Editor's Note: In the coming year, RANE will analyze the geopolitics of natural resources and raw materials. This series will be published periodically throughout the remainder of 2026; you can find all parts here.

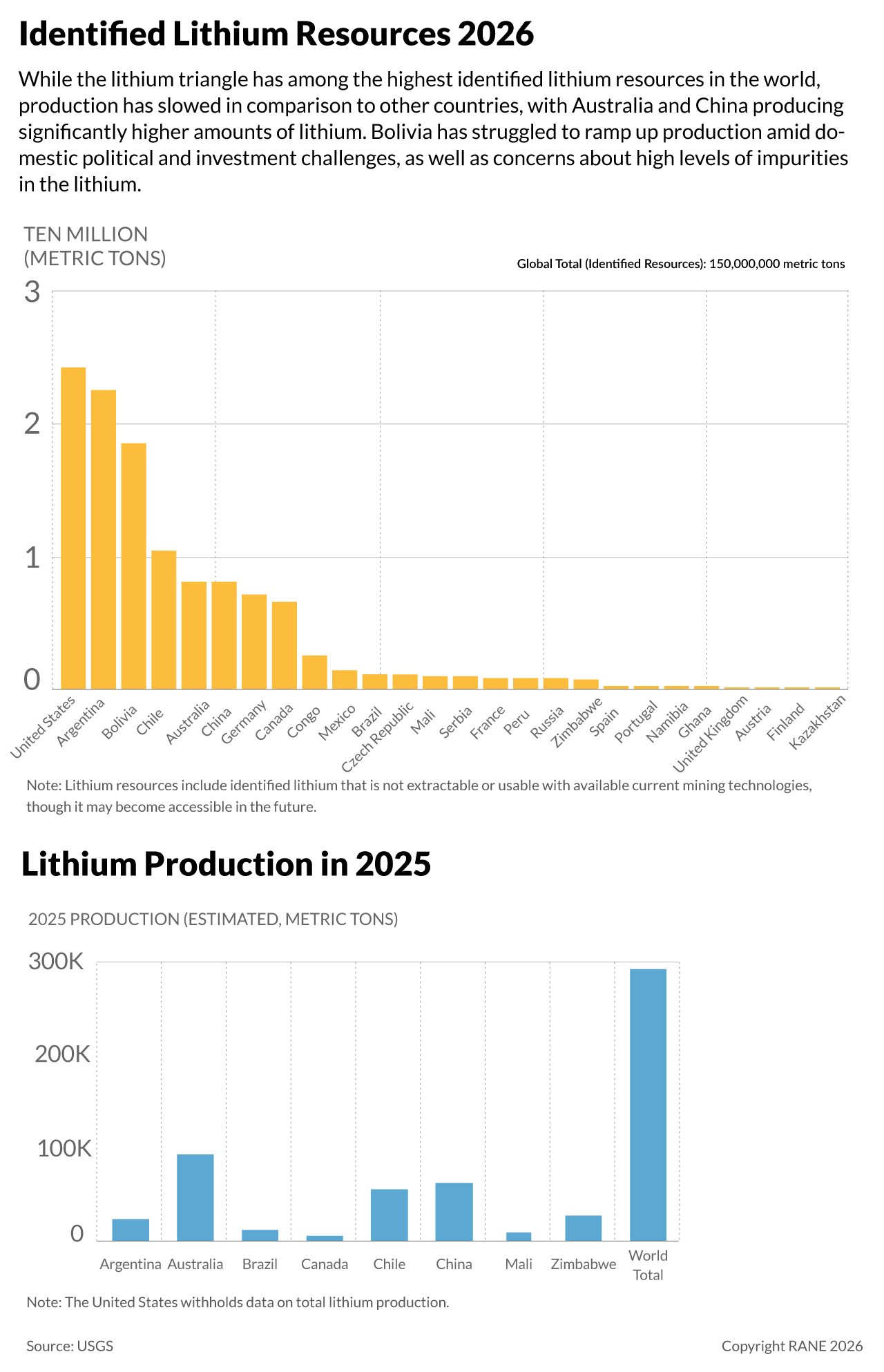

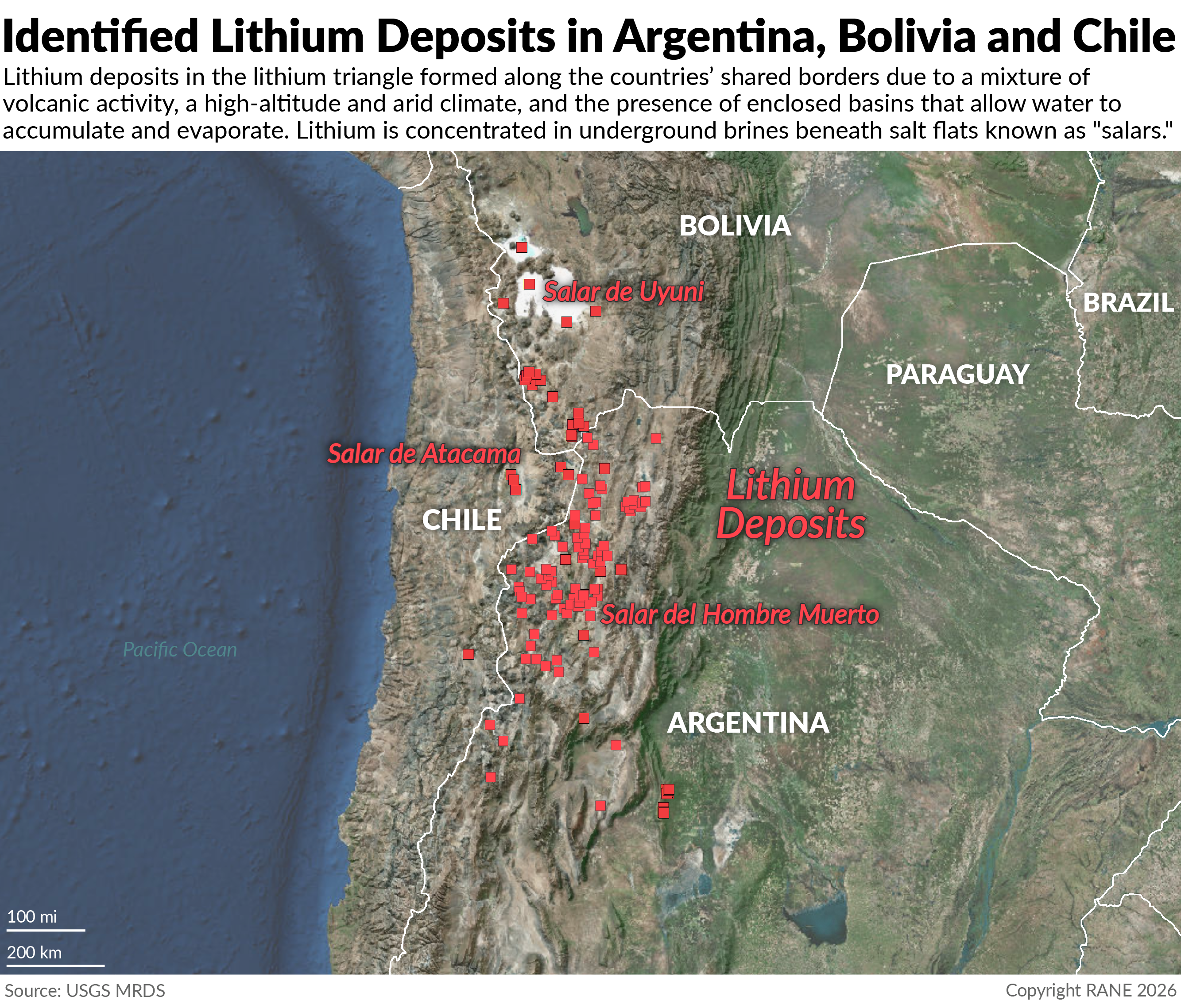

The "lithium triangle" countries of Argentina, Bolivia and Chile are poised to benefit from expected rising lithium demand in the coming years, but they are unlikely to see a substantial surge in wealth without a more monumental market change. The global shift toward renewable energy and technological advancements has significantly increased demand for specific metals and minerals. Notably, lithium demand has surged since the 1990s due to its vital role in lithium-ion batteries for electric vehicles, energy storage systems and, more recently, backup power for data centers. According to 2026 data from the United States Geological Survey (USGS), the salt flats in South America's so-called "lithium triangle" — comprising Argentina, Bolivia and Chile — alone contain 42.6% of the world's identified lithium. But while this concentration of "white gold" has sparked intense international interest and hopes for regional economic growth (particularly for small Bolivia), extraction has been slowed by market fluctuations, demand shifts and local operational hurdles. However, the recent election of right-wing governments in all three nations suggests upcoming policy changes that may alter the region's outlook.

- According to the International Energy Agency (IEA), total demand for lithium reached 95 kilotonnes in 2021 and 205 kilotonnes in 2024.

- Lithium is primarily sold as lithium carbonate and lithium hydroxide. Lithium carbonate is cheaper, more stable and easier to store and transport. Lithium hydroxide is produced by further processing lithium carbonate, making it more expensive to manufacture, but it also enables better-performing batteries.

