People relax on the bank of the Tagus River where Venezuelan PDVSA oil tanker Rio Arauca lies at anchor, having been impounded by Portuguese authorities for nearly two years due to unpaid debt, March 9. The ship is one of 18 vessels declared in emergency by the Venezuelan state-owned oil company after Bernhard Schulte Shipmanagement (BSM) decided to cancel operating PDV Marina (the maritime arm of PDVSA) tankers due to an unpaid debt of some 12 million euros.

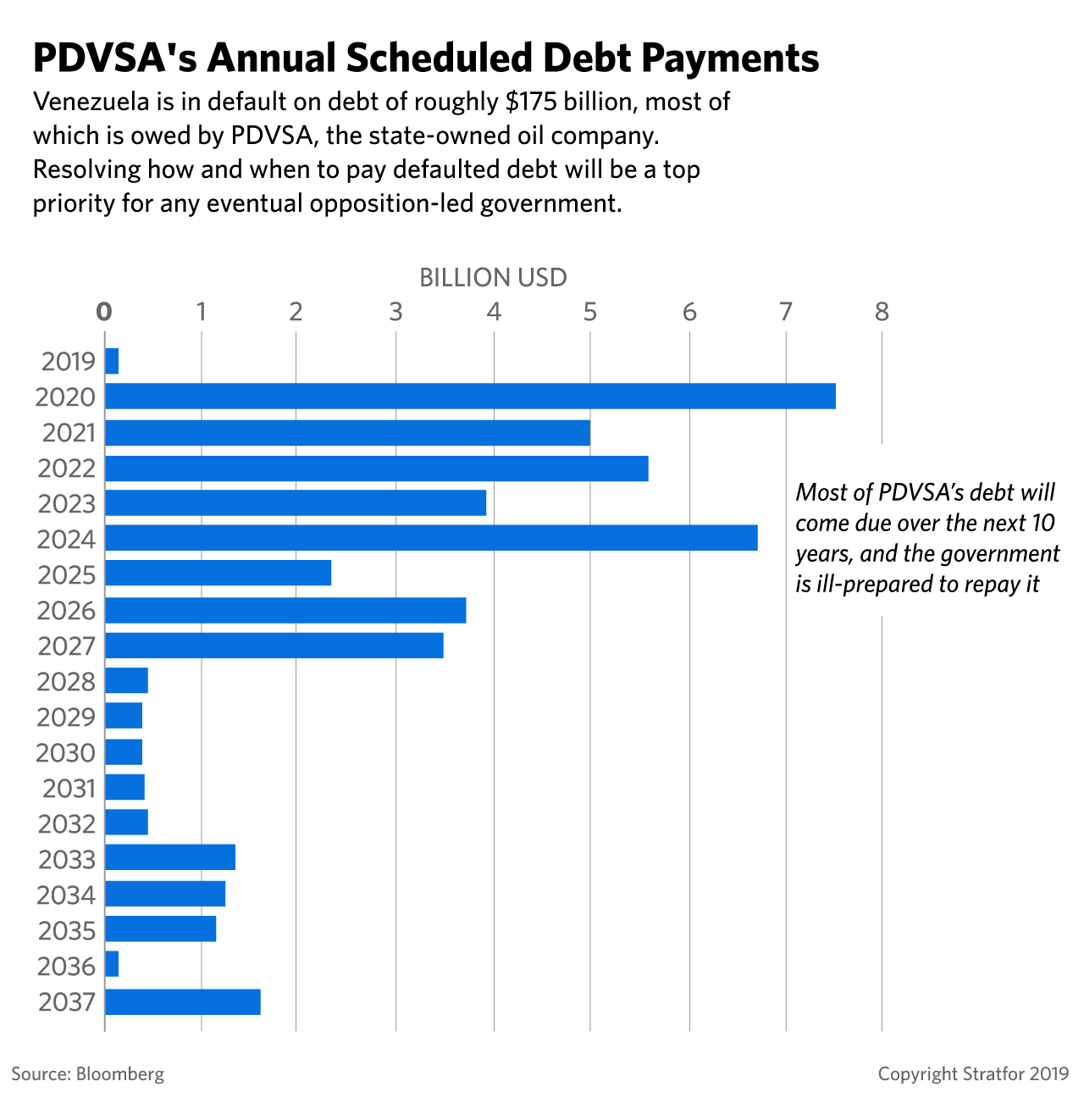

Beyond Venezuela's day-to-day grind through economic and political turmoil, legal chaos is now looming. Over nearly 20 years of leftist rule, Venezuela has defaulted on nearly $175 billion in foreign debt and expropriated assets from dozens of foreign companies — most of which took Venezuela's government to arbitration. With yearly oil export revenue sitting at less than $30 billion, Venezuela can't immediately meet most of its obligations to companies seeking debt and expropriation payments. And with the opposition faltering in its bid to unseat President Nicolas Maduro, credible attempts to lay the groundwork for a future economic recovery are receding. Given that, the economic task facing the opposition — should it ever grab power — will become larger than ever as the issue of unresolved payments clouds the likelihood of sustainable growth.

Guaido's Star Fades

During the past decade, Venezuela has steadily defaulted on most of its foreign debt, particularly after the 2014 crash in global oil prices, which plunged Venezuela's poorly managed public finances into a crisis. But creditors seeking repayment on defaulted debt know the Maduro government is unlikely to seriously entertain any debt restructuring plan; after all, the president's main priority is to cling to power — not satisfy Wall Street. Any negotiations, accordingly, would have to proceed with a post-Maduro government. But for such an administration, power might prove to be a poisoned chalice given the prospect of a lengthy legal battle with creditors — in addition to the complicated task of attracting foreign investment to a Venezuelan energy sector hurt by years of officially tolerated corruption, neglected maintenance and a significant brain drain.

