Ukraine's intensifying drone campaign against Russia's energy infrastructure is unlikely to trigger a systemic crisis in the oil and gas sector or alter Moscow's calculus on the war, but it will act as a financial drain on Russian oil companies, even as global oil deficits buoy the Kremlin's revenues. On May 17, Ukrainian drones hit Gazprom Neft's 257,000 barrel per day Moscow Kapotnya oil refinery and Transneft's Solnechnogorsk oil pumping station, in what appears to be the largest drone attack on the Russian capital and the surrounding region since March 2025. This follows an almost daily Ukrainian drone campaign since the start of the war in Iran that has targeted some of Russia's most important energy infrastructure, including export hubs, pipelines, storage facilities and refineries. The attacks reportedly forced several facilities to halt or curtail operations and contributed to the loss of nearly 1 million barrels per day (bpd) of Russian crude refining capacity in March and over 1 million bpd in April, or roughly 16%. Russia's oil product exports fell 13.6% month on month to their lowest ever level of 2.2 million bpd, as refinery disruptions forced the government to impose a gasoline and kerosene export embargo on April 2 to protect domestic supply. With domestic storage filling and limited room to absorb surplus crude, Russian crude output fell by about 5% year on year in April to 8.8 million bpd. At the same time, the plunge in domestic refinery throughput freed up higher volumes of crude oil for export, which rose by 5.4% month on month from March to 4.9 million bpd.

- Gazprom Neft's Moscow Kapotnya refinery, which has reportedly halted processing following the May 17 drone strike, is among the top 10 largest in Russia and meets roughly 40% of Moscow and the wider region's fuel demand.

- Between January and May 2026, Ukrainian drones attacked at least 16 Russian refineries, some multiple times, including Surgutneftegaz's Kirishi refinery (with a 355,00 bpd refining capacity) and Rosneft's Ryazan oil refinery (340,000 bpd capacity), as well as the Lukoil refineries NORSI (320,000 bpd capacity), Yaroslavl (300,000 bpd capacity) and Perm (250,000 bpd capacity). The drone attacks also targeted Russian export hubs at Primorsk, Ust-Luga, Tuapse and Novorossiysk, along with major gas and condensate processing assets, including Gazprom's Astrakhan plant and Novatek's Ust-Luga complex, both of which suspended operations.

