A picture taken on Aug. 14, 2018, shows the logo of Turkey's central bank at the entrance of its headquarters in Ankara.

On Sept. 24, the Central Bank of the Republic of Turkey (CBRT) announced a surprise interest rate hike in a preemptive move that seeks to prevent the country’s depreciating currency from unfolding into a larger banking or balance of payments and external debt crisis. The steadily declining value of Turkey’s national currency, the lira, is largely the result of economic imbalances — partially precipitated by a highly negative real interest rate, a credit-fueled construction boom, and large external financing needs, as well as the CBRT’s lack of credibility and near exhaustion of Ankara’s foreign currency reserves.

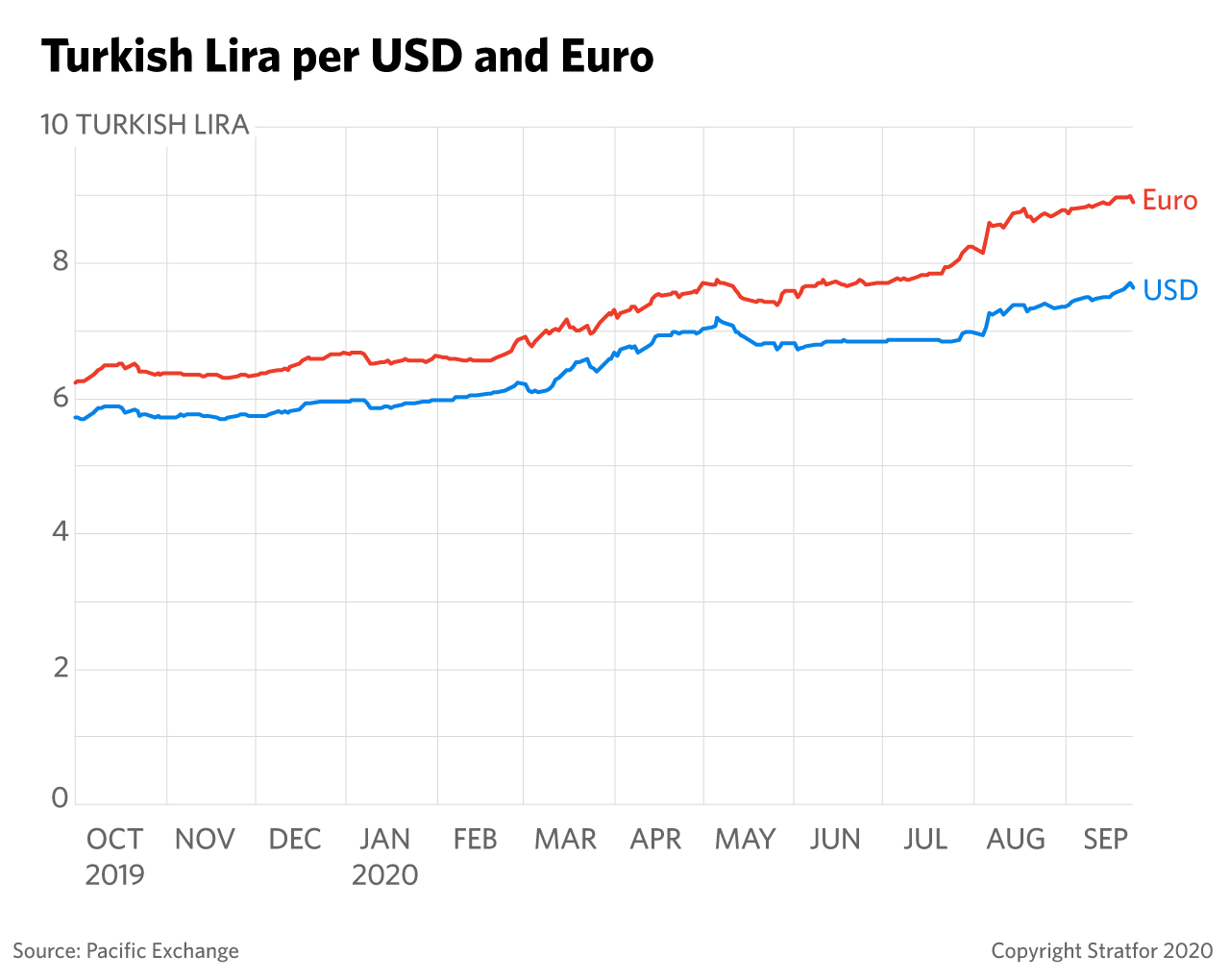

- The lira hit historic lows against both the dollar and euro on Sept. 23, depreciating nearly 15 percent and more than 21 percent, respectively, since late May.

- Turkey is in its second currency crisis in a little more than two years. Unlike previous episodes of currency weakness, however, Turkey’s foreign currency reserves are exhausted and its exports have not responded to the plummeting exchange rate.

A major change in Ankara’s monetary policy was likely necessary to break the lira’s exchange rate decline, given that Turkey is among the world’s most vulnerable emerging market economies. The latest available data from July indicated that Turkey’s net reserves were then negative, at -$38 billion, with gross external financing requirements (current account deficit plus external debt due in the next twelve months) equivalent to more than 25 percent of GDP (or more than $200 billion). International investors’ willingness to finance those needs have declined precipitously on the basis of Ankara’s unorthodox monetary policies, which have included lowering interest rates even in the face of relatively high inflation.

