(Burak Kara/Getty Images)

Turkey faces a stark economic choice. It could continue on its current path, artificially propping up growth at risk of deepening pressure on the financial system and currency, and perhaps precipitating a balance of payments crisis with a collapsing banking system and possible sovereign default. Or it could accept the short-term pain of a renewed recession caused by tight monetary and fiscal policy from increased interest rates and reduced fiscal and credit stimulus. The second option would attack high inflation, compress imports and lay the basis for a return to sustainable growth. A Central Bank decision on Nov. 19 will shed light on what path Turkey is choosing.

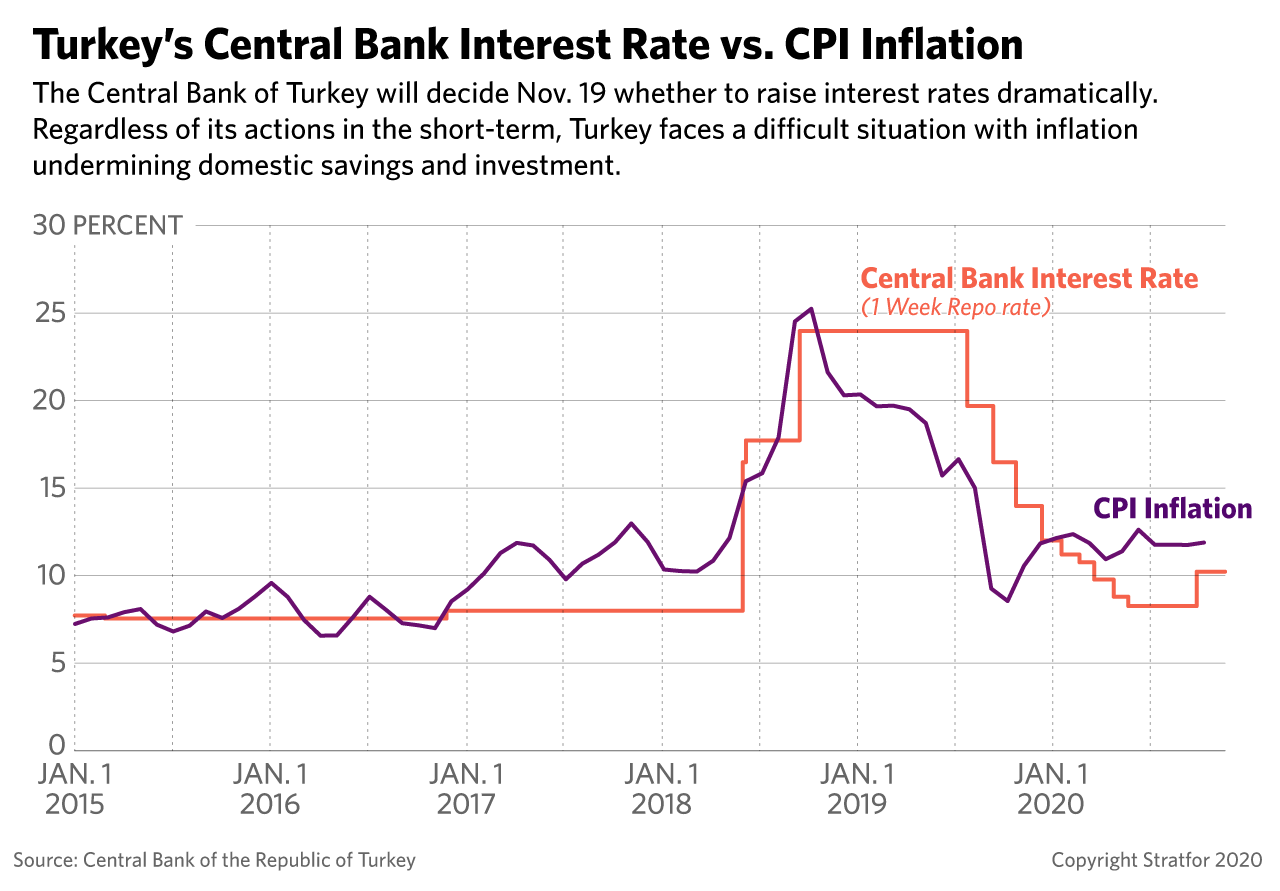

Turkey's efforts to reverse a long-term currency depreciation and mitigate a nascent financial crisis face a critical test Nov. 19, when the Monetary Policy Committee of the Central Bank of Turkey decides whether to reverse course and raise interest rates dramatically. Turkey's leadership, including President Recep Tayyip Erdogan, has raised investor expectations via recent statements and personnel reshuffles. Failure to satisfy these expectations could plunge Turkey into a near-term currency, balance of payments and banking crisis. Erdogan's Nov. 7-9 shake-up of his chief economic advisers plus various statements made since have seen the lira recover about 10 percent of its value against the dollar.

