Forecast:

- In the coming months, the stark disjunction between China's stock market boom and its slowing economy will weigh more heavily on stock performance.

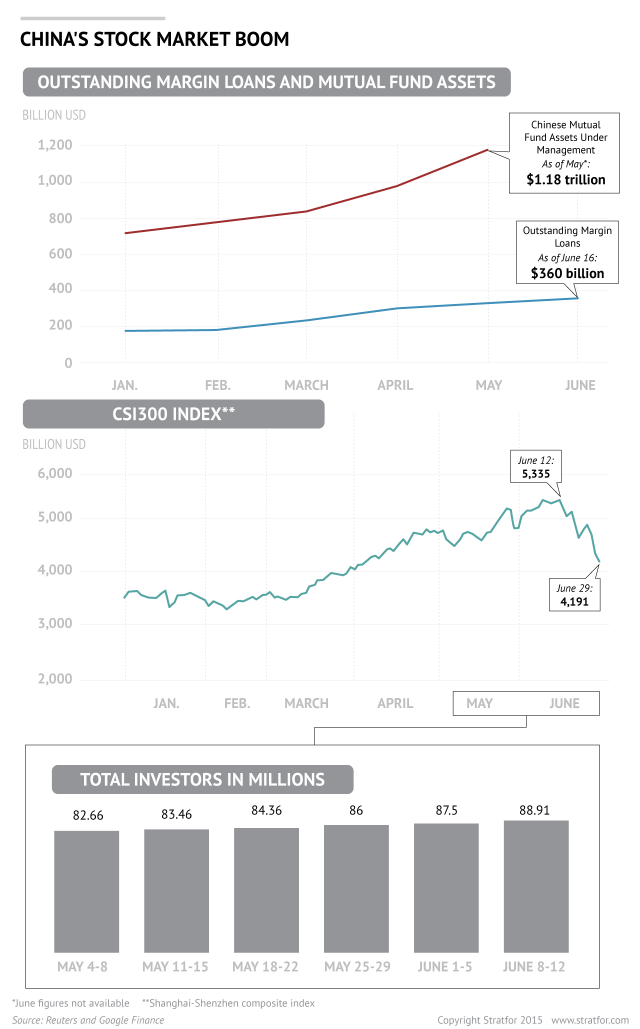

- As the stock market boom inevitably winds down, authorities will struggle to contain financial fires caused by the sharp increase in reliance on margin financing (both formal and "shadow") by stock market investors. The volume of outstanding margin loans is too small to trigger a systemic crisis, but temporary liquidity crunches cannot be ruled out.

- The eventual decline of the stock market, combined with the continued slowdown of property markets across China, will leave ordinary Chinese with fewer options for investing their savings.

The Shanghai Composite Index, which tracks the performance of stocks on China's largest exchange, fell 3.3 percent on June 29, compounding a 7.4 percent drop June 26 — the largest single-day decline since 2008, when Chinese stocks were in the midst of a global financial crisis-induced collapse. Days of sustained falls, even as the country's central bank further cut reserve requirement ratios and interest rates, have reduced the Shanghai exchange more than 21 percent from its June 12 peak, officially making it a bear market. It is unclear whether the fall will continue or, as has happened several times in recent months, whether it will stabilize or even reverse itself in the weeks ahead. But the sharp declines over past weeks cast a spotlight on the increasingly glaring gap between China's buoyant equities and the reality of its continued, and in many ways deepening, economic slowdown.

There was an extraordinary boom in Chinese stocks over the past year. In the 12 months since June 2014, when the boom began, the combined market capitalization of the Shanghai and Shenzhen exchanges rose more than 140 percent. Since early May alone, more than 5 million new investors, most of them ordinary Chinese, have entered the market, bringing the total number of investors to 90 million. Over the past five months, total assets under management at China's mutual funds have nearly doubled, from $720 billion to over $1.2 trillion. In November 2014, China overtook Japan as the world's second largest stock market, with a market capitalization of $4.5 trillion. Today, its stocks have an estimated value of around $9 trillion, roughly equivalent to the country's gross domestic product.

