Editor's Note: In the coming year, RANE will analyze the implications of shifting demographic trends around the world. This series will be published periodically throughout the remainder of 2026; you can find all parts here.

Gulf governments' workforce localization efforts will help reduce budgetary burdens and support economic diversification, but they will also increase business costs and potentially reduce productivity due to skill mismatches. Over time, they will fuel regional competition and open the door to greater private sector unemployment in a future economic downturn. In April, several Gulf Cooperation Council (GCC) countries took additional steps to increase the number of local citizens, rather than foreigners, employed in the private sector, especially in high-skilled jobs. For example, on April 6, the United Arab Emirates' Vice President Sheikh Mansour bin Zayed Al Nahyan announced that the mandate of the Emirati Talent Competitiveness Council, or Nafis, whose goal is to increase Emirati participation in the private sector, would be extended from August 2026 to 2040. Then, on April 15, the Kuwaiti Ministry of Social Affairs announced that it had begun final interviews for the second phase of its "Kuwaitization" program to fill senior and supervisory roles in co-ops, public sector organizations that comprise the majority of retail trade, across the country, amid broader efforts to increase Kuwaiti participation in the private and public sectors. And on April 19, Saudi Arabia's target for 60% of private sector marketing and sales roles to be filled by Saudi citizens entered into effect after a grace period, marking one of Riyadh's latest "Saudization" efforts to boost local employment in the private sector.

- Gulf workforce localization requirements vary by country, sector and size of the company, but the sectors with the highest quotas align with each country's strategic and domestic priorities. For example, some of the highest quotas in Saudi Arabia are in the healthcare and dentistry sectors — exceeding 60% in some cases — in order to address Saudi Arabia's aging population. Oman, on the other hand, has higher quotas for logistics, financial services and administrative positions. The United Arab Emirates' highest quotas are in the financial, real estate and healthcare sectors, and Bahrain has prioritized banking, financial services and retail. Qatar has the highest quotas in energy, cybersecurity and information technology. And finally, Kuwait has high quotas in energy, banking and telecommunications.

- On April 5, Saudi Arabia's Ministry of Human Resources and Social Development provided an updated list of 69 professions, such as data entry and secretarial work, that require full Saudization, effective immediately, though with a six-month grace period for 50 of the professions.

