Kazakhstan's agreement with Russia for the construction of its first nuclear power plant will help solidify Moscow's long-term geopolitical foothold in the country, but Astana will seek to hedge this dependency by engaging China on future projects and leveraging new mining regulations to extract downstream nuclear technology from foreign partners. On April 21, Kazakhstan's Atomic Energy Agency chairman Almasadam Satkaliyev said the agency was working on a deal in which Russia would provide an interstate loan covering 85% of the roughly $15 billion cost of Kazakhstan's first nuclear power plant, with Kazakhstan covering the remaining 15%. Rosatom, Russia's state-owned nuclear corporation, will build the plant near Ulken on Lake Balkhash in southeastern Kazakhstan. The project envisions a two-reactor facility with a total capacity of 2.4 gigawatts, with commissioning targeted for 2035-36. Once signed, the financing and construction agreements will build on Rosatom's existing mining presence in Kazakhstan's uranium sector through joint ventures with Kazatomprom, the country's state-owned atomic company. They will extend Russian involvement from upstream resource extraction into reactor construction, financing and lifecycle services. At the same time, Kazakhstan also announced in July 2025 that China National Nuclear Corporation (CNNC) would lead construction of its second and third nuclear plants, with the second tentatively planned at Moinkum, also near Lake Balkhash. Separately, the government is exploring the potential deployment of small modular reactors (SMR). On April 15, Kazakhstan released its Nuclear Development Strategy to 2050, calling for the construction of at least three nuclear plants and potentially a fourth. The plan reflects Astana's effort to leverage its position as the world's largest uranium producer to develop domestic nuclear generation capacity.

- Kazakhstan is the world's largest uranium producer, accounting for over 40% of global output, with production reaching about 25,800 tonnes in 2025. It also holds the world's second-largest proven uranium reserves, after Australia, estimated at roughly 14% of global resources.

- In 2024, Kazakhstan held a controversial referendum to greenlight the construction of a nuclear power plant, a politically sensitive issue for the public given the enduring Soviet-era nuclear weapons testing legacy, with a majority reportedly voting in favor of allowing the construction of nuclear power plants.

- Kazakhstan's Nuclear Development Strategy to 2050 outlines plans to develop a full nuclear industrial cluster, including fuel-cycle capabilities, localized manufacturing, workforce development and supporting infrastructure, such as transmission and grid integration. It also emphasizes energy security, decarbonization targets and long-term demand growth tied to industrial expansion and electrification.

