Editor's Note: In the coming year, RANE will analyze the geopolitics of natural resources and raw materials. This series will be published periodically throughout the remainder of 2026; you can find all parts here.

Over the coming years, new extraction technologies, changes in demand and environmental concerns will impact the competitiveness of extraction activities in the lithium triangle. The likely shift to Direct Lithium Extraction (DLE) — a mechanical brine-extraction process that filters lithium in a matter of days, rather than the months required by current brine extraction — is set to have a major impact on the industry. The method is currently in testing, but as it is scaled up for industrial use in the coming years, it could significantly accelerate lithium mining from brine. Though DLE is more expensive than brine extraction, it is less expensive than spodumene extraction, meaning that it could provide Bolivia, Chile and Argentina with the tools needed to increase investment attractiveness, while potentially enabling the region to notably increase annual production. However, the outlook for global lithium demand is less certain, even as the push for the green energy transition continues. This dynamic has been evident in recent years, with lithium prices surging in 2021 and peaking in 2022 at over $80,000 per ton, then dropping as Chinese lithium production surged. The outlook for electric vehicles is a critical component for future demand, as though the total number of EVs sold per year is still growing, the pace of growth is decelerating globally, a trend set to persist at least for the next few years as U.S., EU and Chinese policy shifts reduce the push to purchase electric vehicles. Technological shifts could also unsettle lithium markets. The lithium-ion battery was a major market disruptor for pre-existing battery technologies and fossil fuels; it is more likely than not that at some point in the future, whether it be years or decades, an alternative to the lithium-ion battery will be developed that reduces demand for the technology and consequently the metal. Sustainability concerns could also reduce demand, as lithium is not a renewable resource, raising questions about its long-term viability for the energy transition. This will likely further contribute to the push for alternative energy sources in the coming years, raising the potential for a pivot away from lithium that would further weaken demand. Finally, separate from global demand and sustainability concerns, lithium extraction poses local environmental hazards, including contaminating surrounding soil and water, in some cases poisoning reservoirs with chemicals. Brine extraction also requires significant water resources, which is particularly concerning in Chile, as the country is already experiencing worsening water insecurity. Though experts expect some of these environmental concerns to ease with the wider use of DLE, they will not be entirely defused, making this a long-term point of tension between authorities and local communities.

- The surge in lithium prices in 2022 followed a COVID-related production slowdown in 2020, which resulted in low available supplies as the industry began to ramp back up.

- According to the IEA, sales of electric cars have continued to rise in recent years, reaching above 17 million worldwide in 2024. However, in the United States, growth in EV sales slowed to 10% in 2024, compared with 40% in 2023. Data from Cox Automotive also indicated that EV sales fell by 27% year over year in the first quarter of 2026 compared to 2025. While this is partially due to a broader slowdown in auto sales in the United States, the overall market share for EVs fell by 5.8%. This is at least partially due to the elimination of a $7,500 federal tax credit for electric vehicles, which ended in September 2025.

- The European Union has been at the forefront of government policy pushes for the large-scale adoption of EVs. In 2025, battery-powered EVs accounted for 17.4% of new EU car registrations, up from 13.6% in 2024, according to the European Automobile Manufacturers' Association. Hybrid electric vehicles also accounted for 34.5% of new car registrations in the bloc in 2025, while plug-in hybrids accounted for 9.4%. The European Union is maintaining its broad policy push for EVs, but in recent years, authorities have softened policies. In December 2025, Brussels announced plans to soften emissions rules for new cars, scrapping a proposed ban on combustion engines starting in 2035. EV adoption is all but certain to continue to increase in the bloc in the coming years, particularly amid the ongoing global oil supply shocks caused by the Iran war, but these policy shifts in the European Union will likely still contribute to the broader global deceleration.

- China has consistently had the highest electric car sales among major markets in recent years. In 2024, approximately half of all new car sales in the country were electric, with EV sales growing by 10 percentage points year-over-year in 2023 and 2024. Still, China has phased out some of the measures that initially drove the wide adoption of EVs. Government subsidies for EV purchases ended in 2022, and China is also phasing out its purchase tax rebates by the end of 2027.

- The current most prominent alternative energy technology to lithium-ion batteries being explored is sodium-ion batteries, which some EV makers are already using in their vehicles. Compared with lithium-ion batteries, sodium-ion batteries are cheaper to produce and perform better in cold temperatures, but they are also heavier and have lower energy density.