Strikingly, however, this dramatic growth has taken place against a backdrop of steady declines across most major indicators in the economy at large. Industrial profits fell 1.4 percent in the first four months of the year, while those across the state-owned sector — which enjoys disproportionately high representation on China's largest stock exchange, in Shanghai — collapsed by nearly 25 percent. Profits are rising among private sector businesses, but at 6.1 percent in the January-April period, their annual growth pales in comparison to concurrent gains in the Shenzhen index, on which private enterprises are better represented. At the same time, growth in fixed-asset investments, which account for nearly 50 percent of China's GDP, has fallen to its slowest pace since the global financial crisis, and housing construction-related spending — by far the largest component of fixed asset investment — is growing at roughly one-third the pace of a year ago. To be sure, home prices and sales have seen a modest rebound in top-tier markets in recent weeks. And services, high-tech and consumption-related industries continue to grow at a stable rate. But these gains are far from sufficient to support nationwide GDP growth at the government's 7 percent annual target, let alone to explain the stupendous performance of China's equity markets in recent months.

A confluence of factors accounts for the sharp growth in Chinese equity markets over the past 12 months. Excitement over China's nascent high-tech sector, along with strong growth in consumption and services industries, has undoubtedly contributed to the boom. But these factors alone do not fully account for the rapidity and scale of gains made across the board on both of China's leading exchanges, nor for its coincidence with slower growth across most of the country's industrial sector. Rather, the current stock market boom must be understood in relation to two other factors: China's regime of strict capital controls and the decline, starting in March 2014, of the real estate sector.

Expansion in China's Stock Markets

A defining feature of China's financial and economic development over the past three decades has been the government's tight control over the flow of capital in and out of the country. For most of the Reform and Opening period, individual Chinese were prohibited from investing overseas. This has changed somewhat in recent years, in part in an effort to better regulate cross-border capital flows and to combat illicit capital flight. But even today, the vast majority of overseas Chinese investment comes from state-owned enterprises and high net-worth individuals, many of them Party officials or affiliates. Ordinary Chinese by and large are barred from parking their capital and seeking returns beyond China's borders.

Domestically, partially by design and partially because of a lack of financial depth (a legacy of the Mao era, during which securities were outlawed), ordinary Chinese have traditionally had few avenues for investing their savings. Until the late 1980s, they had two options: to deposit savings in state-owned banks, where returns consistently trailed inflation, or to keep them under their mattresses, where returns were even worse. The reason for this arrangement was simple: decades of self-isolation from global trade and financial markets made China in the 1980s an extremely capital-poor economy. And since the government owned the economy, and thus bore sole responsibility for raising and investing funds, it had to ensure it could capture as much of the population's wealth as possible. The easiest way to do this was to give ordinary Chinese no choice but to put their savings in state-owned banks.

China's earliest stock exchanges emerged organically in the late 1980s in cities like Shenzhen and Chengdu in an environment of extraordinary (and short-lived) political openness, rapid growth in private sector industry (which for the most part lacked access to state-controlled funds), and rising demand for higher returns from a population getting its first taste of capitalism in decades. By the early 1990s, however, these earlier exchanges had largely been co-opted by the state and transformed into a nationwide platform — with the newly created Shanghai exchange at its center — for raising capital for the state sector. Ordinary Chinese seeking new places to invest their savings cared little whether the exchanges targeted smaller private firms (as the original Shenzhen exchange did) or larger state-owned firms (as Shanghai, which became the model for other markets nationwide, did), so long as the returns were potentially greater than what might be earned on a commercial bank deposit.

This process coincided with the creation and expansion of commercial urban real estate markets in the mid-1990s, which provided another opportunity for ordinary Chinese to invest their savings. For a combination of social, cultural and policy reasons, and in part because of the lack of transparency and high volatility in China's increasingly state-centric stock markets, the development of the commercial real estate sector vastly outpaced that of stock markets in the 1990s and early 2000s. Stocks were a useful additional means of channeling the population's wealth into state entities, but they were not critical to the state's financing efforts. Indeed, in some ways the development of the stock market threatened Beijing's interests because the more deposits that were redirected to stocks, the less that went to banks' coffers. State-owned enterprises continued to rely primarily on banks for funding, and banks relied on consumer deposits.

