Forecast

- Spain's recent economic growth is overshadowed by persistently low salaries and an unwanted rise in part-time, temporary work.

- Despite a rise in exports due to internal devaluation, the trade deficit continues to grow.

- Political parties promising economic health are losing credit and growing more fragmented.

- Because of a divided government, Spain will not be able to maintain its path of economic recovery.

Six years into the economic crisis, the Spanish economy is finally seeing some decent growth. During the first quarter of the year, Spain's gross domestic product grew by 0.9 percent and, as Madrid recently said, it expects annual growth to be close to 3 percent. The country has also seen a drop in its unemployment rate, with Eurostat reporting 25.1 percent a year ago and 23 percent in March. The government in Madrid attributes the improvement in numbers to EU-sponsored policies applied by the conservative government. The reality, however, is a bit more nuanced.

The International Monetary Fund recently warned that Spain's GDP remains below pre-crisis levels and will not return to its 2008 level for at least another two years. Spain's job market is also not expected to return to pre-crisis levels anytime soon. According to the IMF, unemployment will still affect one in five Spanish workers in 2020.

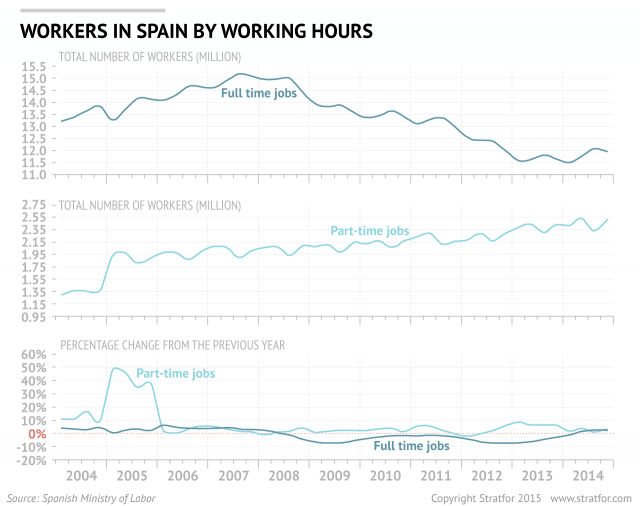

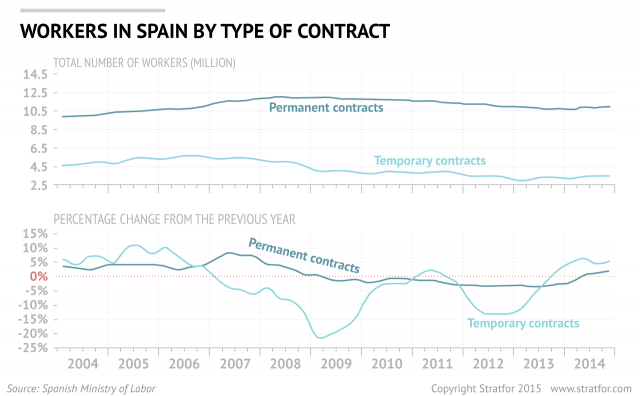

In addition to high unemployment rates, many Spaniards are afflicted by precarious and temporary employment. According to official figures, only one in 10 work contracts signed in March were for permanent positions. The number of temporary contracts is growing twice as fast as permanent contracts. During the first quarter of 2015, the number of people working on temporary contracts grew 5.42 percent year-on-year, while the number of permanent contracts grew only 2.71 percent.

Spain is also experiencing a rise in part-time jobs. During the first quarter, the number of people working full-time jobs grew 2.91 percent year-on-year, while the number of people working part-time jobs grew 3.83 percent. Almost two in 10 workers in Spain work less than 35 hours a week. This is not unusual in Europe, with countries such as the Netherlands having higher part-time work rates. However, the situation in Spain is not by choice, and most part-time workers would prefer a full-time position.