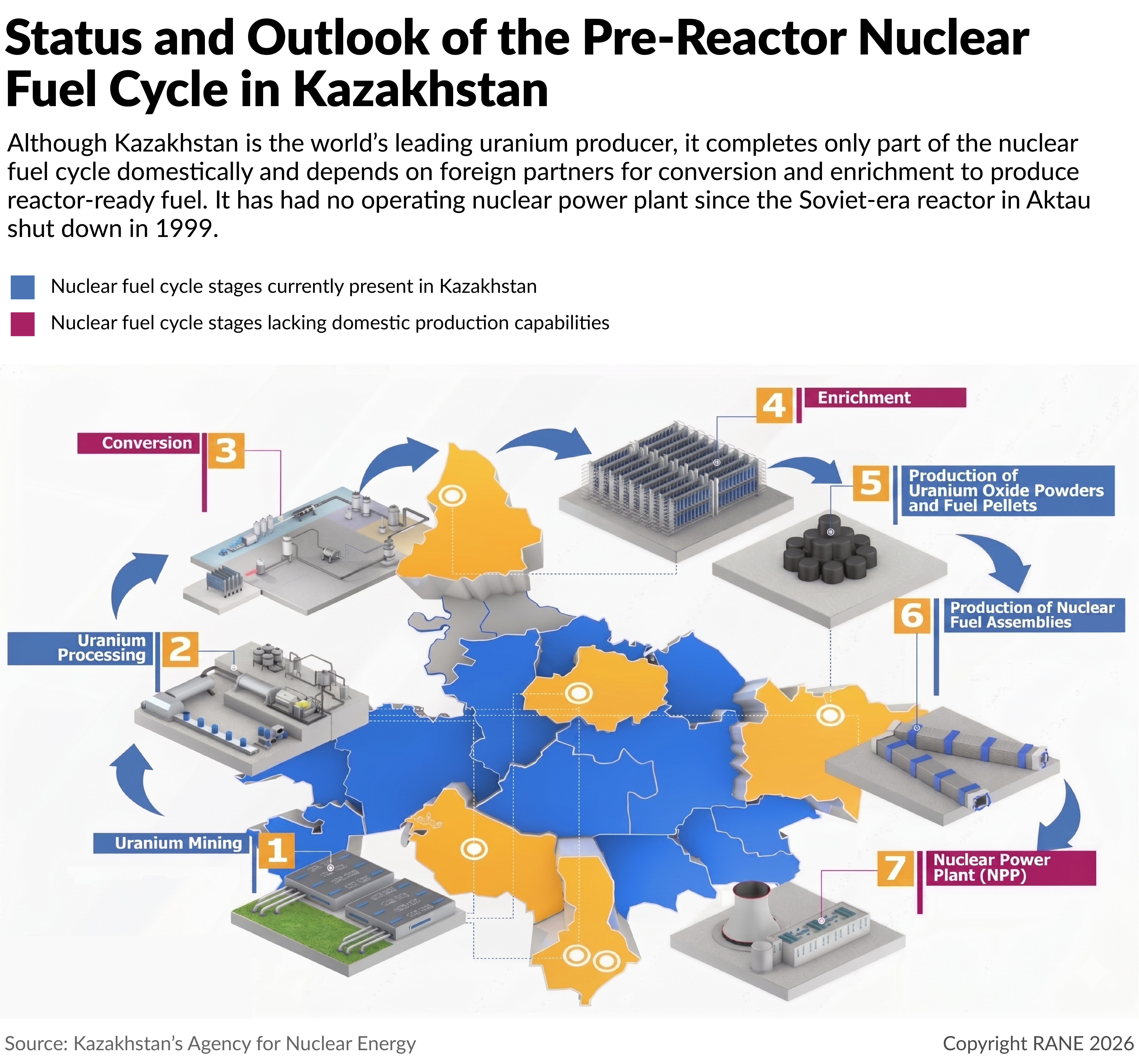

- Kazatomprom controls all domestic uranium production and operates through an internationalized structure integrated into global nuclear supply chains, with 12 of its 14 uranium enterprises being joint ventures, involving partners from Russia, China, France, Canada and Japan. Its largest export markets include China, Russia (mainly for conversion and enrichment), the United States and France.

Kazakhstan is determined to deploy nuclear power to address regional electricity shortages, yet selecting Rosatom and its state-backed financing underscores Astana's strategic necessity to accommodate Moscow's strategic interests. Kazakhstan's power system remains structurally imbalanced, with most generation concentrated in the coal-heavy north while demand growth is strongest in the south. To cover deficits, the country relies on Russian imports or internal transfers. But these remain vulnerable due to aging infrastructure, underinvestment and fragmented grid development, leaving the country exposed to supply shortfalls during peak periods. In this context, nuclear energy offers a predictable, baseload long-term solution that aligns with Kazakhstan's resource base. As the world's largest uranium producer, Kazakhstan has a clear comparative advantage in the upstream segment of the nuclear fuel cycle, making the political case for domestic nuclear generation relatively straightforward. However, the choice of Rosatom as the vendor and the state-to-state financing model reflect a geopolitical accommodation as much as technological and economic considerations. Despite Western restrictions, Rosatom remains the dominant global exporter of nuclear power plants, controlling roughly 70% of the reactor export market, and offers an integrated package that includes reactor construction, fuel supply, long-term servicing, spent fuel processing and state-backed financing. This model, however, also serves a geopolitical function for Moscow as it binds recipient countries into decades-long dependencies through fuel, maintenance and financing arrangements that extend across the plant's operating life. The Kremlin has leveraged Rosatom's existing footprint in Kazakhstan's uranium sector to secure downstream expansion into reactor construction and financing. For Astana, rejecting such a package in favor of a non-Russian vendor would have carried political risk, as Moscow views Kazakhstan's alignment, including on nuclear cooperation, as a core strategic interest. But Astana is also mitigating this exposure by engaging China, which likely reflects uncertainty over Russia's ability to execute new projects under Western sanctions, concerns about Rosatom's financial position and a broader reluctance to deepen dependence on Russia.

