Maj. Gen. Tun Tun Nyi, Maj. Gen. Soe Naing Oo and Brig. Gen. Zaw Min Tun (left to right) of Myanmar's military information committee discuss their intent to thwart attempts by leader Aung San Suu Kyi's party to alter the "essence" of the country's constitution at a news conference in February 2019.

Editor's Note: This assessment is part of a series of analyses supporting Stratfor's 2020 Annual Forecast. These assessments are designed to provide more context and in-depth analysis of key developments over the next quarter and throughout the year.

In the months leading up to Myanmar's late 2020 elections, an atmosphere of political uncertainty and a risk-averse approach to reforms will combine to make it difficult for the country to attract foreign investment, even as it pushes to diversify beyond Chinese involvement. Myanmar's next government will likely be more divided and incoherent than the one now led by the National League for Democracy (NLD), with added complexity expected as ethnic minority, military-aligned and other parties jockey for position. More immediately, in the run-up to the election, the risks associated with spikes in anti-Muslim communal violence, stepped-up military offensives in ethnic border regions and a stagnating peace process with insurgents will rise. These factors, combined with the global trade slowdown, could limit Myanmar's economic growth. The 2020 vote, coming a decade into Myanmar's post-dictatorship period, will be a key test for the country's new political balance.

Suu Kyi Versus the Military

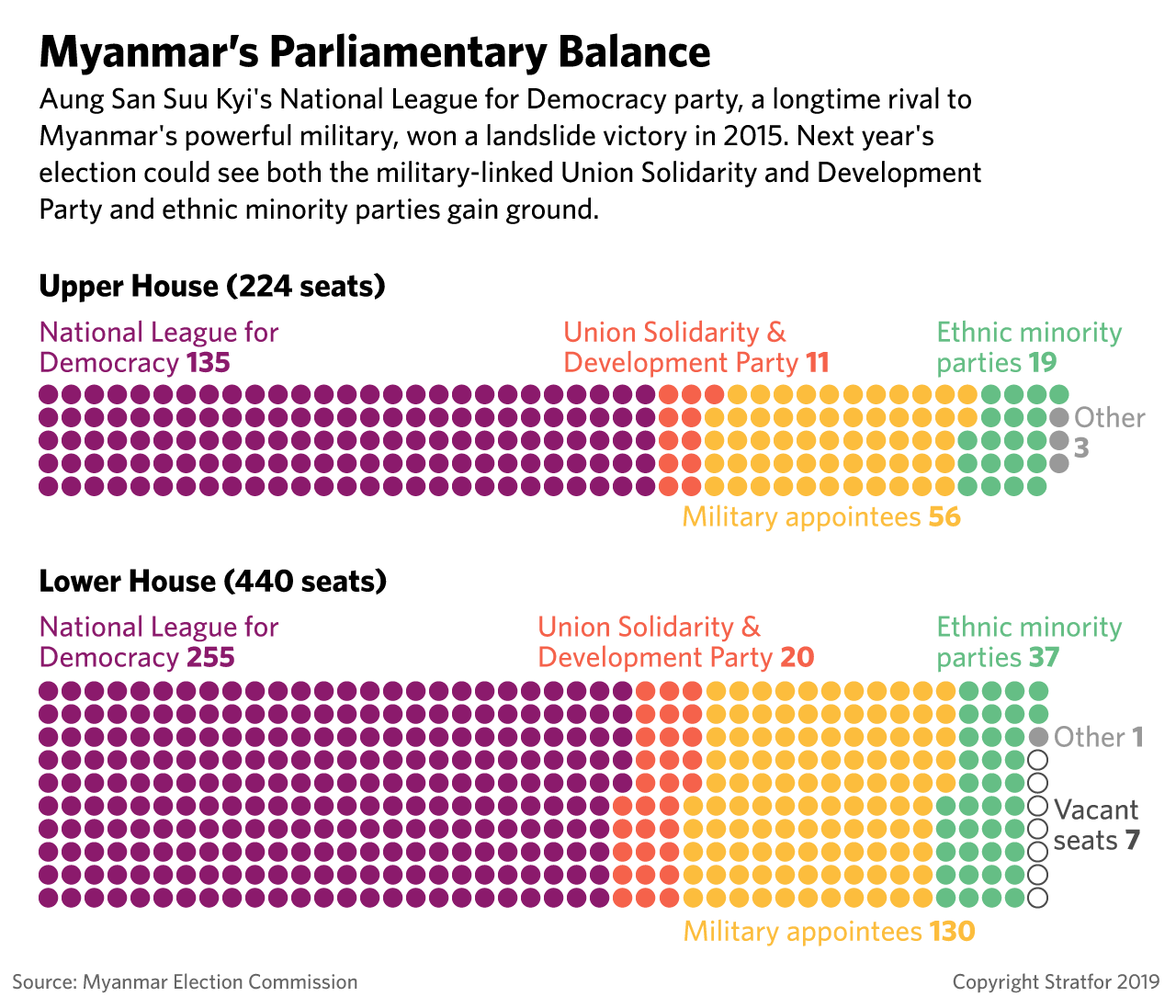

Although the election date has not been officially confirmed, sometime around November 2020 more than 1,000 seats in Myanmar's national, state and regional parliaments will be contested. The stakes are high for the ruling NLD and its leader, Aung San Suu Kyi. The party will be aiming for a repeat of its 2015 landslide victory over the military-aligned Union Solidarity and Development Party (USDP), a goal that will be difficult to achieve. Beyond competition from the USDP, the NLD's electoral strength could be divided by splinter parties that have been established since the last election. The Union Betterment Party, formed by both former military officers and a hard-line, anti-military offshoot of ex-NLD members (the People's Party) will field candidates in the next election.