Statistics from Spain's Ministry of Employment also reveal the three most common jobs held in the first quarter of 2015 were agricultural laborers, waiters and cleaners. In April, the month tourism season begins in Spain, almost half the new jobs were in hotels — mostly contractual positions set to end later in the year.

Finally, salaries are stagnant. According to the Organization for Economic Cooperation and Development, salaries in Spain fell 1.8 percent in 2014. They continue to progressively diverge from those elsewhere in the eurozone. In 2008, average hourly wages in Spain were 24.3 percent below the eurozone average, and in 2014 they were 27.3 percent below the average. In Greece the change was more dramatic. During the same period, average hourly wages went from 29 percent below to 46.4 percent below the eurozone average.

The Financial Effects of Internal Devaluation

The policies applied by the conservative government of Prime Minister Mariano Rajoy over the past four years are part of what is known as internal devaluation — the attempt to restore international competitiveness by reducing labor costs. Internal devaluations are often seen as an alternative to "traditional" devaluations, which involve monetary policy. Traditionally, Spain would deal with economic crises by manipulating its currency, but this option is no longer available because of the introduction of the euro.

Spain's internal devaluation has had mixed results. According to the Ministry of Economy, exports grew 26 percent between 2008 and 2014. In 2014, Spain's exports exceeded 240 billion euros ($270 billion) for the first time. However, the country continues to run a trade deficit, which, after decreasing during the recession between 2008 and 2013, began to grow alongside the economy in 2014.

Spain's domestic consumption is also improving. The real estate and automobile sectors have seen a timid recovery after suffering massive decreases during the crisis. However, because of stagnating salaries and pervasively high unemployment rates, Spain may not be able to maintain domestic demand. Additionally, private debt continues to be a serious threat to the Spanish economy. Spain's private debt is at around 178 percent of GDP. This means that Spanish banks will continue to be very cautious when it comes to providing new credit, while many households and companies will delay consumption and investment decisions.

Although Spain's public debt is not as dramatic as that of Greece or Italy, it has grown steadily since the beginning of the crisis and is nearing 100 percent of GDP. The government in Madrid has slowly reduced its deficit and has pressured regional governments to do the same. But the positive environment created by the European Central Bank has led to lower interest rates for countries in the eurozone periphery. As a result, Madrid increasingly relies on sovereign debt for financing. Low interest rates are certainly helpful, but very low inflation rates are causing Spain's relative debt burden to grow.

Spain's recent economic growth is explained by two additional factors. First, tourism is one of the few activities that continued to grow during the crisis. Foreign visitors chose Spain because of falling prices in the sector and political instability in competitor destinations (including Turkey, Egypt and even Greece). Second, Spain, like most of Europe, has benefited from low oil prices and a relatively cheap euro. Madrid cannot count on these external factors to continue indefinitely.

The Political Effects of Spain's Policies

While Spain's internal devaluation has had mixed financial effects, its political consequences are more straightforward. Spain is evolving from a stable, two-party system to a more fragile, multi-party system with complex alliances. As people grow tired of the traditional parties, opinion polls show Spain's political environment is divided into four groups with comparable levels of popular support. The mainstream Popular Party (center-right) and Socialist Party (center-left) are now as supported as the left-wing Podemos and the centrist Ciudadanos. With Spain holding regional elections on May 24 and general elections before the end of the year, distribution of power in the country in 2016 will be very different.

The ruling Popular Party has so far failed to convince voters that the country's economic recovery will be fast, sustainable and felt by all Spaniards. The Socialist Party is struggling to find the balance between promising growth-related policies and defending Spain's commitments to the European Union. Podemos, in the meantime, is losing ground because of internal divisions and the rise of Ciudadanos, a party that attracts protesters but resists using the inflamed rhetoric that scares voters away from Podemos.

This will result in fragmented parliaments in many of Spain's autonomous regions and, most notably, at the national level. Although the next government in Madrid will be met with a slightly improved macroeconomic situation, abnormally high unemployment rates and a rise in part-time and temporary positions will continue to threaten the country's economic recovery, and decision-making will become more complex as the year progresses.