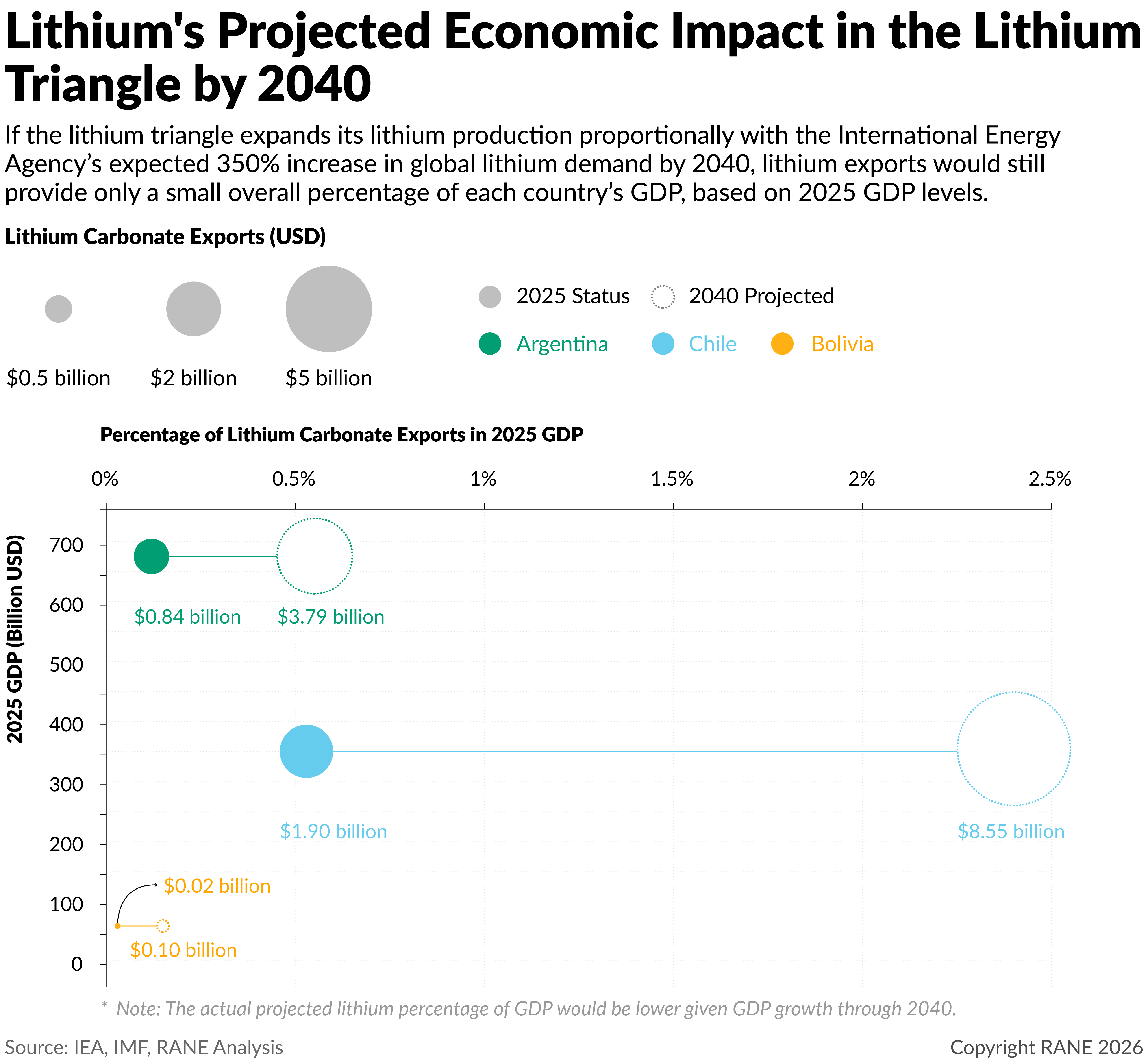

Over the next decade, Chile, Argentina and Bolivia are all set to see lithium extraction expand, providing economic benefits. In the coming years, all three governments will be highly focused on further expanding lithium development to capitalize on demand for the green energy transition and the growing feasibility of DLE. Chile will likely see the greatest benefits, as President Kast is expected to focus on further strengthening the country's already comparatively attractive operating environment. Chile will also have a leg up over the other two countries, given its comparatively low corruption levels, well-developed infrastructure and high-quality lithium resources. Argentina is set to see a significant acceleration in lithium production as well, particularly given its high number of current exploration projects and as economic conditions stabilize under President Milei. Even if the country's Glacier Law reforms do not take effect in their current form, authorities will remain intent on implementing other policies to attract new investment. Bolivia will face the most challenging production ramp-up due to its poor starting position, lower-quality lithium and landlocked geography, all of which will require significantly more investment to reach a comparable level of production to Chile and Argentina. Additionally, though President Paz is intent on expanding lithium extraction, there remains political uncertainty as to future governments. Although the MAS party lost the 2025 elections in a landslide, there is still a substantial left-wing base in the country that could resurge in the 2030 elections and renationalize lithium production, a move that could make the country unattractive to investors. Therefore, while Bolivia will almost certainly see lithium production expand in the coming years, it will remain low in comparison to its regional neighbors, with economic benefits slow to materialize for the country's population. All three countries have the moderate potential to flip back to the left-wing in the next election cycle. But future left-wing governments (even in Bolivia) would be unlikely to implement policies that dramatically hamper lithium production, given its profitability, though they could take steps to expand taxation and environmental regulations. For all three countries, the successful expansion of lithium production will provide economic benefits. Bolivia and, in particular, Argentina will likely use funds from investment and production aid for debt repayments and economic stabilization. These funds will help with infrastructure modernization as well, improving operating conditions in these countries, even for companies outside the extractive industries sector. If invested appropriately, the lithium revenue could also be used to better fund and expand welfare programs for education and poverty reduction, though given the current right-wing tilt of all three governments, this is unlikely in the near term. Still, the overall impact of increased lithium exports on the countries' GDPs would be relatively restrained given current growth expectations. The IEA predicts total lithium demand to reach 928 kilotonnes by 2040, an approximately 350% increase from 205 kilotonnes in 2024. Thus, even if the lithium triangle matches pace with this increase (a possibility for Chile and Argentina, but extremely challenging for Bolivia), it would not provide substantial enough funds to significantly raise GDP, with lithium carbonate exports from Chile rising from 0.53% of 2025 GDP to 2.4% of 2025 GDP in 2040.

