Russia's cautious approach to oil production cuts will triumph over Saudi desires for deeper trims at the OPEC ministers meet late next week at the cartel's headquarters in Vienna.

OPEC+ is likely to agree on a modest cut in oil production at the regularly scheduled meeting of OPEC ministers on March 5-6 in Vienna. The ministers most likely will simply agree to adopt the recommendation of the cartel's technical committee earlier this month for an evenly distributed trim of 600,000 barrels per day. At that time, Russia turned down a Saudi suggestion that an emergency ministerial meeting be scheduled, preferring instead to monitor the spread of the COVID-19 outbreak to get a better gauge of its expected impact on demand.

Now, with the widespread expectation that the disease will become a global pandemic, Russia will be convinced of the need for action. But any cuts it agrees to will fall well short of the dramatic volume that would jolt the price of the Brent crude benchmark. Rather, production targets will be adjusted to limit a further slide in prices. Cuts beyond current levels likely will not take effect until the second quarter at Russia’s insistence, allowing for a reassessment in June. The fact that Libyan production remains down over 1.1 million bpd and shows no sign of a quick recovery is also a major consideration limiting a deeper cut. However, if Libyan production resurges, OPEC+ production levels could be adjusted.

There's a wide degree of uncertainty around the level of reduced demand that will result from the coronavirus crisis. S&P Global Platts and Bloomberg estimated that Chinese demand in February would decline about 3 million bpd, but with many Chinese businesses restarting after an extended Lunar New Year holiday, consumption seems to be recovering outside strict quarantine zones. Road traffic data from GPS maker TomTom shows an increase in most Chinese cities over the past week, though traffic volumes remain well below normal. The data also shows a marked decline in traffic in Milan, the epicenter of Italy’s cluster of COVID-19 cases. However, there's been no real impact yet in Rome or the rest of Europe.

While it has become clearer in recent days that the COVID-19 virus likely will spread widely outside China, once that happens, the response of other governments is likely to change. Mandatory travel restrictions will be seen as less effective, and published plans by the British government, for example, do not envision cutting off international travel because of the economic effects. Rather, prevention efforts will begin to shift toward personal hygiene measures and the protection of vulnerable individuals. This uncertainty will make Russia reluctant to commit to deeper production cuts through the end of the year, but that could change if demand drops further.