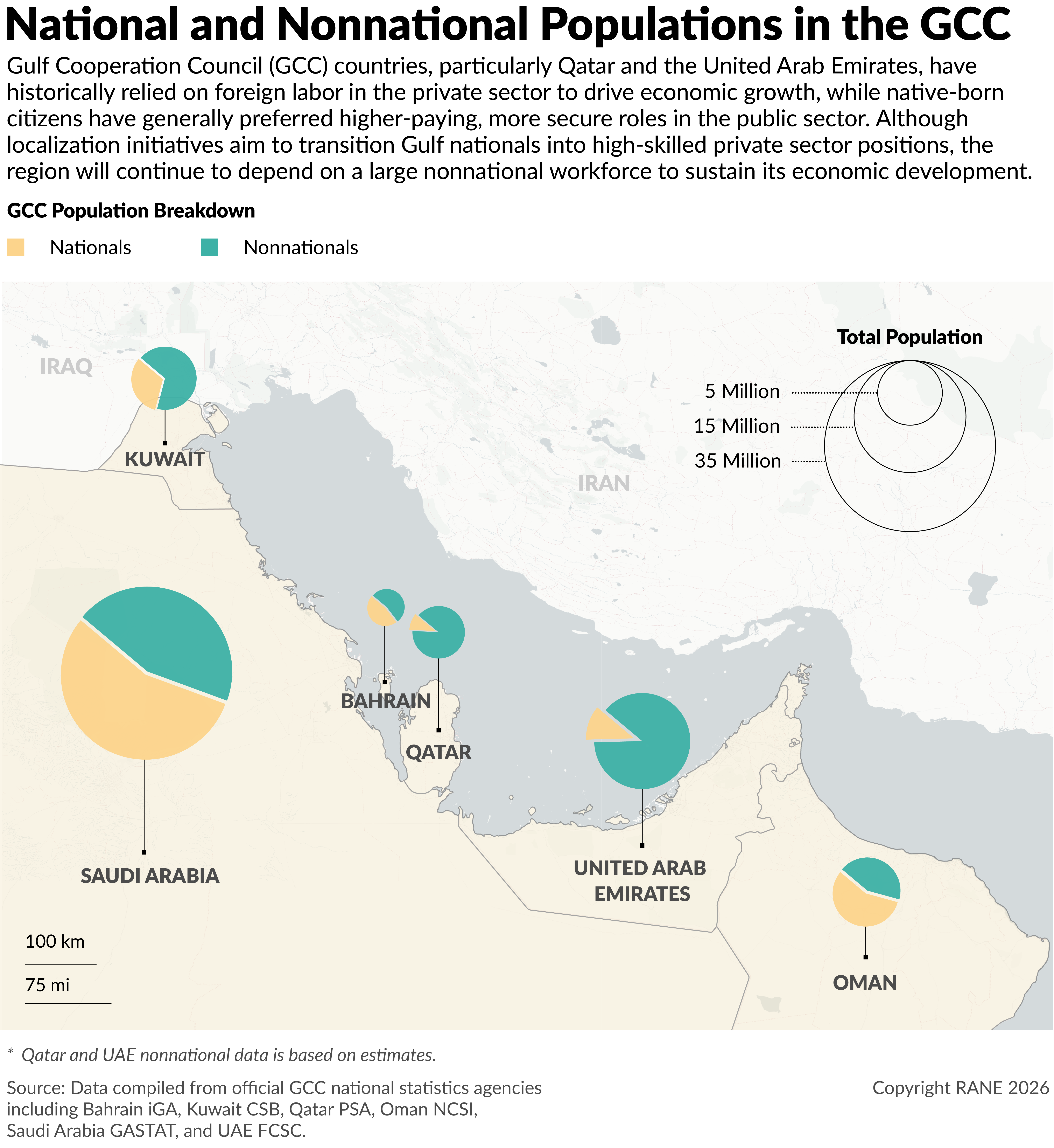

Gulf governments are implementing workforce localization initiatives as critical components of their economic modernization and diversification plans, driven primarily by the need to reduce reliance on foreign workers and mitigate the financial strain of high public wage bills. As part of GCC countries' economic modernization and diversification plans, governments have pursued localization initiatives to boost citizens' employment in the private sector, develop their domestic workforces' skills and reduce reliance on foreign workers. Indeed, according to the GCC's assistant secretary general for economic and development affairs, Khalid bin Ali Al Sunaidi, over 75% of the GCC's workforce in 2024 was comprised of foreign workers. In the United Arab Emirates and Qatar, the percentage was nearly 90%, making them the most reliant on foreign workers in the Gulf. The GCC's reliance on foreign workers has been fueled by relatively small populations of nationals and rapid economic development. Gulf citizens have tended to prefer working in the public sector due to higher salaries and greater job security compared with private sector equivalents, and because, until recently, the private sector in the GCC was relatively small. As such, foreign workers have filled labor gaps in both high- and low-skilled sectors, mainly in the expanding private sector. Across the GCC, however, nationals' heavy employment in public sector positions has resulted in high public wage bills, which comprise a sizable share of regional governments' annual budgets. High public wage bills, combined with low global oil prices over the past few years, have further incentivized governments to reduce the size of their public sectors and increase private sector employment of nationals. Most recently, decreased state revenue due to disruptions caused by the Iran war has further strained GCC countries' budgets, adding yet another reason to lower their public wage bills.

- More than 21 million of the 35 million foreign workers currently hosted in GCC countries are from South Asia, especially from India, Bangladesh and Pakistan. Other countries supplying significant numbers of foreign workers to GCC countries include Egypt, the Philippines, Yemen and Sudan.