- The lithium triangle's current right-wing governments are unlikely to be highly focused on environmental damage from lithium mining, so this will not create major constraints on production, at least for the next few years. Still, environmental concerns will remain a point of contention among left-wing and Indigenous groups in all three countries, meaning that future centrist or left-wing governments could impose new environmental regulations and mining restrictions that hinder lithium development, potentially even suspending some particularly controversial projects.

- Though expanded lithium production would increase government revenue and foreign direct investment, lithium extraction is not a labor-intensive sector, and the likely adoption of DLE would further reduce labor needs. This has the secondary risk of inflaming tensions with local communities, which would be most impacted by the environmental and land-use impacts of the mining activities, but are unlikely to see substantial employment in the sector. Still, as many of these communities are already poor due to their remote location, even a slight increase in employment would be impactful.

A surge in lithium demand significant enough to drive substantial wealth accumulation in the lithium triangle is highly unlikely amid current trends, but if it does occur, the increased revenue would provide further economic benefits. For the lithium triangle to gain more sizeable financial benefits in the next two decades, lithium demand would have to increase by two to four times the IEA's 2040 projections, high enough to raise the metal's price and trigger a greater push for investment in extraction and accelerated production. Such a monumental surge in demand is unlikely, given the potential for new technologies to supplant lithium-ion batteries, ongoing efforts to recycle lithium and uncertainty surrounding future energy transition efforts. However, this low-likelihood scenario could occur if the United States and China significantly expand competition over lithium triangle resources, which could happen if an alternative to lithium-ion batteries is not developed in the coming years and if there is a substantial ramp-up in focus on the green energy transition (particularly within the United States). This competition already exists to a limited extent, with Chinese companies investing heavily in Argentine lithium supplies as well as regional logistics infrastructure, and the United States intent on expanding access to critical minerals and reducing Chinese influence in Latin America. Increased U.S.-China competition would provide Argentina, Bolivia and Chile with greater wealth that would allow for more extensive welfare programs aimed at reducing significant income inequality and poverty levels, which have topped 20% in Argentina and Bolivia. It would also provide funding for the lithium triangle to expand domestic lithium-ion battery manufacturing, which is currently minimal across all three countries. Stronger domestic manufacturing would more closely integrate Argentina, Bolivia and Chile into global supply chains for automobiles and energy cells, creating more jobs that further benefit local populations. Still, outside the lithium triangle, this increased U.S.-China competition would also mean greater costs for companies with supply chains dependent on lithium, potentially shutting out smaller-scale buyers and raising the cost of electric vehicles and other lithium-dependent products. Prices would likely be more prohibitive for smaller consumer electronics companies, as automotive and tech companies have more money to spend in a competitive market.

- By way of comparison, copper production has been a major driver of Chile's economic development over recent decades, with copper ore and concentrates accounting for over half of Chile's exports ($35 billion) in 2025. In contrast, lithium currently accounts for only 10% of Chile's GDP, and to reach levels comparable to copper, demand for lithium carbonate would need to reach approximately 3,857 kilotonnes, more than four times the current IEA demand estimate for 2040.