Peruvians wearing masks to protect themselves from COVID-19 wait outside a bank to collect government aid bonuses in Iquitos, Peru, on June 15, 2020.

Peru’s post-pandemic path to economic recovery will primarily require retaining confidence in prudent fiscal management and political stability, as well as addressing the structural issues impeding the country’s long-term financial sustainability. Peru has a window of opportunity to address long-term issues, but in the absence of progress, the economy is vulnerable to exogenous shocks that increase short-term risks to economic stability.

Peru is a generally well-managed economy that has had strong overall growth with low inflation, and low public sector and external debt. Indeed, its reputation among international investors, including an investment-grade sovereign credit rating, is based on previous prudent fiscal management that includes a fiscal rule limiting budget deficits and low debt-to-GDP ratios. As such, under “normal” circumstances a probable post-pandemic return to positive growth would be expected to be accompanied by declining budget deficits and moderate growth in external and public sector debt. Reasonably-sized budget deficits averaged less than 2% of GDP from 2014 to 2019. But this year the deficit will equal 10.7% of GDP in 2020 and, under the recently passed budget, is expected to decline to 6.2% of GDP in 2021. Both, however, are historic highs and the decline in 2021, while achievable, will represent a massive fiscal adjustment.

Yet, political tensions have dominated in recent years, including having three presidents in the span of one week in November 2020. That has added significant political risk and uncertainty to Peru’s economic policymaking, especially as politicians jockey for advantage ahead of the April 2021 general election. Although the government approved a budget at the end of November that is similar to the one put forth by impeached President Martin Vizcarra, Peru’s governance structure exaggerates stresses between the executive and legislative branches, and there remains a high probability of the country resorting to populist economic policies. Vizcarra’s ouster under a controversial procedure was akin to a “no confidence” vote in a parliamentary system and weakens executive power, even as the was opposed by many Peruvians. It puts a premium on the ability to pander to popular sentiment to retain or maximize short-term political gains.

With the highest per capita death rate in Latin America, Peru’s COVID-19 crisis has helped drive its economy into a deep recession, despite massive fiscal stimulus. The Peruvian economy was projected to have shrunk 14% in 2020, following a decade in which annual growth averaged 4.5%. The country initially had one of the world’s strictest COVID-19 lockdowns. But with two-thirds of the labor force in the informal sector, Peru’s lockdown was unenforceable, even as it devastated output, including in the critical mining sector. Lockdown measures have since been eased, with economic populism gaining strength as politicians try to supplement a $27 billion stimulus plan to jumpstart the economy, which amounts to 12 percent of GDP.

Peru has not had difficulty financing fiscal deficits, using a combination of its own resources and new international borrowing. But its fiscal stabilization fund may be depleted. On Nov. 25, Peru was able to place $4 billion in 12-, 40- and 100-year bonds in what was considered an early vote of confidence by markets for the new interim government led by Francisco Sagasti. The so-called “century bond” was at a relatively low yield of 3.3%, which shows faith in the ability of Peru’s central bank to manage inflation, as well as in Sagasti’s ability to restore stability.

Yet Peru is at an inflection point, with political uncertainty putting its status as a stable and attractive investment destination at risk, which will not change once the pandemic passes. On Dec. 15, Fitch Ratings fired a warning shot at Peru, changing its outlook on the country’s credit ratings from stable to negative, while leaving Peru’s sovereign rating at BBB+. The agency cited the "deterioration of policy predictability" in the country and its government's "weakened balance sheet,” as Peru authorized public pension withdrawals to further stimulate its declining economy. The country’s public pensions are on a "pay-as-you-go system" and require increased government current expenditures to cover withdrawals, threatening its reputation for fiscal responsibility. At the same time, several high-level officials are exiting Peru’s Ministry of Economy and Finance, possibly undermining its professionalism.

Peru also has an open, unconditional $11 billion credit line available from the International Monetary Fund (IMF) that was approved in May. Given the country’s current circumstances, however, it’s unclear whether the IMF would grant Lima access to those funds without further consultation and agreement on a fiscal path. Along with gross foreign exchange reserves of $60-70 billion, the IMF credit line would be a last line of defense in the event of a further crisis. But Peru has seen three presidents and two finance ministers since the IMF agreement was negotiated, meaning the continuation of prudent policies on which it is based cannot be assured.