- The CBRT reports gross reserve assets of $90.3 billion, but that includes $45 billion of gold that is illiquid and cannot be used to settle debts.

- There are, however, $83.1 billion in net liabilities that include foreign exchange swaps with domestic banks. The latter are essentially borrowed reserves from domestic banks.

- The CBRT could theoretically use gross reserves for emergency needs, though defaulting on liabilities, especially foreign exchange swaps, would risk plunging the Turkish banking sector into crisis.

- Turkey does not report foreign exchange intervention data, but is believed to have sold about $30 billion into markets from March-July to slow the lira’s depreciation, with total 2020 intervention possibly as high as $80 billion.

Turkey’s slowing economic growth, high inflation and weak banking sector have placed Ankara under increased political pressure, which may have prompted the CBRT to try to increase the cost of funds to commercial banks as a backdoor option for monetary tightening. The new rate hike, however, strips away the facade of policy easing by the CBRT, with its benchmark policy interest rate increasing by 200 basis points (bps) from 8.25 percent to 10.25 percent on Sept. 24, and the CBRT tightening liquidity the day after the announcement. That partly reverses cuts totaling 1,575 bps made between July 2019 and May 2020, despite an inflation rate averaging just under 12 percent in 2020. Turkey’s inflation may also be underreported since nearly 30 percent of the country’s consumer price index includes goods subject to price setting or influence by the government. The rate hike announcement has, however, immediately strengthened the lira’s exchange rate.

Suppressed interest rates were previously intended to stimulate the Turkish economy, which is expected to shrink by up to 5 percent this year due only in part to the COVID-19 pandemic. Banks, especially Turkey’s three state-owned banks, have also been pressured to lend and to show extreme forbearance on delinquent loans. This, combined with negative real interest rates, has created a credit bubble in which year-over-year (YoY) domestic credit was up by 41.5 percent in July alone. That encouraged an unsustainable surge in domestic construction, with house sales up by 124.3 percent YoY in July after a 208 percent increase in June. At the same time, Turkey’s gross fixed capital formation has been falling, down by nearly 15 percent in 2019, suggesting a boom in unproductive domestic investment.

Turkey also suffers a chronic shortfall in domestic savings resulting in a structural current account deficit, amplified this year by rising imports from the domestic credit binge.

- A high import content of exports, averaging more than one-third, has sapped the pass-through effects of currency depreciation on export competitiveness. In addition to a weak global environment, that has caused falling external demand from Turkey’s main trading partners in Western Europe. This has, in turn, stymied increased exports.

- Collapsing international travel and tourism, which makes up roughly one-fifth of Turkey’s exports and accounted for $35 billion in 2019 export revenue, was off by 95 percent in the first half of 2020, further limiting the availability of international funding.

- Turkey’s balance of payments depends extensively on short-term foreign borrowing that currently stands at more than 15 percent of GDP, or more than $100 billion based on the country’s 2019 GDP.

- Net foreign direct investment was only 1.1 percent of GDP in 2019, well below the average for similar countries such as Portugal (3.5 percent), Poland (2.5 percent) and even Argentina (1.4 percent).

Long-term external debt sustainability is sensitive to lira depreciation, as well as Turkey’s high external financing needs (which prior to the COVID-19 crisis, were estimated at about $200 billion per year, including the current account deficit, or nearly one-fourth of Turkey’s pre-crisis projected GDP). Turkey’s external debt is only moderately high at 58 percent of GDP as of the end of 2019 according to World Bank data. Turkey’s public debt-to-GDP was only 32 percent at the end of last year. Nonetheless, there is an unknown, but possibly large amount of off-budget contingent liabilities with more than $60 billion in government-guaranteed investments under public-private partnerships made for 221 projects in 2018.

Turkey’s financial vulnerability is also heightened by a relatively high level of domestic “dollarization,” with 51 percent percent of domestic bank deposits in foreign currencies compared with only one-third of banking sector assets as of Sept. 18. Turkish banks appear well-capitalized, with low levels of non-performing loans (NPLs) at only about 5 percent. That’s deceptive, however, with NPLs distorted by regulatory actions encouraging forbearance that keep suspect loans out of collection without increasing credit quality. Loans with government guarantees are also risk-weighted at zero. Among other things, the lira’s depreciation has stressed corporate balance sheets for companies with foreign currency debt, and NPLs could increase to 20 percent by next year.

While CBRT’s rate hike provides some immediate clarity to economic policy, it’s still unclear whether Turkey has the political will to make needed economic reforms to address looming financial issues and achieve long-term sustainable growth. Other issues Ankara has yet to address include:

- Strengthening corporate and commercial bank balance sheets. Turkey’s sovereign wealth fund injected $3 billion into the three state banks in May, but action is needed to deal more decisively with problem loans.

- Disinflation to achieve positive real interest rates, as well as underpinning the exchange rate and supporting de-dollarization. The new CBRT policy rate increase begins to address this issue, but real interest rates are still negative.

- Resolution of contingent fiscal liabilities to increase transparency and control off-budget expenditures. Falling tax revenue with lower employment and a deferral of business taxes in an effort to keep companies afloat have swelled Turkey’s fiscal deficit, which in the first seven months of 2020 exceeded that budgeted for the entire year. Employment support is financed through the government’s off-budget Unemployment Insurance Fund (ISF), adding to the real deficit that is financed mainly through the banking system.

- A replenishment of foreign exchange reserve buffers, with the CBRT refraining from direct market intervention and avoiding capital controls.