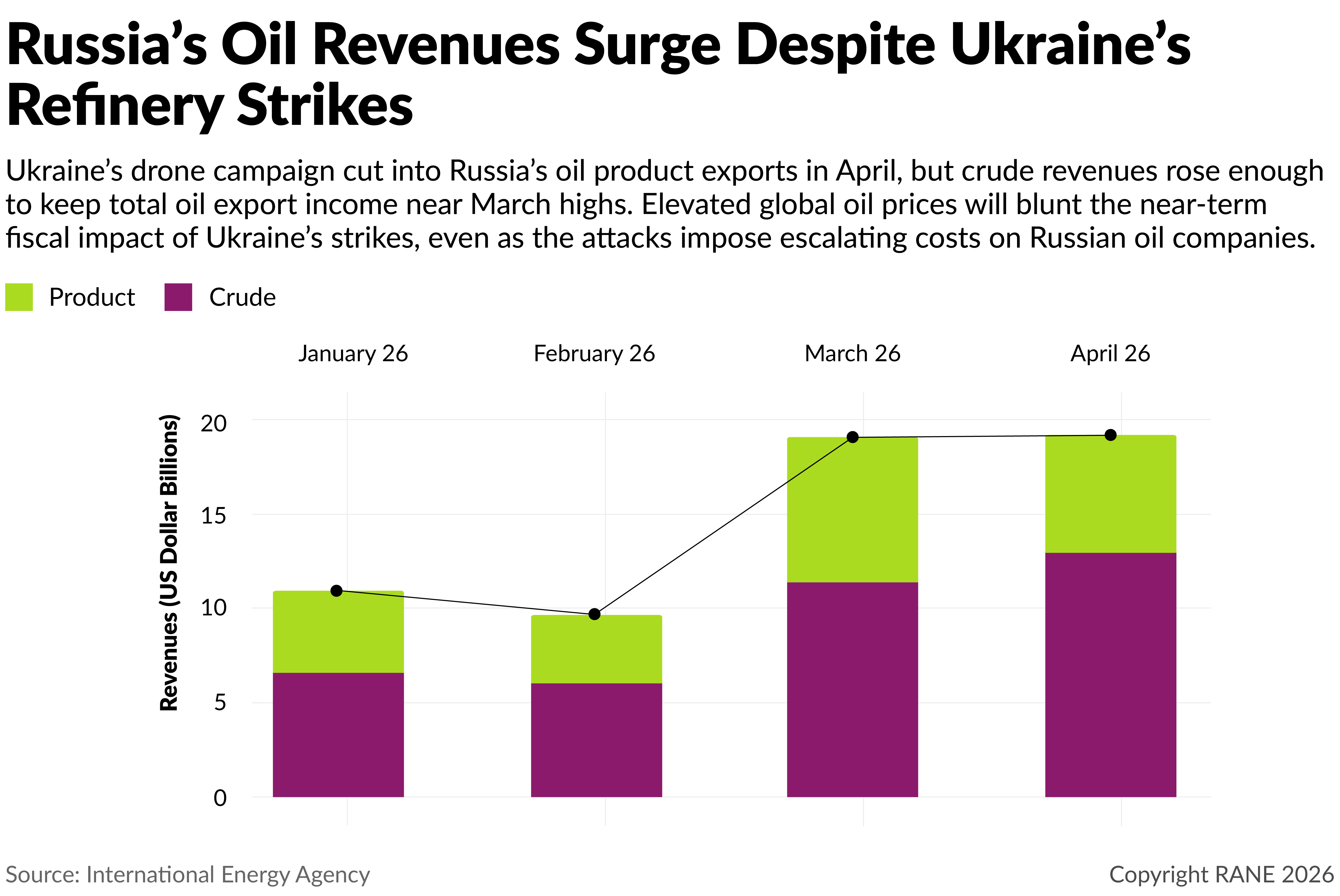

Global oil supply shocks caused by the Iran war have driven up crude prices, surging Moscow's export revenues, but Ukraine is leveraging its far-reaching drone program to hamper Russia's energy infrastructure. Iran's attacks on Gulf producers and ongoing shipping disruptions through the Strait of Hormuz have severely strained global oil supplies since the war began in late February. The supply crunch has lifted global crude and oil product prices, and, following temporary U.S. sanction waivers on Russian waterborne oil, has drawn new buyers to Russian Urals grade. As demand for Russian barrels increased, Urals prices have more than doubled, rising well above the $59 per barrel price Russia had assumed in its 2026 budget and narrowing the discount relative to international benchmarks. Meanwhile, Ukrainian attacks hobbled Russian refining operations or forced temporary halts, causing a drop in product exports. But despite this, Russia's gross export revenues still rose from $9.7 billion in February to $19.1 billion in March and $19.2 billion in April, according to the International Energy Agency (IEA). At the same time, the Ukrainian attacks appear to reflect a more refined prioritization of Russian energy targets, as well as improvements in the scale, range and operational sophistication of Kyiv's long-range drone program. The frequency, scale and geographic reach of recent strikes indicate that Ukraine can now generate larger strike packages, route drones around Russian air defenses, and repeat attacks against infrastructure where damage creates bottlenecks, forces shutdowns, raises repair costs and complicates export logistics.

- According to the IEA, Russia's total revenues from oil product exports fell from almost $7.7 billion in March to $6.2 in April, or by nearly 20% month on month. But this was offset by a surge in crude revenues from $11.4 billion in March to $12.9 billion in April, an increase of 13.2% month on month.

- According to Russia's finance ministry, Russian federal oil and gas revenues (primarily through the Mineral Extraction Tax and export duties) rose from 433 billion rubles ($5.9 billion) in February to 617 billion rubles ($8.4 billion) in March, up 43% month on month, and then to 855 billion rubles ($11.6 billion) in April, up 39% month on month — more than doubling since January. This massive influx of cash has offset the early 2026 revenue shortfalls, putting the Russian government back on track to balance the federal budget without a major deficit.

- OSINT data indicates that while earlier Ukrainian drone attacks often involved 1-2 drones reaching a refinery, recent strikes have reportedly involved 5-7 impacts, multiple attack waves over roughly a week, larger explosive payloads reaching facilities, and more hits on tank farms and storage areas, even as censored Russian state reporting makes damage assessment more difficult.

Russia's massive refining base and resilient export infrastructure will prevent a systemic oil sector crisis, but it will struggle to offset lower refinery runs, as Ukraine's repeated strikes will cause cascading disruptions, force upstream well shut-ins by exhausting storage buffers, and lead to a long-term degradation of energy infrastructure. Russian refinery throughput is likely to remain depressed in 2026, with crude runs averaging around 4.8 million bpd in the second quarter (down from 5.1 million bpd in March) and about 5 million bpd for the year, as repeated Ukrainian attacks will force more outages. Lower domestic processing capacity will push more Russian crude into export markets, but Russia will likely have limited room to keep increasing crude shipments, with Urals exports already near pre-2022 levels (about 1.9 million bpd in April) and close to loading capacity. This will leave Russia with less room to offset new capacity reductions through rerouting, higher crude exports or faster repairs, as further damage to ports, tank farms, pumping and loading stations and other petroleum product infrastructure increasingly affects both refined product exports and crude flows. The main threat will lie in a scenario in which choked product and crude export routes force Russia to fill up its storage networks, compelling costly shut-ins at the wellhead. Though Ukrainian strikes have already reportedly forced producers to shut in wells, Russia's geographically dispersed export network has so far absorbed the damage. Russia's broader oil sector resilience is also reinforced by its large refining base, low operating costs at mature fields and enough domestic or China-sourced equipment to keep most existing onshore oil production running. However, Russia's refineries and other energy infrastructure assets were built during the Cold War to withstand aerial bombardment, not sustained precision strikes against above-ground assets like tank farms or pumping stations. As Ukrainian drone salvos delivering multiple hits over several days continue, repeated fires and cooling cycles will cause thermal fatigue of metal, meaning the infrastructure will slowly degrade under stresses it was never designed to withstand. Ultimately, even limited damage short of destroying core processing units will continue to create cascading operational and logistical failures and drain Russian oil companies financially. However, to precipitate a systemic rupture rather than mere logistical friction, Ukraine would need to move beyond its precise but payload-light kamikaze drones, which lack the kinetic mass to obliterate hardened oil infrastructure, and instead start deploying heavy missiles. This would enable Ukraine to execute synchronized, high-density strikes that could paralyze multiple export nodes simultaneously and trigger systemic disruptions to Russia's oil sector, though Kyiv currently lacks an arsenal of such missiles.