The problem for bondholders — such as the Venezuelan Creditors' Committee, a group holding around 13 percent of Venezuela's defaulted debt, which already met the opposition earlier this year to discuss ways to commit to debt restructuring — is that Maduro does not appear to be going anywhere soon. The push to remove Maduro is stalling in the absence of a credible opposition contender for power. This is compounded by the White House's increased focus on Iran, meaning the present government in Caracas is likely to prolong its rule — perhaps by several years.

At the same time, Maduro's continued rule could very well prompt soul-searching in the opposition. The National Assembly, the opposition-controlled legislature that is unrecognized by Maduro's government, tends to change leadership every year. Given that, lawmakers could jettison the opposition's top challenger to Maduro, Juan Guaido, and his U.S.-based negotiating team and search for a new way to accomplish regime change if the dissident leader fails to unseat Maduro by the time his term ends in January 2020.

The Tall Task Facing the Opposition

The diminished outlook for Venezuela's opposition could also stall talks between creditors and the would-be government, as bondholders will be forced to seek new negotiating partners as the country's dissidents jockey to replace Guaido as the prime challenger to Maduro.

The collapse of the effort to oust Maduro will complicate the opposition's hopes of revitalizing Venezuela's energy sector. Though the opposition plans legislative reforms that would give private investors control of oil blocks (a move intended to circumvent the Venezuelan government's lack of capital for joint ventures), the energy sector it might, one day, inherit will be severely diminished. With Maduro still in power and in no mood to pay foreign debt, creditors and claimants will have several more years to pursue Venezuelan energy assets abroad. This means the opposition will confront an even bleaker economic picture even if it manages to eventually unseat the current president.