- Approximately 65% of the world's lithium is used to make batteries for electric vehicles, according to Benchmark Mineral Intelligence estimates in 2025. Other major uses include industrial applications such as ceramics and glass manufacturing, and pharmaceutical mood stabilizers.

- Lithium in the lithium triangle is primarily extracted from brine, in which producers use water to wash lithium-heavy mineral deposits into basins, before allowing evaporation to slowly concentrate supplies over a year or longer. Mining companies also extract lithium from spodumene, a lithium aluminum inosilicate mineral; this process is more expensive but faster than brine extraction, with lower initial costs to begin operations. Spodumene lithium extraction is more common in Argentina than in Chile and Bolivia.

Chile has had the greatest success of the three countries in developing its lithium resources, consistently ranking among the top producers in recent decades, and has recently enacted reforms intended to further open its lithium resources to new investment. Chile, a historically free-market country, has a high level of state control over lithium development compared to other natural resources. The government has designated lithium as a non-concessionable mineral, requiring government involvement in its extraction. Despite this, lithium production in the country remains strong due to extensive government efforts to develop extraction infrastructure, well-funded programs and stable long-term contracts with the Chilean chemical company SQM and U.S. chemical company Albemarle, which extend to 2030 and 2043, respectively. Chile also benefits from well-developed infrastructure and extensive