- GCC restrictions on foreign workers' movement and job mobility have historically kept turnover relatively low, though recent labor reforms enacted in most GCC countries have made changing jobs easier for most foreign workers, especially in highly skilled positions. Some sectors, including hospitality and healthcare, have higher rates of foreign worker turnover, creating vulnerabilities in the labor supply.

- GCC countries have some of the highest public wage bills in the world. According to the World Bank, in 2022 (the last year of available data), the public sector wage bill as a percentage of total public expenditure was 26% for the United Arab Emirates, 26% for Oman, 31% for Bahrain, 32% for Qatar, 41% for Kuwait and 49% for Saudi Arabia. Workforce localization policies, hiring caps and efforts to avoid replacing retiring workers have helped some countries, such as Oman, reduce their public wage bill. However, others, such as Kuwait, have had less success in reducing their public wage bills, leading to budgetary cuts elsewhere.

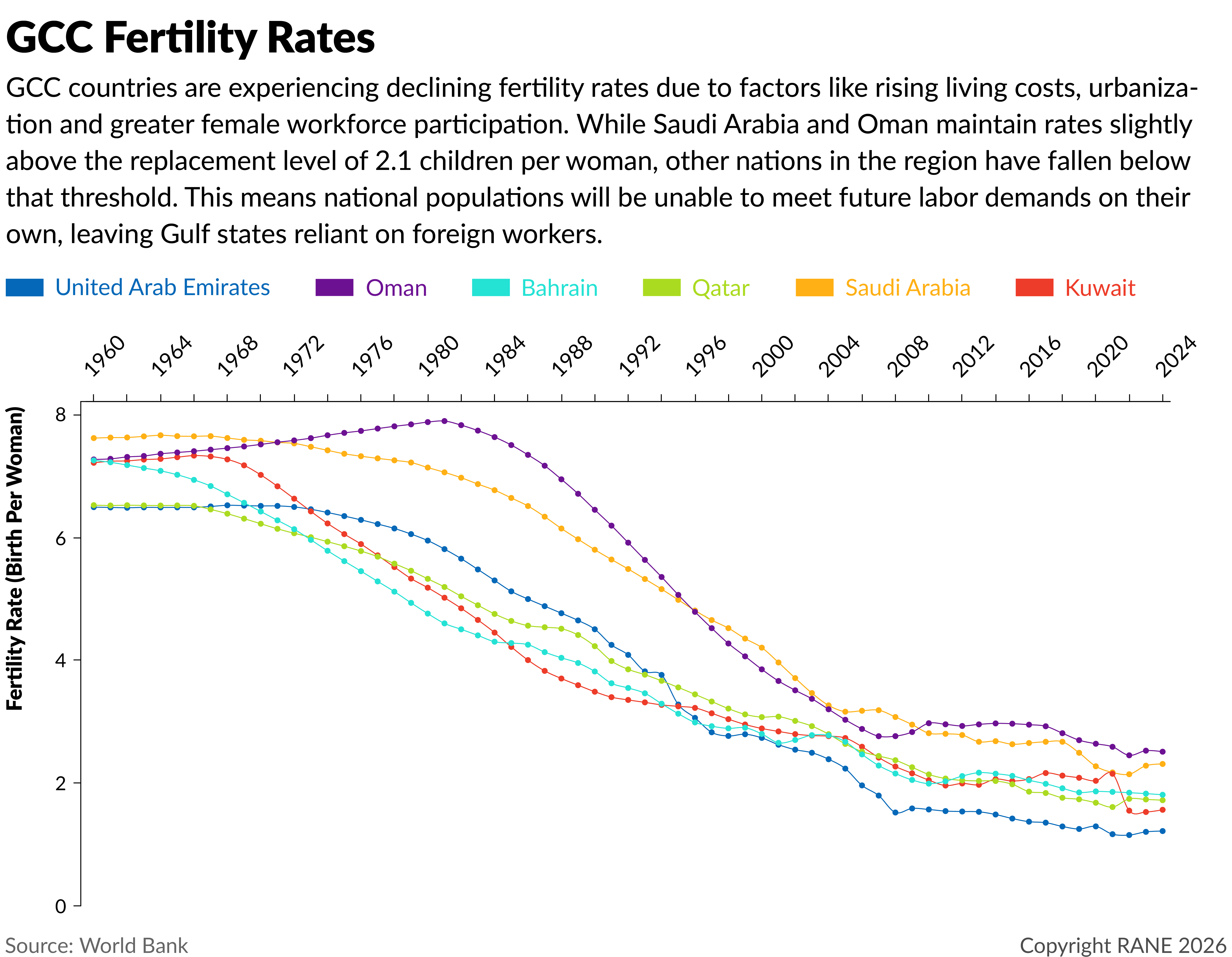

With projected population growth lower than the replacement rate in most regional states, the future labor market in GCC countries will continue to rely heavily on foreign workers, though a significant divide is expected to emerge, with nationals dominating high-skilled private-sector roles. Fertility rates have been declining in GCC countries and, in all but Saudi Arabia and Oman, have fallen below the natural replacement rate. This is driven in part by increased female participation in the workforce, delayed marriage, increasing costs of living and increased urbanization. As such, while the GCC population is forecast to increase over the next decade, this growth will largely be driven by migration rather than national population growth. Therefore, workforce localization efforts will not reduce the importance of foreign workers to GCC economies; rather, they will shift it. GCC countries are pursuing initiatives to increase their skilled labor forces, especially in the AI and tech sectors, with Abu Dhabi's One Million Prompters Program, for example, designed to increase Emirati advanced tech and AI skills. Through these initiatives, GCC nationals will likely increasingly displace foreign workers from high-skilled private sector jobs, especially those aligned with each GCC country's economic diversification strategy. However, foreign workers are highly likely to continue to hold the majority of low-skilled private sector jobs because of their lower pay, relative undesirability to GCC nationals and lower localization quotas. In countries with relatively small local populations and a high reliance on foreign workers, such as Qatar and the United Arab Emirates, workforce localization efforts will be insufficient to meet labor supply needs, at least for the foreseeable future, even in high-skilled sectors. As such, these governments in particular will likely take additional steps to reduce bureaucracy for foreign workers, thereby facilitating reliable foreign labor supplies for economic growth.

