Gulf infrastructure investments designed to bypass the Strait of Hormuz will face constraints from regional distrust, uncertain commercial viability and, for many, years-long construction timelines that largely leave regional countries dependent, to varying degrees, on the Strait of Hormuz despite ambitions to diversify export routes. On May 21, Bloomberg reported that Saudi Arabia's Public Investment Fund (PIF), the kingdom's sovereign wealth fund, is considering consolidating its logistics projects into a single, large portfolio, to streamline its transport and supply chain ambitions in a process that has gained urgency since the start of the Iran war — part of a regionwide pattern of renewed discussions on developing regional infrastructure to bypass the Strait of Hormuz. Meanwhile, on May 15, Abu Dhabi National Oil Company (ADNOC) said it was expediting a second West-East pipeline, projected for a 2027 launch, which will double the United Arab Emirates' oil export capacity via its Port of Fujairah along the Gulf of Oman. The announcements were just the latest of war-driven infrastructure and logistical adaptations that Gulf Co-operation Council (GCC) countries have taken to reroute goods that would normally be exported through the strait, such as the surge of crude oil exports through Saudi Arabia's East-West Petroline to Yanbu Port on the Red Sea and the temporary, high-volume use of large-scale trucking operations across the Arabian Peninsula. The United Arab Emirates has also been leveraging Omani ports, such as Sohar, for redundancy (like by rerouting Emirates Global Aluminum exports) while advancing the domestic build-out of an emergency supply route through Khor Fakkan to Abu Dhabi and Dubai. Additionally, the now three-month-long closure of Hormuz has revived interest in broader trans-regional projects, like the reactivation of the Arab Gas Pipeline (via Jordan and Syria to address Lebanon's energy shortages and eventually link into Turkey), proposed plans for a Kuwait-Iraqi-Turkey energy corridor, an India-UAE-Oman undersea pipeline, and long-term consideration of land connections like reviving the historic Hejaz Railway (which once ran from Turkey to Mecca).

- Despite an April 7 ceasefire, neither Iran nor the United States has abandoned its mutual blockades that have largely closed the Strait of Hormuz, shutting in exports from ports based in the GCC's eastern littoral region. Only a handful of ships have managed to leave the Gulf, down from the 100-150 that would normally cross daily before the war.

- With the United Arab Emirates' main ports in Jebel Ali and Port Khalifa isolated, it has become increasingly reliant on its non-Hormuz port at Khor Fakkan, as well as trucking and flights from Saudi Arabia and Oman's non-Gulf ports to ensure the arrival of food, medicines and consumer goods. The United Arab Emirates is the only Gulf Arab country with ports in both the Gulf of Oman and the Persian Gulf, allowing it to bypass the Strait of Hormuz.

- Meanwhile, the head of Kuwait's state-owned national oil company, Kuwait Petroleum Corporation, is reportedly in talks with Saudi Arabia and the United Arab Emirates for potential pipelines, as interest remains high in finding bypasses.