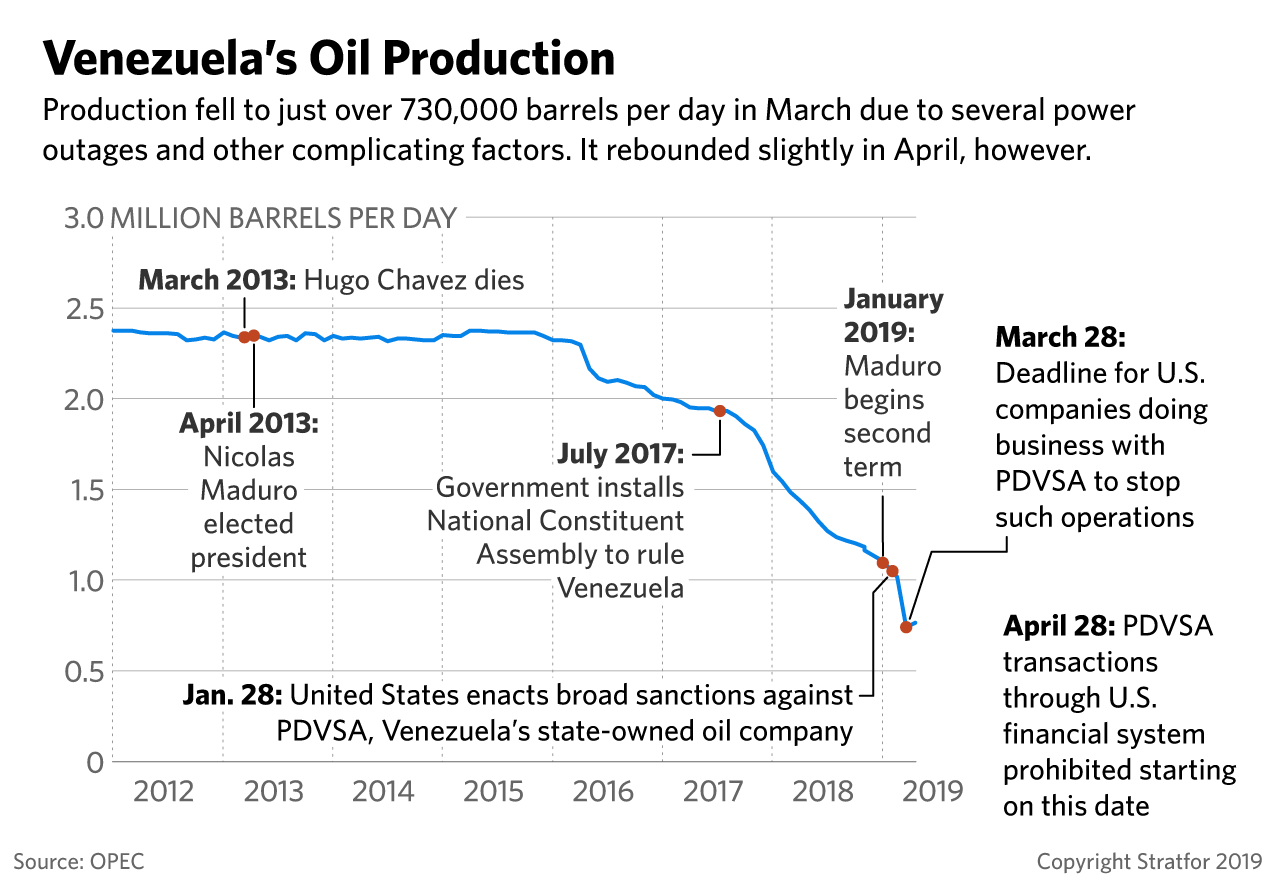

In the short term, the prospect of action against the current administration raises the likelihood that state-owned Petroleos de Venezuela (PDVSA) will face persistent disruptions to its operations as creditors go after assets ranging from cargoes of crude oil to tankers and terminals abroad. Such property includes Venezuelan oil refiner Citgo, which is backed by a bond whose principal payment is due in October. Though Citgo is a private company, a U.S. federal court ruling in 2018 authorized lawsuits against it to collect on PDVSA's unpaid debts given its connections to the Venezuelan state-owned firm. Venezuela's opposition could make the payment if Washington unlocks Citgo funds that it has frozen in U.S. banks, but creditors could still choose to subsequently go after the company's assets.

Ultimately, several more years of unsettled debt brings greater problems for bondholders and potential investors. Some groups of bondholders will have time to consolidate and seek to collect on more Venezuelan assets abroad, particularly property belonging to PDVSA. Unpaid debt will accrue interest, while the total tally of debt that will eventually become subject to negotiation will only grow.

In the end, investors planning to enter Venezuela's energy sector may have to wait until bondholders and arbitration claimants reach tentative deals with an opposition-controlled government prior to pumping substantial funds into the country. Otherwise, they risk wading into the middle of an unresolved legal dispute that will distract future Venezuelan authorities from crucial tasks, such as organizing energy auctions, and prevent PDVSA from reliably accessing badly needed capital for equipment maintenance and talent acquisition. Only energy investors with a high risk tolerance and access to enough capital to overcome the vast investment issues that will be present throughout the energy supply chain will risk entering Venezuela so soon after a government transition.