Already, there are signs that the NLD's challengers are gaining steam. Myanmar's military, which ran the country for five decades until 2010, will work to increase the USDP's share of seats, seeking a mandate through its proxy party to develop a more legitimate and sustainable grip on power — much like the military in neighboring Thailand. The USDP lost badly to the NLD in 2015 but showed some signs of strength in 2017-2018 by-elections — a sign of a better performance ahead in 2020. Any gains by this party will augment the power of the deeply entrenched military, which appoints a constitutionally guaranteed 25 percent of lawmakers. Currently, the military and its USDP proxy hold 31 percent of parliamentary seats compared with the NLD's 60 percent. Gains by the military's political allies could allow them to form a coalition that would jeopardize the NLD's hold on the government or, failing that, act as a greater block to the NLD's agenda. This would make it harder for the NLD to replicate the string of successful economic policy reforms it has made since 2015, which include an amended investment law, the new Myanmar Companies Law, establishment of a new investment ministry and streamlining of investment approvals via a new online process.

In the time leading up to the election, the NLD will try to deliver on its pledge to reform the constitution, but since the military controls enough votes to vote down constitutional measures, its efforts will fail. Regardless, this could sap parliamentary attention and roil the political scene, leading to legislative delays and acrimony. The constellation of ethnic parties advocating for greater minority rights and autonomy for their regions or groups in terms of resource control and governance will also play a major role in shaping the government's post-election agenda. With Myanmar's minority-dominated periphery set to fill 31 percent of the national parliament and the majority Burman parts of the country 41 percent, the races in these regions will be key. If the ethnic parties gain greater power on the national stage, it could complicate efforts to extract resources in minority areas, challenge large development projects and push against the military's hard-line stance on ethnic insurgencies.

Peace talks between the government and Myanmar's 21 major ethnic armed groups are unlikely to make major headway in 2020 as the current government will hesitate to make concessions on key federalist powers that would open it to criticism by pro-military, nationalist challengers. The military, for its part, could escalate its offensives against ethnic insurgent groups to further impede chances for progress in those talks.