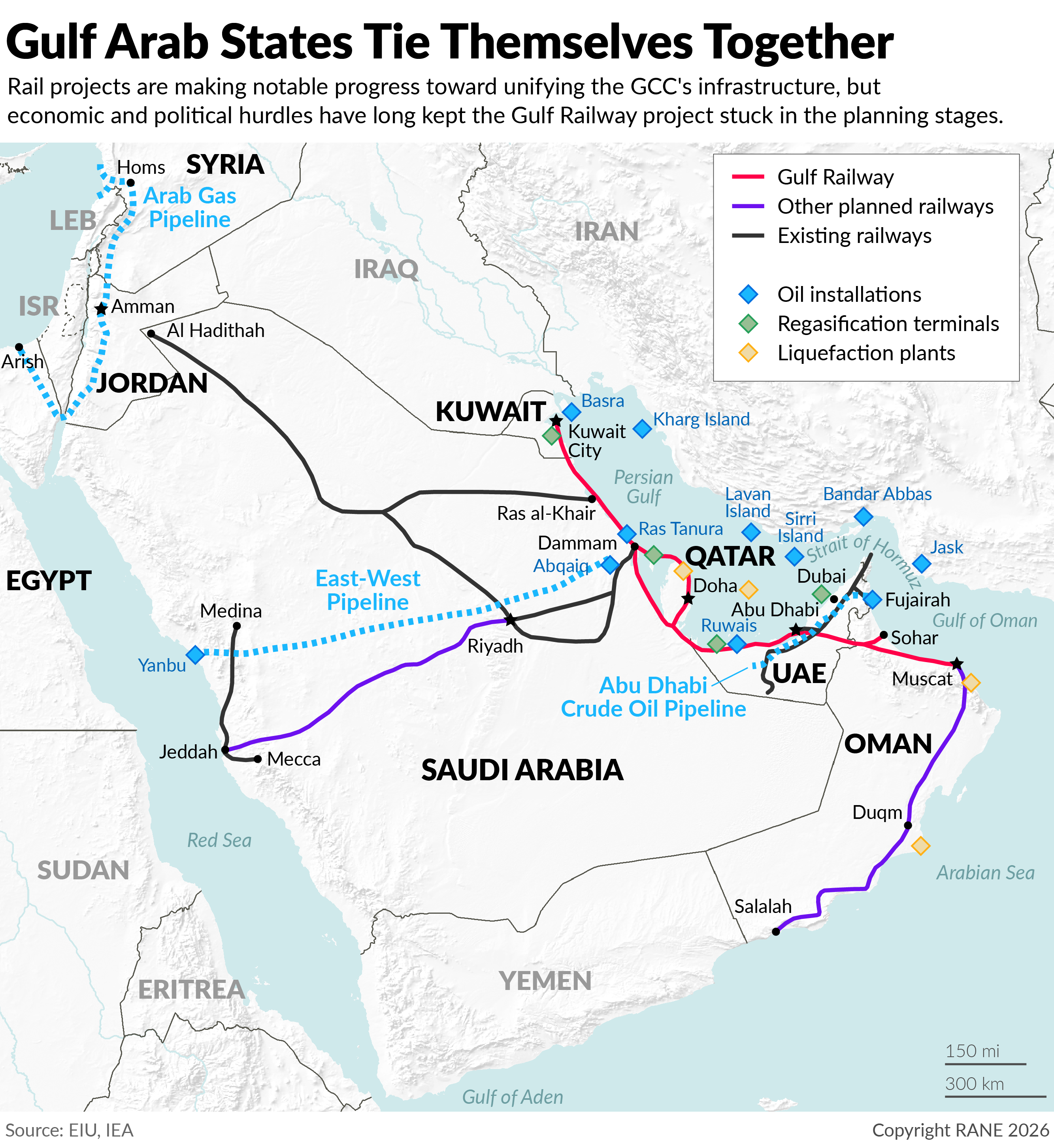

GCC countries have long leveraged their geographic position between Asia and Europe to establish themselves as key logistical nodes for global trade, but they also have a long history of internal competition and conflict that has undermined regional connectivity and infrastructure integration. The region's infrastructure strategies have evolved over decades of ambitious development, led by the United Arab Emirates' construction of massive facilities such as Jebel Ali Port, which other GCC nations have since sought to emulate. A key part of this strategy has been to connect Europe and Asia, with regional ports serving as stopovers, while also exporting energy to both of these regions. To mitigate assumed Hormuz-related risks before the war, Saudi Arabia and the United Arab Emirates constructed east-west oil pipelines, though these remain only partial replacements due to higher costs, lower capacity and the historically low perceived likelihood of a prolonged blockade of the strait that would necessitate the use of alternative export routes. Meanwhile, broader rail connectivity has frequently stalled, with projects such as parts of the United Arab Emirates's high-speed rail line canceled during the 2015 oil bust. Moreover, regional instability, including the Syrian Civil War and chaos in Iraq after the U.S. invasion in 2003, has isolated the peninsula from Turkey and the Mediterranean via land. Further, a Mediterranean route via Israel remains blocked by a lack of normalization with Saudi Arabia, while any revival of the historic Hejaz Rail line would require a complete rebuild to address its antiquated Ottoman-era gauge. Finally, the legacy of the 2017-2021 Qatari blockade — in which Saudi Arabia, the United Arab Emirates, Bahrain and Egypt cut off air and sea connections to Doha — continues to fuel deep-seated distrust, highlighting the persistent risk of GCC states weaponizing shared infrastructure against one another.