- New Central Bank Gov. Naci Agbal pledged Nov. 11 to restore transparency and predictability to monetary policy.

- Erdogan said Nov. 11 he would start a period of economic and legal reform, including implementing "bitter pill policies if needed" to get the economy back on track.

- He then said in a televised speech Nov. 13 that bringing inflation down into single digits is the government's highest priority.

- Newly appointed Finance Minister Lutfi Elvan said Nov. 17 that "Turkey's growth process will be designed and controlled in a way that doesn't contradict our fight for macroeconomic stability and against inflation."

Markets generally expect the Central Bank to raise its one-week refinancing rate, the main policy interest rate, by at least 475 basis points to 15 percent from 10.25 percent at present. That would be consistent with inflation of about 12 percent, making interest rates positive by about three percentage points. But that does not account for a country risk premium of at least four percentage points as shown by the current cost of five-year credit default swaps and the current yield spread of Turkish eurobonds over 10-year U.S. Treasury securities of more than 5.8 percent.

Nonetheless, there is speculation that the Central Bank might try to get away with a much smaller basis point increase of just 150 in the face of sharply decelerating domestic credit growth that stood at 40.4 percent between June-September 2019, but only 2.1 percent in September. It's unclear if markets will perceive that as a step in the right direction, or see it as lacking in credibility and signaling only minimal action. Erdogan has traditionally favored policies that encourage credit growth to stoke economic consumption and investments, and old habits die hard, meaning he might want to avoid a large interest rate increase.

Regardless of short-term Central Bank action, Turkey faces a difficult situation it must address sooner rather than later, or risk heightened uncertainties:

- Inflation is an enduring problem in Turkey, and investors do not trust the Central Bank to manage the issue, especially after the rise in the price level hit 25 percent in 2018, five times the target rate. And Turkish academic economists recently cited evidence that the government might be underreporting inflation, especially given perceived politicization at the official Turkish Statistical Institute. The weak lira combined with high inflation expectations undermines domestic savings and investment.

- Negligible Q3 growth did not make up for a 10 percent decline (year on year) in H1, and Turkish GDP is projected to end the year having declined up to 5 percent over 2019.

- Growth has been supported by credit-led stimulus that increases consumer credit at extended maturities and submarket interest rates. But that boosted import demand, exacerbating a chronic current account deficit. This plus other economic imbalances put downward pressure on the lira, and increased the risk of instability.

- The depreciating currency has not helped reduce the current account deficit. This is because dependence on imported energy priced in dollars and a high import content of exports has limited gains in competitiveness from a weak lira. The current account deficit swung from a surplus of $2.8 billion in the first nine months of 2019 to $2.4 billion in the same period of 2020, with capital outflows and a further decline in foreign exchange reserves.

A plausible and enduring tightening of monetary policy is a first condition to reassert policy credibility with domestic and international investors, but Erdogan's history is not reassuring. Mixed messages are being sent as to whether the president really has given up on his preference for low interest rates regardless of the cost. Even as he talked about bitter medicine Nov. 11, Erdogan lamented "the shackles" of interest rates endured by Turkey. On the eve of the meeting, Erdogan reiterated opposition to high interest rates, but that may be a bit of political theater for now. Ahead, however, there is no guarantee that he will not seek a return to high growth as a platform for reelection. Erdogan is up for reelection no later than 2023, but may call a vote earlier.

A substantial tightening of fiscal policy is also necessary, even in the face of increased costs from COVID-19. The government's medium-term plan, introduced at the end of September, has not been reworked. It projected positive growth for 2020, including fiscal deficits of nearly 5 percent of GDP for 2021 and 4 percent for 2022. Deficits have been widening since 2018 with 2019's red ink jumping by 70 percent and off-budget activities and guarantees equal to about 4 percent of 2019 GDP. The 2020 budget deficit was up by 44 percent in the first 10 months compared with the same period in 2019. The medium-term plan also dismissed structural problems related to Turkey's boom-bust economic cycles, including high reliance on capital inflows, high inflation, mismatches in corporate debt between lira revenues and foreign currency liabilities, deteriorating bank asset quality and creditworthiness, and chronically low domestic savings relative to domestic investment — the very definition of a current account deficit.

Turkey has not had difficulty accessing global capital markets, but the short maturity structure of external debt should be a concern, with more than 50 percent of $440 billion in debt due for repayment by 2023, according to Bloomberg News. High-risk appetite seems to have returned for emerging market debt and Turkey was able to place a $2 billion eurobond in early-October — but only at a yield of 6.4 percent, which was 200 basis points higher than its previous issue in February. A liquidity crunch or pressure on external funding from a return of global risk aversion would lead directly to a debt and balance of payments crisis.