India's problems with inflation are long-standing. As in many emerging countries, weak institutions have allowed governments in India to impose their will on the central bank. This tends to result in looser monetary policy than the central bank would have implemented independently. Governments prize growth over stable prices, and inflation is often the result. Along with these common challenges, however, India has a few unique troubles. Because the country has a relatively low per capita gross domestic product, its citizens spend a large amount of their income on food. As a result, nearly half of India's consumer price index basket — the regularly consumed items that define prices — is composed of food items. (Food products make up just 14 percent of the United States' CPI basket, by contrast.) These, in turn, depend on the annual monsoon: A poor monsoon can result in a poor yield, sending food prices soaring — and with them, headline inflation. Throw in India's famously creaky infrastructure, which compounds costs and inefficiencies in transporting goods, and you have a recipe for high prices.

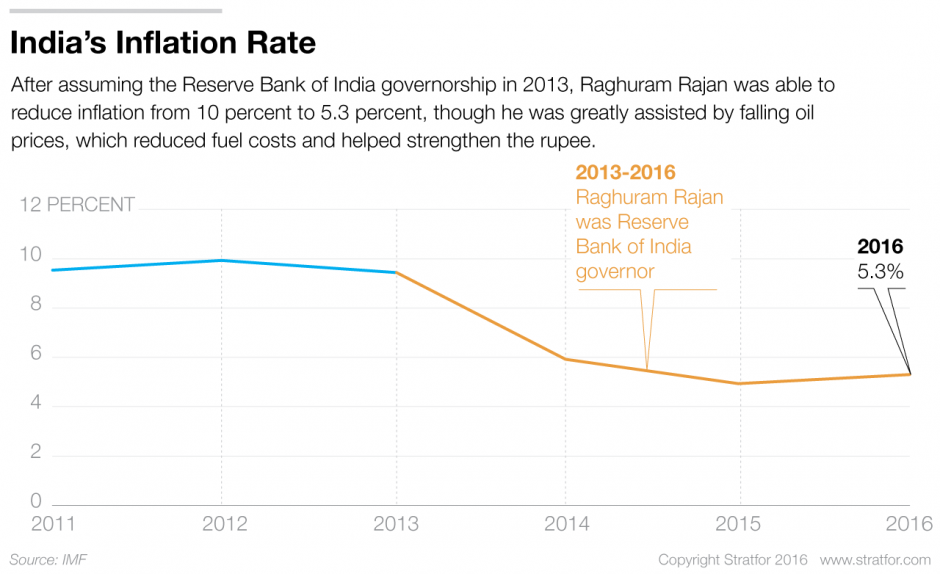

During his time at the helm of the central bank, Rajan proved skillful at managing inflation, cutting it from 10 percent to around 5 percent over the course of his three-year tenure. He was also a celebrity of sorts, having served as the International Monetary Fund's youngest chief economist. The press seized on his renown, portraying him as a maverick who used his prestige to stand up to the government and keep interest rates high to curb inflation.

In reality, though, a combination of factors well beyond Rajan's control also contributed to his successes. Oil prices, for instance, fell sharply while he was in power. Unlike many developed countries, India needed to the prices to decline to hit its inflation target. And unlike many other emerging countries, India is an oil consumer, meaning that a fall in the price of oil was an unequivocal boon. Foreign capital flowed into the country as investors recognized its advantageous situation, buoying the rupee. Furthermore, Rajan appeared to have the government's support, at least at first. When Prime Minister Narendra Modi came to power in 2014, he entertained Rajan's suggestions for modernizing central bank procedures with innovations such as the monetary policy committee and the inflation target.

The outlook for the new monetary policy team, by contrast, is not so rosy. Considering how far oil prices have already dropped, it is hard to imagine them plummeting again as precipitously as they did over the past two years. The monsoon, meanwhile, is as unpredictable as ever. Though 2016's rainfall was relatively healthy, there is no guarantee that this will repeat in 2017. Perhaps most important, Modi is now halfway through his electoral term and will soon have to start thinking about re-election. To bolster its popularity ahead of the 2019 vote, Modi's administration could pressure the monetary policy committee to ease interest rates; already, many members of the ruling Bharatiya Janata Party are calling for cuts. And since half of the monetary policy committee's members are government appointees (as, indeed, is the governor himself), they may well yield to the prime minister. Having assumed their new positions, the central bank's leaders could soon find themselves dealing with a familiar problem: high inflation.