- According to the IEA, Russia maintains over 30 major refinery complexes and over 250 mini-refineries, with a total primary refining capacity of approximately 7 million bpd. Less than 20% of Russia's major refining complexes are "new builds," with the remaining being legacy Soviet plants that have been kept running through decades of upgrades. Russia's sprawling export infrastructure also enables it to transport volumes via Baltic ports in Ust-Luga and Primorsk, the Black Sea port of Novorossiysk, the Kozmino port in the Far East, the East Siberia-Pacific Ocean pipeline and the Omsk-Pavlodar pipeline via Kazakhstan, as well as by rail.

- Ukraine's drone strikes on pumping stations in Transneft's network are beginning to affect upstream logistics by disrupting crude transport corridors from West Siberia and Yugra, where roughly 42% of Russian oil is produced. With storage filling and pipeline throughput constrained, at least one producer reportedly shut in 400 wells, according to leaks obtained by Ukrainian intelligence. Transneft, Russia's state-controlled oil pipeline monopoly, also stopped accepting Kazakh crude for transit through the northern Druzhba route on May 1, ostensibly because its pipeline system no longer had the technical capacity to accommodate additional transit volumes.

- Russian oil companies, not the state, will face massive permanent financial expenses amid Ukraine's ongoing airstrikes, including for insurance, physical protection and electronic countermeasures. Although public cost estimates are unavailable, future financial reports will likely reveal the impact through soaring operating and repair costs.

Ukraine's drone campaign is unlikely to disrupt Russian crude exports to the point that it alters Moscow's war calculus, but the attacks will impose mounting costs on Russia, especially in the case of a prolonged Strait of Hormuz closure, which would drive initial gains before demand destruction eventually caps them. If shipping through the Strait of Hormuz normalizes soon, Russia will likely retain a meaningful oil windfall. Although prices would likely fall from current levels, depleted inventories and the time needed to rebuild them, along with higher freight and insurance costs and the risk of another closure of the strait, would likely keep oil prices well above the Russian fiscal rule cut-off price. In this scenario, Moscow would receive several more months of elevated oil revenues, even as lower refinery runs, weaker oil product exports, domestic fuel subsidies, higher taxes, and the cost of repairing damaged facilities would consume part of the windfall. With the United States issuing a new May 18 waiver for Russian crude trade to avoid compounding Hormuz-related supply risks during the summer demand period, Moscow will be even better able to monetize elevated prices, further limiting the near-term fiscal impact of Ukrainian strikes. In a scenario where the Strait of Hormuz remains closed for longer, driving oil prices higher, Russia would initially earn more per barrel, but the gains would eventually become less linear and less stable. If prices remain near or above $150 per barrel for an extended period, they would weaken global demand, reduce refinery runs and increase the risk of recession-like demand destruction, which could then lower prices, capping Russian crude export gains. Against the backdrop of lower oil prices, Ukraine's intensifying drone campaign could become disruptive enough to trigger localized fuel shortages, especially during winter or peak-demand periods. Yet, as both historical precedents of aerial punishment campaigns and Russia's own winter bombardments of Ukrainian infrastructure demonstrate, while these localized disruptions may incinerate economic value and inflict domestic friction, such financial attrition alone would not be enough to shatter societal resolve or coerce the Kremlin into abandoning its overarching strategic objectives of the war in Ukraine.

- The higher oil price environment has raised the cost of Russia's domestic fuel price controls. In April, fuel damper payments — the government's financial mechanism for subsidizing oil refineries — reached about 207 billion rubles ($2.8 billion), more than half of Russia's total oil and gas revenues in January.

- In its May 2026 report, the IEA projects that under its base-case scenario, where the Iran war ends by early June, the global oil market will remain severely undersupplied through the late third quarter of 2026, accumulating a 900 million-barrel deficit by September. A more prolonged closure of the Strait of Hormuz could double that cumulative deficit by the end of 2026.