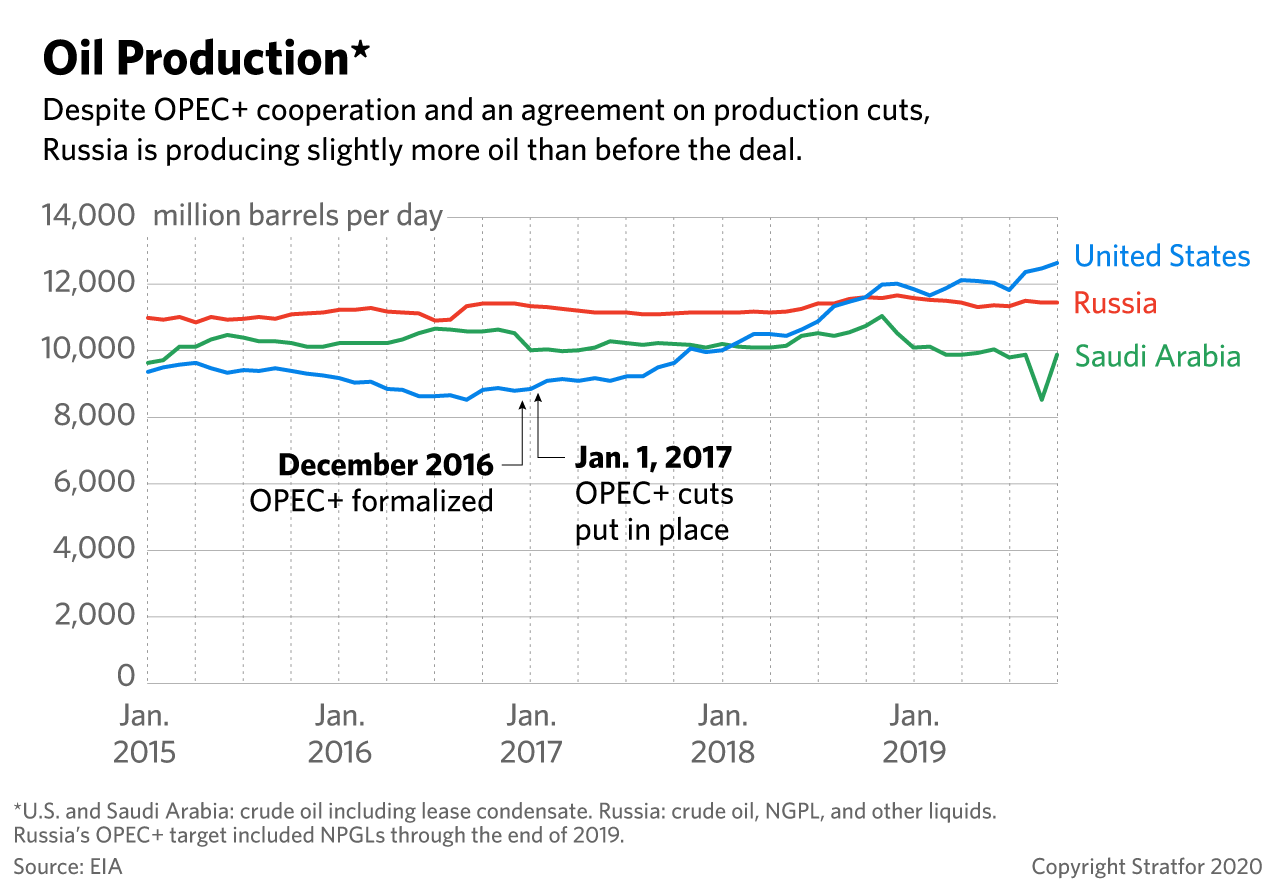

Russia's desire to err on the side of caution again shows its differences with the Saudis and the relative power positions in that relationship. President Vladimir Putin has clearly accepted the "lower for longer" philosophy of oil prices and has made very conservative budget assumptions. Russia only needs Brent to range in the high $40s per barrel to balance its state budget and it has plans to cope if prices dip to the low $40s. In contrast, Saudi budget assumptions rely on a Brent price of around $80 per barrel. Putin said publicly last summer that he considers $60 to $65 as the normal range for Brent, but Russia’s reluctance to back swift action in reaction to COVID-19 shows that it accepts that living through a period below that target would be preferable to trying to defend $60 Brent at the cost of continuing to lose market share to U.S. shale and other competing production.

The Saudis are somewhat frustrated at the situation but do not have good options other than accepting what Russia is willing to do. Imposing deeper cuts either unilaterally or in coordination with Kuwait and the United Arab Emirates remains a plausible, but unattractive, possibility. The Saudis already caved to Russia at the December meeting, accepting Moscow's insistence that it would only commit to price restraint for only three months and redefining Russia’s target to exclude condensates. This moved the goalposts in a way that accommodated Russian cheating and obviated the need for them to make any incremental cuts.

At this point, Moscow will likely stick to a commitment to only modest incremental cuts in the second quarter. The Saudis probably will not go sufficiently deeper on their own or in conjunction with Gulf Cooperation Council partners to erase the likely inventory builds during that period. That would take an effective OPEC+ volume of at least 1 million bpd in addition to Libyan production remaining offline, with the Saudis taking probably half of that volume. If the COVID-19 crisis worsens into the second quarter, the Saudis will first try to agree with Russia on additional distributed cuts, rather than running the risk of the Russians bailing out entirely, then returning to production growth when the crisis abates.

All of this leaves us with a situation where markets have already priced in the anticipated outcome of the OPEC+ meeting. While a failure to agree on any cuts would cause a further price slide well into the $40s for Brent, the expected headline will deliver only modest relief for prices. The Russians know there is a light on the horizon in the form of slowing U.S. shale growth. The dip into the $40s for West Texas Intermediate crude will not significantly affect U.S. volume growth in the second quarter, but in the second half of the year, it should further pare back capital expenditures. The Russians hope this will allow them and the Saudis to increase volumes a bit into 2021.