An employee of a currency exchange counter shows a stack of dinars in the southern Iraqi city of Nasiriyah in Dhi Qar province on Dec. 20, 2020.

Devaluing its currency will help Iraq slow the drawdown of foreign currency reserves but will increase the cost of living, weakening already fraught public support for Iraqi government efforts to implement other longer term reforms in 2021. On Dec. 19, Iraq's central bank adjusted the sale price of dollars to Iraqi banks and currency exchanges from 1,180 dinars to the dollar to 1,460 dinars, an almost 24% devaluation, Iraq's first since 2003. The devaluation will help the government balance sheet going into 2021 by enabling Baghdad to pay overdue salaries in local currency at a better rate, but will not help with other deeper economic reform efforts still being debated by politicians.

- The government is actively debating the 2021 budget, which projects high spending — 150 trillion dinars, higher than the 133 trillion-dinar 2019 budget — but also a high deficit at 58 trillion dinars. (Passing a budget can be such a fraught process in Iraq that a 2020 budget was never officially passed.)

- The International Monetary Fund warned in late 2019 that Iraq's real exchange rate risked moving into "overvalued territory" without fiscal adjustment, and indeed Iraq has increasingly used reserves to prop up its currency.

Iraq's government took the unpopular decision to devalue now because it will help balance its growing budget deficit and stem the swift drawdown on its financial reserves. Iraq's widening budget deficit was aggravated by COVID-19's negative impact on oil prices and oil revenue, Iraq's main source of income, which is earned in dollars. Iraqi foreign exchange reserves (excluding gold) fell to $51 billion by the end of September per the Central Bank of Iraq's most recent available data, down from $62 billion at the end of 2019. The same day as the devaluation, the Iraqi government estimated that it would deplete foreign currency reserves entirely within seven months if it had not devalued the currency — and if the central bank could suddenly no longer defend the currency peg, Iraq would have faced a disorderly and abrupt devaluation anyhow.

- The IMF forecast in mid-December 2020 that Iraq would see an 11% contraction in gross domestic product growth this year and the World Bank forecast in October 2020 that Iraq's economic growth could recover to somewhere between 2.0% and 7.3% in 2021, but only if crisis conditions ease.

- The Iraqi government derives 90% of its revenue from oil, which becomes a liability and not a strength in a year like 2020 that saw a global decrease in demand for energy.

