Editor's note: The first part of this report explored the impact that a continued stalemate or the war's evolution into a frozen conflict would have on Ukraine's investment profile. Part 2 explores the more extreme options of a comprehensive peace agreement or a severe escalation of the war.

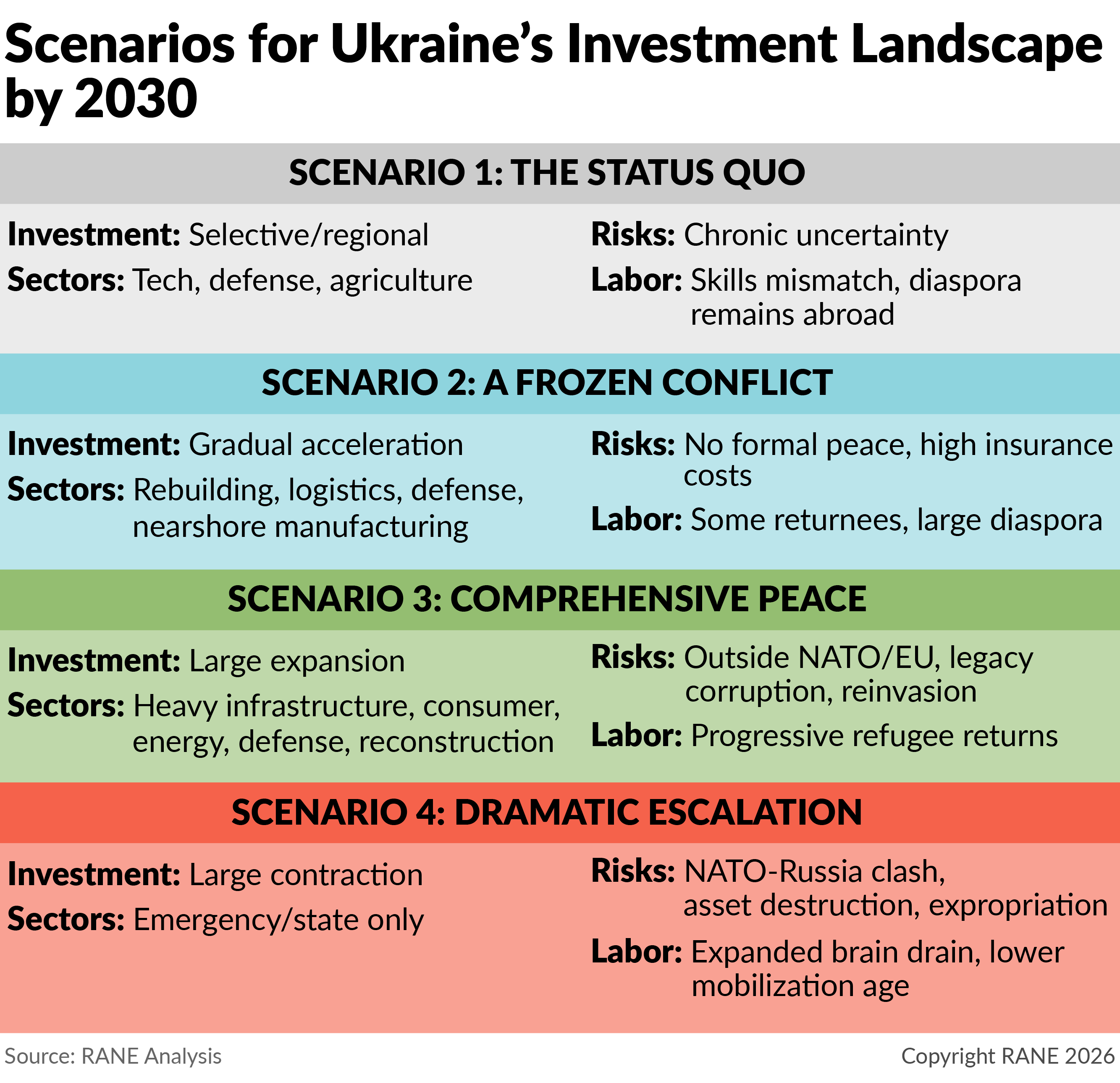

Scenario #3 - A Comprehensive Peace Agreement

In this scenario, Ukraine and Russia reach a comprehensive peace deal accepted by Kyiv, Moscow and the broader international community. Such a deal would likely include Russia retaining all territories currently under its control and potentially securing additional portions of the Donbas region and the Zaporizhzhia and Kherson provinces as part of a negotiated settlement. In return, Ukraine would receive modest Western security assurances and continued economic support. However, it would remain outside both NATO and the European Union, either because of political opposition among member states or Kyiv's inability to complete the institutional reforms required for accession. Active hostilities and Russian missile and drone attacks would end. Ukraine would begin transitioning from wartime economic survival toward reconstruction and economic normalization.

This scenario would likely trigger a substantial expansion of investment activity, primarily because the cessation of violence would dramatically reduce operational and physical security risks. In the immediate aftermath of a peace agreement, Ukraine could experience a temporary recession as it transitioned from a war-driven to peacetime economy, with hundreds of thousands of demobilized soldiers returning to the civilian labor market and industry pivoting back to producing consumer goods. Still, the end of Russian missile attacks alone would improve Ukraine's investment profile by restoring predictability to industrial production, logistics, energy infrastructure, transportation networks and urban commercial activity. International investors that had remained on the sidelines during the war would begin exploring market entry, while multinational corporations already operating in Ukraine would likely accelerate expansion plans. Investor sentiment would improve even without formal EU membership if Kyiv remained committed to introducing economic and institutional reforms to meet the bloc's criteria.