Pacific Ocean access, making it a particularly attractive supplier to China, which receives 70% of Chilean lithium carbonate exports. But in recent years, Chilean production has fallen behind Australia and China, which are now the world's first- and second-largest producers, respectively. This is partly due to the countries' use of hard-rock mining to extract lithium (a significantly faster process than brine extraction). It is also partially due to investment barriers in Chile, as while the Chilean government has tried to implement new developments in recent decades, there were no new government approvals of lithium projects for 30 years, from 1993 until the 2020s. In recent years, Chile's government has taken steps to make its lithium resources more investor-friendly, with former President Gabriel Boric adopting the country's National Lithium Strategy in April 2023, which is focused on sustainability and expanding the development of new areas through government-driven projects using private sector contractors. But major legislative changes have not occurred yet, and after far-right President Jose Antonio Kast took office in March 2026, Chilean lithium policy goals are set to change again. Kast has pursued explicitly pro-market economic policies and wants to accelerate project approvals and new exploration, as well as reduce state-majority ownership requirements.

- SQM has signed an agreement with the National Copper Corporation of Chile (Codelco) to extend the contract to 2060, with Codelco owning half of the shares plus one.

- Chile's gap in new lithium projects only ended with U.K.-linked CleanTech Lithium's proposal to develop the Laguna Verde brine deposit in Atacama, receiving government approval in March 2026. The deposit contains an estimated 1.9 million tons of lithium carbonate equivalent.