The current expansion in China's stock markets is by no means the first, nor even the biggest, since official exchanges were opened in 1990, but it is in many ways the most significant. It comes amid the slowdown of China's decade-plus real estate boom and at a time when ever more Chinese seek means to protect and grow their savings. For the past 10-15 years, and especially since 2008, real estate has been not only the single most important industry in China but also by far the leading investment destination for ordinary Chinese seeking high returns on their savings. This speculative investment activity, much of it fueled by state-backed credit, sustained the extraordinary proliferation of housing markets across the country, and in doing so played a crucial role in maintaining high rates of employment and social stability in the wake of the global financial crisis.

While China's property sector was booming, ordinary Chinese had comparatively little incentive to invest in the stock market. In the 2000s, China's exchanges became notorious for their dysfunction and volatility because of lack of transparency and poor oversight of the initial public offering process. By 2006-2007, the last major boom period, they had come to be viewed by most ordinary Chinese as akin to the lottery — a far cry from property, which generated seemingly never-ending profits and had the benefit of being a fixed asset. Over the past several years, however, the government has gradually introduced a number of reforms aimed at professionalizing the country's biggest exchanges, including reforming the initial public offering process, strengthening the national securities regulator, and slowly opening Chinese stocks to Hong Kong and international investors.

The redevelopment of China's stock markets coincided with the slowing of China's housing market, and this convergence — combined with the proliferation of communications technologies that allow far more people to connect to markets than ever before — has underpinned the rapid growth of the Shanghai and Shenzhen exchanges over the past 12 months. In short, with real estate no longer capable of providing the returns it once did, ordinary Chinese have turned to stocks. For Beijing, this is in many ways a welcome development. As long as the market remains buoyant, it is providing a much-needed source of financing to thousands of Chinese companies, both state-owned and private, at a time when the government is working desperately to curb the economy's dependence on state-backed credit. At the same time, insofar as it allows ordinary Chinese to expand their wealth, it can be a useful tool of social management at a time of slowing growth, heightened concern over local government and corporate debt risks, and increased political uncertainty.

Growing Risks

But as has become clear in recent weeks, China's stock markets are increasingly vulnerable to the sort of debt-fueled speculative activity that drove the country's housing boom into bubble territory and that has made the process of deflating that bubble so treacherous both economically and politically. One key difference between the ongoing boom and that of 2006-2007 is the emergence of margin financing, or loans used to invest in stocks. Before 2010, China had no formal channels for individual investors to take out loans for investment in the stock market. Certainly margin loan-like tools existed, but on a highly informal and ad hoc basis, disconnected from the state-owned banking sector and thus posing little threat to national financial stability. When the market crashed in 2008, it wiped out the personal savings of many millions of investors, but the lack of leverage minimized the risk of financial contagion.

There has been a remarkable surge in margin financing over the past five months, both formal and informal. Since January, the value of outstanding margin loans has doubled to roughly $350 billion. Informal margin financing has an estimated value of between $80 billion and $160 billion. Though small compared to the total value of China's stock market or assets in the state-owned banking sector, the surge in margin financing both formal and shadow raises the risk of a liquidity crunch — and possibly wider financial contagion — if and when the market does enter into terminal decline. In recent weeks, the government has moved to limit banks' exposure to margin loans by raising the minimum assets required to qualify for margin financing and creating a program to facilitate the rollover of margin loans. But these measures, like policies intended to cool China's housing market by tightening the flow of bank credit in years past, could have the side effect of driving up demand for informal sources of margin financing.

One outstanding question raised by the fall in stock prices during the week leading up to June 26 is what new investment avenues may emerge if and when the current stock market boom does come to an end. The massive oversupply in China's housing sector makes a significant, sustained recovery in real estate markets beyond a handful of top-tier cities highly unlikely in the next 6-12 months and possibly for years to come. But with capital controls still largely in place and with the government likely to proceed slowly with efforts to liberalize interest rates on bank deposits, it is unclear what other high-return options exist for ordinary and wealthy Chinese alike, not to mention for China's growing industry of institutional investors such as mutual funds. China's population is increasingly attuned to the benefits of investing, and as the economic slowdown begins leading to unemployment in many regions over the coming months, it will be increasingly dependent on it. But Beijing will struggle to provide its populace with new investment opportunities.

Lead Analyst: John Minnich