- The region's reliance on ports that are close to coastal urban centers has also disincentivized a region-wide trucking and highway network similar to that of the United States, making land routes more expensive and inefficient during a time of crisis. Rail lines, meanwhile, have often been seen as uneconomical or largely prestige projects given that sea shipping remains cheaper.

- Most GCC-wide initiatives — like a bloc-wide customs union, a common currency and a common defense policy — fail to make headway due to intra-GCC distrust. Though a customs union has nominally been in place since 2015, individual states create exceptions, like Saudi Arabia's designation of UAE free trade zone goods as non-GCC products.

Infrastructure projects that can be developed within one country, like the United Arab Emirates, Saudi Arabia and Oman, are likely to gain more momentum in the coming months, though these projects will still face financial headwinds and logistical tradeoffs, and will leave the other GCC states dependent on their larger neighbors. Given intra-GCC competition and other challenges in advancing infrastructure projects spanning multiple countries, the projects that are most likely to make near-term progress are those within a single country. The United Arab Emirates is expected to develop the Khor Fakkan deep-water port as a primary alternative to its isolated Jebel Ali and Port Khalifa installations, modernizing and expanding it despite the geographic difficulties posed by the Hajar mountains. This port expansion will be supplemented by increased rail and trucking capacity, although Fujairah's challenging geography prevents it from fully offsetting the capacity of Jebel Ali or Port Khalifa once shipping through the Strait of Hormuz stabilizes. Similarly, Saudi Arabia will prioritize internal projects, including potentially new east-west pipelines, accelerating the completion of the Jeddah-Dammam east-west rail line, while investing heavily in at-scale trucking and highway construction to support its railway network. Oman, meanwhile, will likely deepen its own internal infrastructure projects, like the development of ports at Sohar, Duqm, Sallalah and Muscat, but the country's comparatively smaller national budget will limit the size of these projects. All of these and other projects will also require state financial backing and guarantees to attract significant private investment, adding another challenge. And, regardless, such projects would leave the smaller Gulf Arab states — Qatar, Bahrain and Kuwait — still trapped behind Hormuz, incentivizing them to find other alternatives that will have to go through their neighbors.

- Oman and Saudi Arabia are both enjoying windfalls from higher oil prices, providing them with greater flexibility for future infrastructure projects. Oman's budget has increased by more than 60%, whereas Saudi Arabia has seen a more modest boost due to the continued export limitations at its Hormuz-related ports. In contrast, shut-in nations like Kuwait, Bahrain, and Qatar are facing budgetary squeezes. Similarly, the United Arab Emirates is experiencing fiscal strain, as its exports via Khor Fakkan remain significantly below pre-war levels.

- ADNOC's CEO Sultan Al Jaber said on May 21 that he does not expect oil flows to normalize until early 2027, even if Iran immediately halts attacks on Hormuz shipping. This suggests that, at least from the United Arab Emirates's perspective, the current disruption's duration provides sufficient commercial justification to develop backup infrastructure. The United Arab Emirates has also become more hawkish toward Iran since the war began, suggesting it is preparing for future Hormuz-related disruptions and is seeking to build greater supply chain resiliency.

- Alternative export routes that bypass the Strait of Hormuz are not inherently immune to Iranian or Iranian proxy attacks. For instance, Iran attacked Saudi Arabia's East-West pipeline and struck Omani ports multiple times over the course of the recent conflict.