- According to a January 2026 GCC Statistical Center report, the total population of GCC countries (national and foreign) is expected to reach 83.6 million by 2050, up from 61.2 million at the beginning of 2025.

- Even though Saudi Arabia and Oman have fertility rates higher than the rate of replacement, around 2.1, they are only slightly above at 2.3 and 2.5 children per woman, respectively. To increase fertility rates, as well as boost female employment, many GCC countries' economic diversification and modernization plans include steps to support working mothers, such as initiatives for subsidized childcare, flexible working environments and extended maternity leave. However, these efforts have not yet yielded any significant increases.

- Iranian attacks against Gulf countries have resulted in the deaths of some foreign workers, including workers from South Asia. Even so, foreign workers — especially low-skilled workers — will likely continue to take positions in Gulf countries in pursuit of economic opportunities.

- In the wake of the Middle East crisis, some companies operating in Gulf countries may reconsider investments, not only due to safety risks but also GCC workforce localization requirements. As a result, some regional governments may slow-walk additional localization quotas, relax enforcement and/or extend grace periods to ensure foreign investment flows. However, they are unlikely to meaningfully reverse the trajectory of their workforce localization strategies, which they see as crucial to their economic development goals.

For businesses in the region, government regulations intended to incentivize national employment present rising operational challenges, including increased labor costs, potential productivity losses from skill mismatches and the risk of noncompliance penalties. Government regulations to incentivize GCC nationals to take private sector positions, such as establishing minimum wages for the roles, will increase business costs for companies. Furthermore, if companies do not meet the quotas for national hires, governments will likely increasingly impose penalties and seek to close loopholes in the future. Further complicating this is a mismatch between the skills required for the job and the skills of locals. Though government-provided educational and training opportunities will likely close some of these skill-related gaps over time, companies operating in the Gulf may have to expend some of their own resources to support additional training to upskill local employees over the next several years. Additionally, with some countries like Saudi Arabia implementing percentage-based quotas on foreign workers, companies may be forced to hire less-qualified local workers to comply with government regulations, incurring productivity losses. Alternatively, some companies may prioritize productivity and efficiency and hire qualified foreign workers to fill positions, accepting the penalties for noncompliance with localization standards. Businesses generally will be more likely to comply in countries with penalties that threaten to infringe on broader operations, such as hiring restrictions and suspension of commercial registration, rather than merely imposing fines.