- Kazakhstan faces severe electricity deficits, driven by aging infrastructure, with 66% of its power grid worn out and more than half of its thermal power plant equipment over 30 years old. The government's 2023 Concept for the Development of the Electric Power Industry through 2029 projects deficits of 5.5 billion kilowatt-hours in total generation and 3,076 megawatts in capacity by 2029. To address these shortfalls, Astana plans to add 11.7 gigawatts of new capacity by modernizing gas-fired plants, rapidly expanding renewables and deploying nuclear energy. Nuclear energy is particularly well-suited, as it delivers reliable, large-scale baseload power to meet growing southern demand.

- Rosatom currently has around 20 reactor units under construction across at least seven countries, including major projects in Turkey, Egypt, Bangladesh, India and China. It typically pairs these projects with state-backed financing or preferential credit arrangements.

- Rosatom historically held a nuclear monopoly across Eastern Europe by supplying proprietary reactor fuel. Following Russia's full-scale invasion of Ukraine, some of the region's more reliant countries executed complex decoupling strategies, facing rigorous licensing hurdles and higher Western fuel costs. The Czech Republic (six reactors), Slovakia (five reactors) and Bulgaria (two reactors) have so far transitioned successfully. Even Hungary (four reactors) signed alternative contracts with the United States and other European suppliers, effectively breaking Russia's regional grip.

Geographic proximity and strong financial interdependence may ease logistics and payment hurdles at Ulken, but opaque terms, corruption and sanctions on Rosatom portend delays and financial instability. Nuclear power plant construction is inherently complex, capital-intensive, and highly sensitive to site-specific and regulatory challenges, often resulting in schedule delays and cost overruns across the industry. In Rosatom's case, many project setbacks have stemmed from technical and management shortcomings, including engineering challenges and site-related complications, such as incomplete surveys or insufficient assessment of geological or topographical conditions. Since 2022, these baseline risks have intensified as sanctions have disrupted financing, supply chains and equipment deliveries for Rosatom's overseas projects, introducing additional delays. The Ulken project in Kazakhstan is unlikely to face the same degree of logistical or payment disruption, given its geographic proximity to Russia and established financial channels. However, project execution will still depend on the final terms and reliability of intergovernmental financing and construction agreements. Earlier problems with Russian-backed coal power projects in Kazakhstan, where sanctions contributed to financing delays, underscore the risk that funding arrangements may not materialize as planned. Beyond financing risks, structural challenges will persist as opaque project terms, cost inflation and entrenched corruption within Russia's and Kazakhstan's state-linked nuclear sectors raise concerns about execution quality, financial transparency and long-term operational safety.

- Since 2022, Rosatom's overseas projects have faced mounting delays and financing strain. At Turkey's Akkuyu plant, commissioning of the first reactor has slipped to 2026 amid funding disruptions and equipment delivery issues. Hungary's Paks II remains more than a decade behind schedule due to contract revisions and procurement delays, while in Bangladesh and Egypt, projects at Rooppur and El-Dabaa have required adjustments to financing terms, payment mechanisms and supply chains.

- In 2024, Kazakhstan and Russia agreed to build three coal-fired combined heat and power plants with Russian state-backed financing. By mid-2025, Astana indicated that concessional funding had not been confirmed and began construction of one project independently. In early 2026, the remaining plants were reassigned to a Kazakh-Singaporean consortium after Russia failed to secure the required export credit guarantees.

The war in Ukraine will intensify Russia's economic constraints, hindering Moscow's ability to provide the comprehensive financing and construction packages that underpin Rosatom's competitiveness, forcing it either to collaborate with or compete against Chinese companies. As Rosatom's access to developed markets narrows, Moscow is likely to treat Kazakhstan and other strategically important Eurasian markets as critical to preserving both its reactor export portfolio and the political influence that accompanies long-term nuclear dependence. Given deep bilateral ties and Russia's entrenched position in Kazakhstan's uranium sector through Rosatom's Uranium One subsidiary's mining interests and its lead role in the Ulken project, the Kremlin will likely commit political capital and state-backed financing to prevent any meaningful erosion of its nuclear foothold. But the longer the war in Ukraine continues and the more Russia's economic constraints deepen, the harder it will be for Moscow to sustain the full package of sovereign credit, technology access and turnkey delivery that has historically made Rosatom competitive. Even if hostilities subside, sanctions and export control regimes would likely remain in place for some time — and with them, impediments to Russian procurements of dual-use components. Such strain would likely increase Russia's reliance on Chinese industrial input and supply chains in some segments as a tactic to preserve its own role. However, integrating Chinese supply chains into Russian exports would risk eroding Rosatom's value proposition over time, making it harder for the company to compete directly against China's own state-backed nuclear companies in key markets, including Kazakhstan, Uzbekistan and Turkey, where governments are diversifying partners for nuclear buildout. Competition would likely be most pronounced in small modular reactors and in financing and equipment supply, where Russia may struggle to match China's manufacturing scale, delivery timelines and capital support.