Kuwait, Qatar and Bahrain, which are fully trapped within the Persian Gulf, as well as the United Arab Emirates's non-Hormuz-adjacent emirates like Abu Dhabi and Dubai, will remain incentivized to develop infrastructure that bypasses the Strait of Hormuz, though the viability of these alternative routes will be constrained by political, economic and security challenges. Kuwait could seek to develop pipelines, railways and expanded highways through Saudi Arabia to reach its Red Sea ports. However, this strategy would face significant political hurdles in securing funding from its divided parliament, as well as economic hurdles stemming from the country's growing debt burden. Furthermore, Kuwait would likely resist allowing Saudi Arabia to finance or manage these corridors, fearing an expansion of Saudi influence over the Kuwaiti economy. Developing infrastructure that crosses through Iraq, Kuwait's other neighbor, will similarly prove difficult. Although Kuwaiti-Iraqi relations have improved, both countries face economic constraints that hinder large-scale pipeline, rail and highway investments, and Iraq's security challenges make infrastructure projects both riskier and more expensive. Additionally, pro-Iranian factions within the Iraqi government may obstruct such projects because of Kuwait's alignment with the United States. Qatar is also trapped behind the Strait of Hormuz, but is much more skeptical of integrating its infrastructure more deeply into Saudi Arabia, which blockaded it in 2017-21 and may weaponize economic connections in the future over other disputes. Bahrain, on the other hand, is already closely aligned with Saudi Arabia and is likely to deepen infrastructure ties with the kingdom, even at the expense of its already comparatively limited sovereignty. As one of the GCC's most fiscally challenged states, Bahrain may benefit from the deepening Saudi-Emirati competition as both seek to boost the Sunni monarchy there, with the United Arab Emirates potentially offering Bahrain intra-Gulf trade route options that would cross through the United Arab Emirates to Khor Fakkan, while Saudi Arabia competes with its direct land connection to Bahrain itself.

- Kuwait and Iraq have long planned to develop a gas pipeline from Ruamila to Kuwait to address Kuwait's gas shortages. But despite its appeal on paper, the project has struggled to become viable due to high costs, insecurity in southern Iraq and pricing disagreements.

- In GCC disputes, Saudi Arabia has historically weaponized border controls to earn concessions or exert influence. In 2009, for example, the kingdom refused to recognize Emirati identity cards for border crossings to undermine travel and trade.

- The Gulf region also has a history of canceling or delaying large-scale projects. The United Arab Emirates delayed its own railway network after the 2015 oil crash, while Saudi Arabia recently announced it would not resume work on its Neom mega-city project until 2030.

GCC efforts to connect Asian and European markets through pipelines, railways and other logistical infrastructure will continue to face economic and political hurdles, making few of these projects viable. There is intense speculation that Gulf states might back the reconstruction of the Hejaz Railway or the rehabilitation of the Arab Gas Pipeline to tie in their own infrastructure to routes that reach Turkey and, thereby, Europe. However, both projects rely on significant stability in Syria, which is still undergoing a shaky political transition and faces large security vacuums. A project to develop the Hejaz Railway for large-scale freight transport would also need to have commercial viability well beyond the timeline of the Hormuz crisis, given that the route is currently obsolete. While such a project could be pursued as a prestige initiative to strengthen ties between Turkey and Saudi Arabia as the countries align their regional strategies, the railway is unlikely to be a significant part of the GCC's strategy to bypass the Strait of Hormuz. In addition to insecurity, the Arab gas pipeline has also suffered from inadequate maintenance, which has increased the cost of rehabilitating it. Other pipelines, such as a route between Oman and India, are logistically and technologically feasible but similarly face major economic hurdles, with no certainty that they will be worth the investment, given the current assumption that the Hormuz closure is not permanent. This will likely leave most Hormuz-related emergency projects in the planning stage, with only prestige projects that have significant political will behind them likely to be implemented.

- The Hejaz Railway was built with a narrow track gauge of 1,050 millimeters (mm), and the few functional areas continue to use the same gauge. Saudi Arabia's railways use a standard 1,435 mm gauge, meaning the Syrian-Jordanian sections would have to be completely rebuilt.