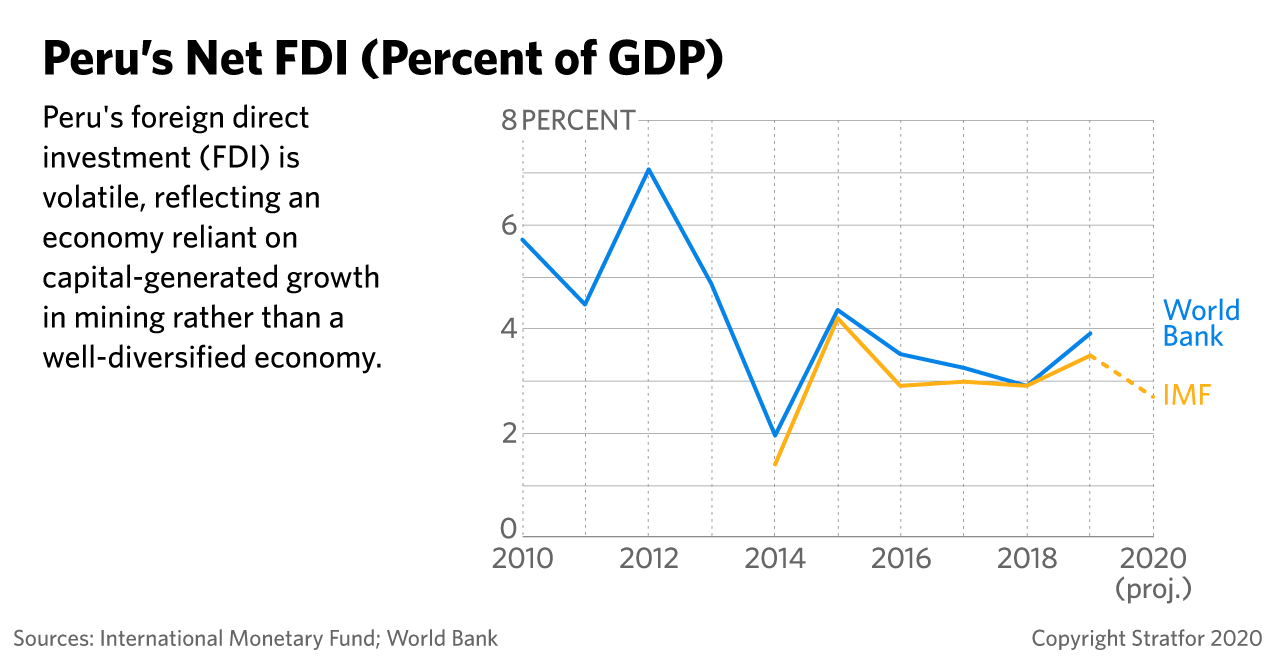

The COVID-19 crisis has also exposed Peru’s structural weaknesses that were previously masked by strong cyclical growth. Peru could use its current reputation and available financing to buy time to address systemic issues, such as its unbalanced development model that’s based mainly on capital intensive growth, especially the mining sector. Peru’s resource-rich, commodity-dependent economy has attracted large foreign direct investment (FDI) and enabled growth fueled by fast capital accumulation. But the country’s high degree of “economic informality” of a largely young, urbanized population leaves many workers without stable links to an economy that is vulnerable to natural disasters.

- While the country is open to FDI, it has a negative investment climate. Peru is ranked 101 out of 180 countries on Transparency International’s global corruption index in 2019.

- Partial dollarization of the economy also leaves banks and the financial sector exposed to exchange rate risk. At the end of 2019, foreign currency accounted for 35% of bank deposits in Peru and more than 26% of banking sector loans.

- Peru is in a “middle income” trap as well: Between 2000 and 2012, Peru’s middle class as a percentage of the population has grown also from 12.3% to more than 34% in 2012. There have been few productivity gains and little export diversification in recent years.

The new Peruvian government elected in April will face trade-offs between continued fiscal stimulus and a reduction in debt with a rebuilding of savings. Recent public opinion polls show most Peruvians are estranged from the political process, but favor constitutional reforms that would correct recent political quarrels and tamp down corruption. But it’s unclear whether this will translate to the election of a government that favors a continuation of the current policy.

Peru is a rare emerging market country that has time to address long-term issues without putting immediate growth at risk — but only if it takes advantage of that grace period to act. Peru’s primary economic headwinds include reduced growth momentum, with concerns about the country’s long-term financial prospects and political stalemates delaying crucial economic reforms. Such headwinds could hamper fiscal deficit reduction if Peru cannot legislate tax increases or resist spending pressure. In addition, global GDP growth will determine the demand for commodities and metals prices. In a potentially adverse scenario, Peru may be forced to compress imports to avoid increasing its current account deficit. An uptick in global uncertainty and risk aversion could also sap FDI.