Argentina's production has not reached the same scale as Chile's, but the country has succeeded in developing extraction due to its attractive regulatory environment. In contrast to Chile, Argentina does not designate lithium as a strategic resource, and the state plays only a minor role in its extraction, with the country's constitution giving provincial governments the ability to grant concessions to companies. By law, provincial governments can charge a maximum of 3% royalties from companies (well below 7%-40% in Chile), further boosting investment attractiveness. These qualities have meant that Argentina has significantly more active lithium projects than regional neighbors, with 40 projects in exploration. Argentina has lagged behind Chile partially due to its later start, with production only ramping up in the 2000s, two decades after Chile. Additionally, Argentina's provincial government system creates a fragmented regulatory framework, and the country has faced greater economic instability than Chile, yet lithium investment still rose despite recent economic challenges. Since Argentine President Javier Milei took office in December 2023, his government has taken a libertarian approach to development, passing the Incentive Regime for Large Investments (RIGI) in July 2024, which, in addition to broadly making investment in Argentina more attractive via tax breaks, specifically focuses on accelerating approvals for new mining projects, including for lithium. In 2026, authorities passed reforms to the country's Glaciers Law to further shift environmental oversight to provinces, which, if adopted, would make it easier to access lithium deposits (as well as copper, gold and silver). However, the legal outlook for the reforms remains uncertain, as critics have argued they are unconstitutional and threaten communities and industries dependent on glacial water sources.

- Over the past few decades, Argentina has experienced an extended economic crisis. The country's annual inflation reached 219.9% in 2024, and its government debt-to-GDP ratio reached 154.6% in 2023, according to IMF data. Many sectors faced a drop in investment between 2021 and 2023, but lithium exploration saw investment increase 77.1% to $139.9 million, making the country the third largest recipient of lithium exploration expenditures globally during the period; this was likely due to a spike in demand in 2022, as well as the positive regulatory environment in the country.

- Argentina's lithium is generally lower quality than Chile's, with a higher magnesium-to-lithium ratio that requires more expensive processing, though it is still higher quality than that of much of the world's lithium supplies.

Of the three lithium triangle countries, Bolivia has struggled the most to develop its mining capabilities due to poor lithium quality, management issues and extended political instability. Bolivian authorities do not release official total production figures, but reported annual production estimates range from 1,500 to 3,500 tons, far below those of major global producers. This is partially a geographic reality: Bolivia, a landlocked country, is more expensive to launch operations in than Chile and Argentina. Furthermore, though Bolivia has significant identified resources, the lithium it possesses contains comparatively high levels of impurities including magnesium, potassium and boron, making it significantly more expensive to refine. But Bolivia's challenges are also due to political constraints. In 2008, then-President Evo Morales (2006-2019) of the left-wing Movement Toward Socialism (MAS) party launched a nationalization campaign for the country's lithium. Amid low funding, mismanagement, a lack of technical expertise, corruption and repeated political crises, development was slow, with state-owned lithium company Yacimientos de Litio Bolivianos (YLB) only recently opening its first plant in 2023. In an effort to accelerate development by gaining access to new extraction technologies, YLB signed contracts with Chinese consortium CBC and Russian company Uranium One Group in 2024. But the outlook for these contracts is uncertain following the election of right-wing President Rodrigo Paz Pereira in 2025, as he has brought them under review amid a broader push to pivot Bolivia's foreign policy away from Russia and China toward the United States.

- Starting in 2024, tensions between former President Luis Arce (2020-2025) and Morales, once allies, significantly escalated amid a dispute over who would represent MAS in the 2025 elections. This led to a split in the party, ushering in a period of legislative gridlock that prevented the Bolivian government from properly addressing dwindling foreign reserves and extreme shortages of basic necessities.

- Political instability and economic challenges have also driven mass, violent unrest in Bolivia in recent years. Groups across the political spectrum have participated in demonstrations that have blocked major highways for weeks or, in some cases, months to demand economic improvements. Protests have frequently turned deadly and lasted long enough to create localized shortages of food and other necessities, severely disrupting business operations.