- In the United Arab Emirates, companies with 50 or more skilled workers — defined by educational background and minimum salaries — face monthly penalties of roughly $2,722 for each Emirati position that remains unfilled in accordance with the workforce localization standards. In Saudi Arabia, companies that do not comply with localization standards could face fines ranging from $800 to $2,666 per violation, as well as restrictions on hiring foreign workers or even the suspension of commercial registrations, which would essentially halt their business operations in the kingdom.

Workforce localization efforts, while intended to improve fiscal health, will ultimately intensify intra-GCC competition in strategic sectors and introduce vulnerabilities if a future economic downturn raises private sector unemployment and forces government support. Over time, workforce localization efforts will likely fuel intra-GCC economic competition as Gulf nations strive to attract investment in key sectors. While tech and AI development are core to the United Arab Emirates and Saudi Arabia's economic diversification plans, the race for dominance will also extend to other areas where the two countries have overlapping priorities, such as tourism and financial services. Saudi Arabia will likely maintain an edge due to the large size of its native-born population and the country's relative safety compared with the United Arab Emirates, which has suffered far more Iranian attacks on major urban areas; this perception of safety will further deepen if Saudi Arabia's reported understanding with Iran to de-escalate tensions remains intact. Workforce localization policies will likely eventually improve fiscal consolidation and reduce bloated public wage bills, giving GCC governments greater fiscal flexibility. Still, the expansion of the private sector will introduce new risks. While the public sector has traditionally offered GCC citizens exceptional job security, the shift toward private employment will increase the risk of layoffs during economic downturns. In such a scenario, GCC governments would likely be pressured to intervene and provide support to the private sector to avoid public backlash. For some countries with robust financial resources and relatively small national populations (namely, Qatar and the United Arab Emirates), providing such financial support would be feasible. Saudi Arabia's Public Investment Fund also provides a financial backstop, though its sizable workforce may necessitate more targeted support. Conversely, countries with smaller investment funds — such as Kuwait, Oman and Bahrain — face a higher risk of domestic unrest if private sector unemployment rises, but also are less able to provide the economic support needed to reduce destabilizing layoffs. In Bahrain, this risk is compounded by sectarian divides, stemming from a Sunni ruling family governing a Shiite majority. These states may, in turn, increasingly look to their wealthier neighbors for financial support to avoid domestic unrest. While Qatar, the United Arab Emirates and Saudi Arabia would likely provide such aid to maintain regional stability, doing so would expand their influence over other Gulf countries and further sharpen the competition for regional dominance, particularly between the United Arab Emirates and Saudi Arabia.

- On April 9, the United Arab Emirates and Bahrain signed a five-year, $5.4 billion currency swap agreement to improve liquidity amid Bahrain's ongoing economic struggles stemming from the Iran war.

- Overall, GCC countries have very low official unemployment rates. In the fourth quarter of 2025, Saudi Arabia's overall unemployment rate was 3.5%, though it was 7.2% for Saudi nationals. Bahrain's unemployment rate was among the highest in the GCC at around 6.1%. By contrast, Qatar had one of the lowest rates in the world at 0.1% due to high workforce participation and its reliance on foreign labor.

- The United Arab Emirates and Saudi Arabia have preexisting tensions fueled by economic competition, foreign policy divergences and competing influence in the region. The United Arab Emirates' decision to exit OPEC on May 1 further underscores its policy independence and will fuel tensions with Saudi Arabia, despite some temporary easing during the Iran conflict.