Reconstruction would become a dominant investment area. Ukraine's postwar infrastructure needs would be immense, encompassing housing, transport, railways, ports, the electricity grid, water, telecommunications, hospitals and industrial facilities damaged during the war. Foreign engineering firms, construction conglomerates, industrial suppliers and infrastructure investment funds would likely compete aggressively for reconstruction contracts supported by Western governments and multilateral development institutions. The scale of reconstruction financing could create sustained demand for private capital alongside public-sector funding mechanisms. Because of Europe's continued financial and military support during the war, a significant number of contracts would be granted to European companies, but Kyiv would also seek to attract American companies to preserve strong ties with the United States.

Ukraine's defense sector would be one of the country's leading strategic industries, supported by long-term Western security cooperation, domestic weapons production and reconstruction-driven industrial investment. The sector would expand beyond wartime needs into advanced drone systems, cybersecurity, missile technology and joint ventures with European and U.S. defense companies, helping position Ukraine as a major regional defense manufacturing and security hub in Eastern Europe. Foreign direct investment would increase as Western defense firms establish production partnerships, technology transfer agreements and manufacturing facilities in Ukraine to support both regional security demand and long-term NATO-aligned industrial integration.

Manufacturing and industrial relocation would likely become particularly attractive under this scenario. Ukraine's relatively low labor costs, extensive industrial base and proximity to the European Union could position the country as a major manufacturing platform for European supply chain diversification. Investors in automotive components, industrial machinery, chemicals, building materials, food processing and consumer manufacturing would likely view Ukraine as an increasingly viable nearshoring destination, especially as European firms seek alternatives to Asian production hubs amid rising geopolitical fragmentation. Western Ukraine and the Kyiv region would probably emerge as the primary centers for industrial reinvestment, although lingering uncertainty about the potential for future escalation of the conflict with Russia may make companies more hesitant about investing in Ukraine's east and south.

The energy sector could become another significant area for foreign capital deployment. Postwar reconstruction would create opportunities not only to repair damaged infrastructure but to redesign Ukraine's energy system around greater integration with Europe. Renewable energy, nuclear modernization, gas storage, electricity transmission, decentralized power generation and green hydrogen production could all attract substantial foreign interest.