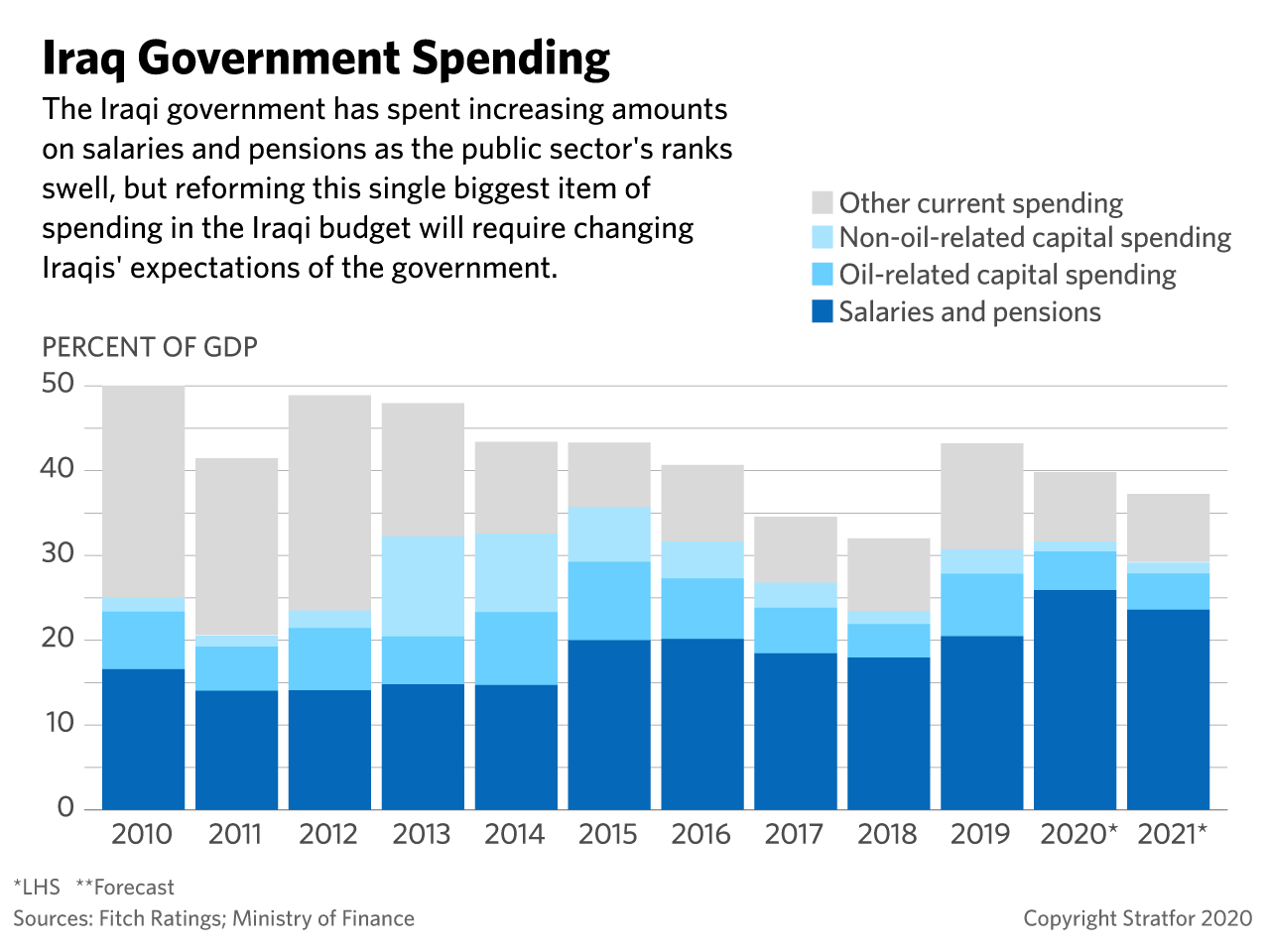

Devaluation will enable the government to pay public sector salaries in the near term. But it will not help solve the growing price tag of public sector salaries, pensions and benefits in the long term, highlighting one of the biggest and toughest financial problems Iraq faces. Devaluation will lower the cost in dollars of public sector salaries and other dinar-denominated liabilities, but actually reducing the overall cost of salaries as a percentage of spending in the budget will require undoing long-standing social expectations of the government providing welfare, employment and other benefits to Iraqis.

- Iraq's biggest employer by far is the government, which employs 4 million public sector workers, pays pensions to 3 million and supplies welfare to 1 million.

- The Iraqi government loosely plans to reduce the public sector wage bill from 25% of GDP to 12% of GDP over the coming year, which will mean forced retirements likely to stir anger at the government.

Devaluation will raise the price of imports in a country that imports most of its goods and lacks the ability to quickly ramp up domestic substitutes, which will increase the cost of living in a poor country about to face other austerity measures. Iraq already struggles with significant poverty. Its official poverty rate has roughly doubled this year to 40%, high even by regional standards. A sharp increase to the cost of imports without sufficient cheaper domestic substitutes will exacerbate inflation and existing cost of living struggles, even if over the long term this encourages the development of domestic manufacturing. In a country that struggles with persistent economically motivated popular unrest and frequent anti-government demonstrations, any cost-of-living increase easily risks sparking even more unrest. Moreover, devaluation comes as the government is planning to implement other measures in 2021 that will increase the cost of living, including a new income tax. New planned hikes to utility costs in 2021 will also collide with planned slashes to Iranian energy imports, likely increasing the cost of electricity and creating volatility in supply.

- Iraq imports more than it exports. In 2019, it imported $92 billion worth of goods, mostly manufactured goods (Iraq does not have a well-developed manufacturing sector), medication, vehicles, tobacco and food. Iraq exported $86.8 billion, overwhelmingly crude oil and fuels.

- Part of the 2021 budget discussions include plans to rationalize subsidies on utilities and implement a new 15% income tax, both of which will increase the cost of living.

The Iraqi government will struggle to implement deeper reforms given the weak political will of the current government, growing public anger over devaluation and the volatile economy, and the fact that 2021 is an election year. Public dissatisfaction with the government's decision to devalue the currency will weaken Baghdad's ability to implement and follow through on much-needed reforms. Moreover, slated legislative elections in June 2021 will render many politicians skittish about making any unpopular decisions on reforms that could lead to austerity measures. And without fixing systemic corruption (a highly unlikely development over the next year), it's hard to see Iraq's economy getting on a better footing in the long term.

- In mid-December, the IMF said that in order for Iraq to actually establish firm financial footing for the long term, it needed to "strengthen public finances, improve governance, reform the electricity sector, promote private sector development, and ensure financial sector stability," all of which will require significantly increased state power and stability.