The Future of Myanmar's Economy

Myanmar will find it more difficult to attract manufacturing fleeing the U.S.-China trade war than better-developed and more stable regional industrial hubs such as Vietnam, Malaysia and Thailand. Myanmar's growth already has softened slightly since a post-transition high of 8.4 percent in 2013 but it continues to hover around or above 6 percent, where it is projected to remain through at least 2022. However, this lags the rates in high-growth, low-development regional peers such as Cambodia, Laos, Vietnam and the Philippines, demonstrating Myanmar's missed opportunities. Myanmar's infrastructure deficit, nascent internal supply chains and still underdeveloped electricity grid and banking sector make it a less attractive manufacturing destination.

Besides political volatility ahead of the elections, a potential for spikes in labor action and communal riots as well as the thorny insurgent peace process and a lack of progress in solving the Rohingya crisis will all inject further uncertainty for investors. Foreign direct investment (FDI) dropped off somewhat in 2018, with net inflows at $1.3 billion compared with between $3 billion and $4 billion per year since 2015. Approved FDI has also been falling off since 2015, when it was $9.5 billion, to $5.6 billion in 2018, and turning the FDI picture around in 2020 will be problematic, especially as the government struggles to make needed policy changes to ease corruption, red tape and regulatory uncertainty that has dampened investment enthusiasm. That said, businesses operating in the country's more developed core between Yangon and Bago or along the Thai-Myanmar border will benefit from greater government incentives such as a push for an industrial zone law that will add predictability to tax exemptions and land concessions now enjoyed in the country's 29 industrial zones. Further opportunity will come with a push for infrastructure development: The World Bank estimates Myanmar will require $120 billion in infrastructure investment over the next decade.

Chinese companies will have the greatest chance to make the most of these opportunities. Under the NLD government in late 2018, the Myanmar and Chinese governments renegotiated terms of the massive Kyaukpyu deep seaport project in Rakhine state to increase Myanmar's share to 30 percent. Those governments are also set to make a final decision on the $9 billion Muse-Mandalay railway project, which will link Myanmar's core with China's Yunnan province while providing more rapid intra-Myanmar transport as well. China is also pushing hard for the resumption of the suspended $3.6 billion Myitsone dam project in Kachin state, halted in 2011 under pressure from protests. These projects do face some risks given that ethnic parties in Kachin, Rakhine and Shan states where they are located could target them over environmental issues or inadequate benefits to local populations.

Myanmar will count more heavily on investment by China, even as it tries to avoid overreliance on its powerful neighbor. After Myanmar began its transition to democracy, most Western countries lifted the sanctions that had been applied under its dictatorship. And the 2017 Rohingya refugee crisis and continued military crackdowns in western Myanmar put the fate of Western outreach in question. While the European Union and the United States responded with sanctions targeting the military rather than the broader economy, as the crisis appears likely to linger, there is a risk that the European Union will move to revoke Myanmar's tariff-free trade access. EU trade accounts for about 12 percent of Myanmar's total, and Europe remains an especially important export market. Although concern about undermining Myanmar's transition or pushing it further into China's arms will likely prevent the EU from revoking its trade status, the bloc might launch an examination, particularly if the Rohingya conflict spikes again.

China's proximity and strategic interest in Myanmar as both an outlet to the Bay of Bengal and key to securing its southern border mean that Beijing will be far more eager to invest there, strengthening its already key position in Myanmar's economy. From 2014 to 2019, China accounted for nearly 19 percent of Myanmar's approved investment and nearly 33 percent of total trade, with that trade growing at a 33 percent rate over the past two years. U.S. trade with Myanmar, by contrast, rose less than 3 percent during that period. In terms of investment, the United States claimed less than 1 percent of the 2014-2019 approved amount, with the European Union accounting for about 8 percent.

Myanmar's next election will be a milestone in the country's transition away from the dictatorship, a period during which the West has failed to effectively supplant Chinese influence there. While Myanmar will continue to try to diversify its economic partners to reduce its reliance on China, it is becoming increasingly apparent that Chinese largesse is one of the few things the country can currently count on.