Agriculture would likely experience a major recovery in investment activity as wartime disruptions to logistics and exports disappear. International agribusiness firms, commodity traders, food processors and agricultural technology providers would likely expand operations given Ukraine's structural importance as one of the world's largest grain exporters. However, Ukraine's territorial concessions to Russia could complicate ownership claims and infrastructure access in some of the country's most productive agricultural regions, particularly if parts of southern Ukraine remain under Russian control. Investors would therefore pay close attention to legal frameworks governing land rights, compensation mechanisms and trade access through Black Sea ports. A comprehensive peace deal would also increase the prospects for developing Ukraine's critical raw materials sector, given that a substantial portion of its reserves is concentrated in the east of the country.

The financial sector, real estate market and consumer economy would also likely recover substantially under this scenario. Banks, insurance firms, telecommunications providers, retailers, logistics companies and commercial real estate developers would begin positioning for long-term growth as displaced populations gradually return and domestic consumption rebounds. Urban redevelopment projects in Kyiv and other major cities could become particularly attractive to international investors seeking exposure to postwar recovery dynamics.

Despite this progress, major geopolitical and structural risks would remain even after a peace agreement. The lack of NATO membership would leave lingering uncertainty regarding the credibility of Western security guarantees and the long-term durability of the peace agreement with Russia. Investors would remain aware that the conflict could reignite if political relations between Russia and Ukraine, or Russia and the West, deteriorate again. Even with a formal peace deal, Russian grey zone pressure on Ukraine via physical sabotage, information operations and cyberattacks would likely continue. The fact that Ukraine remains outside the European Union would also slow institutional convergence with European legal and regulatory standards, potentially limiting investor confidence relative to Central European member states. Corruption concerns, judicial reform challenges, governance weaknesses and political fragmentation could become more visible once wartime emergency governance recedes. Finally, while Ukraine would eventually move toward full current-account convertibility and a more open capital account, safeguards would likely remain in place during the early stages of the postwar period.

Labor availability would improve significantly but not return to prewar levels. The end of missile strikes and immediate security threats would motivate large portions of the refugee population to return, particularly those people whose skills are most valuable in a rebuilding economy. To encourage the return of refugees, Kyiv would likely announce an amnesty for men who left the country illegally. This would ease labor shortages and allow for rapid scaling in the construction, manufacturing and infrastructure sectors. However, the return would still be incomplete. A meaningful share of high-skilled Ukrainians — especially in technology, research and corporate roles — would remain in Western Europe or North America due to income differentials and career path lock-in. Over time, labor availability and price would likely become one of Ukraine's key competitive advantages again, especially given its still-large working-age population relative to many EU states, but this would depend heavily on longer-term institutional reform and wage convergence.

Scenario #4 - The Conflict Escalates Dramatically

In this scenario, the war moves from a prolonged war of attrition into a fundamentally more dangerous and systemically destabilizing phase. This outcome could take two distinct but related forms. In the first, Ukraine's defensive lines deteriorate significantly, allowing Russia to achieve major territorial advances, potentially reaching the Dnieper River or even pushing further west into traditionally safer regions. In the second, and more extreme variant, the conflict expands beyond Ukraine's borders following direct confrontation between Russian forces and a NATO member state, triggering a NATO-Russia confrontation. In both versions, the defining feature is a sharp escalation in violence, a breakdown in Europe's security architecture and a dramatic increase in the risk of uncontrolled escalation between nuclear-armed powers.

For investors, this scenario would represent a severe contraction in investable opportunities in Ukraine and a broader deterioration in risk appetite across Eastern Europe. Ukraine would cease to function as a viable investment destination in most conventional senses. Large portions of the country would become physically inaccessible, insurance markets would withdraw coverage for most operational activities and capital markets exposure would likely be frozen or heavily impaired. Any existing foreign assets in Ukraine would face extreme uncertainty, including expropriation risk, destruction of infrastructure or forced evacuation of personnel. Even sectors that had previously shown resilience, such as agriculture, IT services and manufacturing, would be heavily disrupted by infrastructure collapse, population displacement and the breakdown of logistics and energy systems. Capital controls would be significantly expanded.

