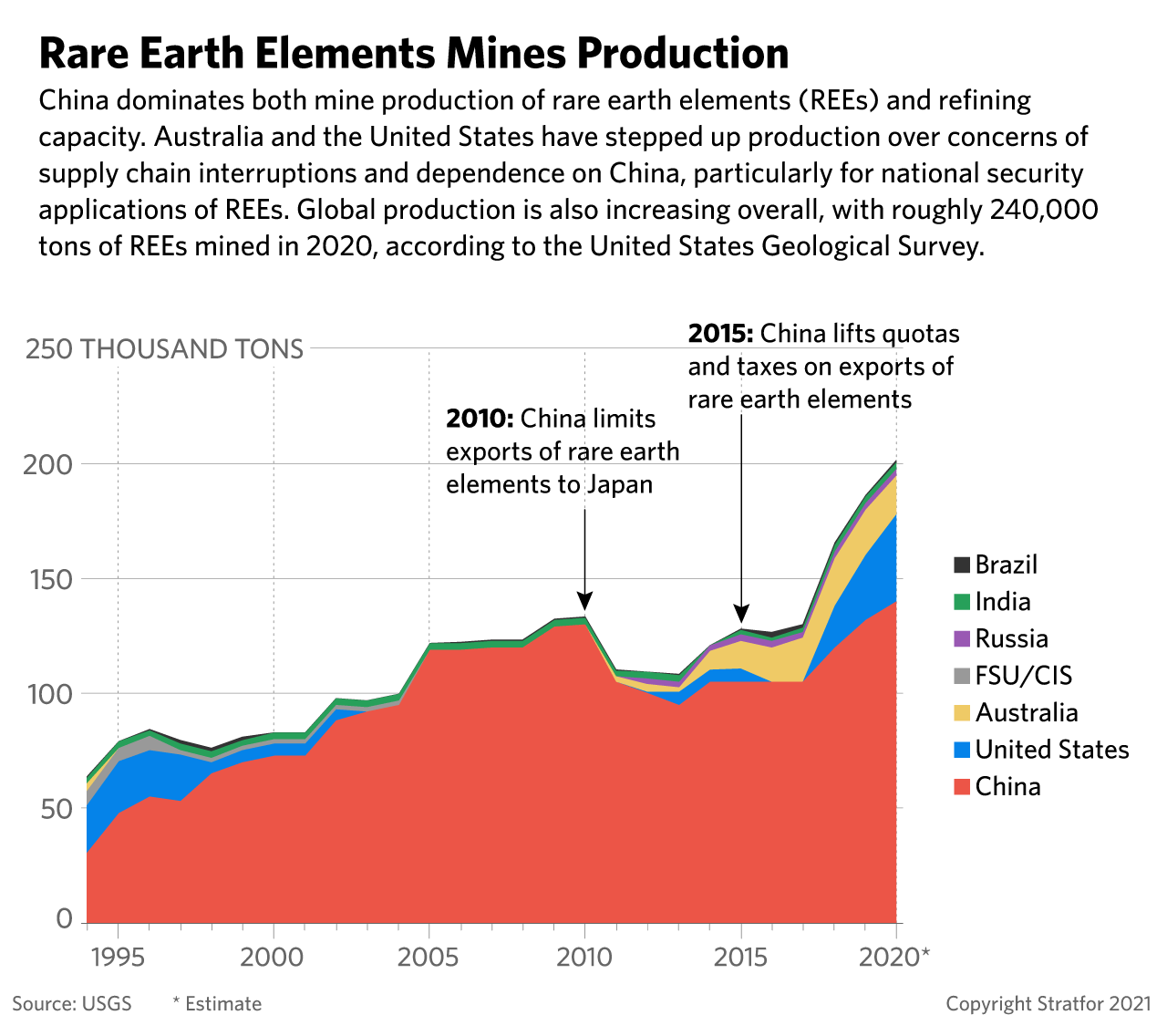

China’s preponderance of refining capacity is driving other countries to counter their own dependence on China. Australia, for example, has ramped up domestic production of REEs since China limited exports of those elements to Japan in 2010. However, Australia remains a small amount of global REE production compared with China. According to the United States Geological Survey, Australian mines produced some 17,000 tons of REEs in 2020, trailing 38,000 tons from the United States and 30,000 tons from Burundi. China produced 140,000 tons last year and continues to dominate the refining of REEs. Some new refining capacity is being established in the United States, Malaysia, and elsewhere. Given environmental standards and intellectual property rights over refining techniques, however, it is unlikely that even with an increase in overseas production of raw mineral ores, there will be a major reduction in dependence on Chinese refining.

Who’s Left Behind

One other geopolitically significant implication of the race for new energy may be in those countries left behind. As we noted, new energy does not eliminate the use of old energy, and oil and natural gas are not going to simply disappear from markets. But that doesn’t mean all current hydrocarbon-dependent economies will remain viable. Costly or fringe areas of oil and gas production may begin to lose international investment and attention due to a combination of competing energy sources, political and regulatory changes, and social and environmental investment pressures. Countries overly dependent on oil and gas exports, as well as those with unstable political, regulatory or security environments, are at risk of divestment. Shifting investment patterns can have a significant impact on national revenues and social policies. And if divestment comes mostly from Western nations, replacement investment from China could bring with it changes in political relations and priorities.

There are, of course, other implications of a changing climate and energy mix on the geopolitical balance of world power that we will continue to explore. The shift from landline to cellular telephones provided an economic and development boost to regions like southern Africa, where there was little chance of heavy investment in the physical infrastructure for dispersed populations. New energy may provide similar opportunities for dispersed populations. But if grid connectivity remains important for power redundancy, the cost of running additional lines may leave many areas isolated as others rapidly expand electrification, widening the opportunity gap between regions.

Not all populations are necessarily willing to shoulder the cost of the energy transition, even in developed countries, which may also lead to greater fragmentation — particularly as countries begin to add tax and tariff to carbon costs of manufacture. And as the mining of minerals for alternative energy expands, so too will the environmental cost shouldered by the resource-supplying countries, which will once again stoke frictions and potential political revolutionaries as larger powers are accused of resource imperialism.

As we look at the impacts of climate change, the political decision to pursue alternative energy will drive new competition over critical resources. History is replete with examples of the opportunities and instabilities that shifting commodity priorities can engender. Competition over resources will reshape political and economic priorities, refocus military and security assets, and intensify local political dynamics as new money and competing political interests of big powers converge on resource producers. But while the world may have moved past imperialism and colonization as tools to secure critical resources, the disruptive pressures at the local level are often no less severe, and the focal areas for great power competition will follow the shifting mineral priorities.