- Russia holds major stakes in Kazakhstan's uranium sector through Uranium One, including 49% of the joint venture Budenovskoye (which operates a massive, newly developed mega-deposit), 50% of Karatau and Akbastau, and 70% of South Inkai Southern Mining and Chemical Company.

- In December 2025, Turkey secured an additional $9 billion in Russian financing to complete all four Akkuyu units, even as China has indirectly entered the project by replacing blocked Siemens components. Turkey is also reportedly considering alternative partners for future projects, including a potential U.S.-South Korea consortium for the Sinop plant and Chinese involvement at a third site in Thrace.

Meanwhile, in the upstream segment, Astana will leverage new subsoil regulations to pressure foreign partners to secure downstream technology transfers and achieve fuel-cycle sovereignty, though Russia will resist concessions that jeopardize its geopolitical leverage over Kazakhstan. Although Kazakhstan is the world's leading uranium producer, it still lacks domestic conversion and enrichment capacity. This means Astana cannot convert upstream dominance into a sovereign fuel cycle without foreign technology, capital and a permissive geopolitical environment, at a time when Moscow would have a clear incentive to resist any effort that would reduce Kazakhstan's dependence on Russian downstream services. The December 2025 amendments to the Subsoil Use Code will give Astana more leverage as mining contracts expire. Kazakhstan will likely use these rules to press foreign partners for downstream concessions, initially focusing on conversion and, eventually, enrichment. Precedent at the Inkai mine, where in 2016 Kazakhstan tied long-term upstream access to downstream cooperation from a Western major, suggests this tactic is not new. The upcoming uranium production contract renewals will trigger tough negotiations with Russia, while also opening a narrow window for Western participation in Kazakhstan's downstream sector. Russia, however, is unlikely to concede genuine autonomy. As Uranium One's subsoil use agreements approach renewal, Moscow will likely attempt to steer Astana toward a selective accommodation, offering limited localization while withholding sensitive technology to maintain operational control over key downstream segments. If this approach fails, or if Chinese, South Korean or Western companies offer Astana more attractive terms, Moscow could leverage its stranglehold over Kazakh export routes and the planned Ulken nuclear power plant to stymie Astana's diversification efforts. Several key indicators will signal the trajectory of this competition, starting with the renewal talks for the South Inkai deposit, which is currently set to expire in 2029. These negotiations will reveal whether Russia intends to accommodate Kazakhstan's new localization rules to preserve its position, or if it begins treating the asset as expendable. If Moscow resists concessions or threatens to walk away, a secondary indicator will be whether Astana invites non-Russian partners to build domestic conversion capacity, likely in exchange for minority stakes, or if it pivots to China as a fallback. In the medium term, a breakthrough in conversion capacity would signal that Kazakhstan is using the new Subsoil Use amendments not only to renegotiate terms with Moscow but to bring non-Russian partners into the downstream nuclear chain and thereby build a more competitive and diversified downstream structure. Progress on enrichment, however, will remain a longer-term and much more geopolitically fraught objective. The most likely outcome will not be full Kazakh fuel cycle sovereignty, but a renegotiated dependency in which Astana gains more formal control over its uranium assets and expands conversion capacity without fully escaping Russian leverage.

- In December 2025, Kazakhstan amended the Subsoil Use Code to make the extension of uranium production periods for foreign partners in joint ventures conditional on either handing over at least a 90% stake to Kazatomprom or transferring and localizing the conversion and enrichment of uranium (up to 5% enriched uranium hexafluoride).

- In March 2026, upon expiration of the Akdala subsoil use agreement, Uranium One effectively lost its 70% stake in the Akdala mine as the deposit was transferred into Kazatomprom's trust management under the new Subsoil Code provisions. The next production contract due for renewal is South Inkai in 2029, while other Uranium One-owned uranium assets are not expected to come up for renewal until the late 2030s.

- In 2016, Canada's Cameco agreed to provide Kazatomprom royalty-free access to its uranium refining technology and a five-year option to license its conversion technology as part of the restructuring of the Inkai joint venture, in exchange for extending production rights through 2045 while reducing Cameco's stake to 40% from 60%.