In the more severe variant involving NATO-Russia escalation, Ukraine would effectively become part of a wider active war theater rather than a standalone conflict zone. Under such conditions, investment decisions would shift from sectoral allocation to pure capital preservation and geopolitical exposure management. International firms would prioritize exit strategies, asset protection and supply-chain rerouting away from both Ukraine and potentially broader Eastern European exposure, depending on the scope of hostilities. Europe would likely experience sharp risk repricing across the defense, energy, insurance and banking sectors, with spillover effects into sovereign bond markets and currency stability in frontier European economies.

Sectors of the Ukrainian economy that were considered attractive under more stable scenarios would either collapse or transform into emergency-state industries. Agriculture, for example, could experience severe disruption not only in production but also in export corridors, particularly if Black Sea access becomes further militarized or infrastructure in the west of the country is damaged. Ukraine's role as a global grain exporter would be severely impaired, contributing to higher global food prices and increased volatility in commodity markets. Industrial production would likely fragment geographically, with remaining capacity concentrated in relatively secure western border regions if they remain operational at all.

Ukraine's energy infrastructure would remain a primary target and critical vulnerability. Large-scale destruction of power generation, transmission systems and fuel logistics would push Ukraine into a prolonged humanitarian and reconstruction emergency rather than an investment-led recovery phase. Any foreign involvement in the energy sector would likely shift from investment to emergency assistance, repair contracts and government-backed reconstruction under wartime conditions. Even these activities would depend heavily on military security guarantees, which would be uncertain or rapidly changing.

Ukraine's technology sector would face similarly severe disruptions. While some remote or diaspora-based operations might persist, domestic IT capacity would likely fragment due to infrastructure instability, workforce displacement and connectivity constraints. Cybersecurity activity could intensify, but increasingly as part of state-directed defense efforts rather than commercially scalable investment opportunities. Foreign firms would likely relocate operations to EU countries, accelerating brain drain and permanently shifting parts of Ukraine's tech ecosystem abroad.

From a broader geopolitical investment perspective, this scenario would trigger a sharp global risk-off environment. A NATO-Russia confrontation in particular would likely generate widespread repricing across global equity, credit and energy markets. Defense sectors in NATO countries would likely experience rapid expansion in production and investment, while energy markets would face severe volatility driven by sanctions, supply disruptions and infrastructure targeting risks. Safe-haven assets would dominate capital flows, with institutional investors likely increasing allocations to U.S. Treasuries, gold and core Western European sovereign debt. For Ukraine specifically, foreign investment would virtually freeze and external private financing would practically disappear. Any future reconstruction plans would be highly uncertain, contingent on the eventual outcome of the conflict, territorial control at cessation and the broader architecture of European security that emerges afterward. Even long-term investors with strategic horizons would likely adopt a wait-and-see posture, focusing instead on scenario optionality rather than active deployment. Ukraine's capital controls would likely become more stringent, as Kyiv could impose emergency restrictions on all capital outflows, currency exchange and cross-border transfers, all of which would discourage foreign investment.

In this scenario, labor availability in Ukraine would deteriorate sharply. Mass displacement would likely accelerate, with millions more Ukrainians fleeing westward into EU countries, compounding the existing diaspora. Moreover, the Ukrainian government would likely lower the compulsory mobilization age (currently 25), further shrinking the civilian labor market. Domestic labor markets would fragment geographically, with remaining workers concentrated in either heavily militarized zones or relatively isolated safe regions in the far west. The most economically productive segments of the workforce — high-skill professionals, entrepreneurs and mobile technical workers — would be disproportionately likely to leave permanently, accelerating long-term human capital loss and further weakening Ukraine's investment attractiveness.