The Iran conflict is increasing global economic uncertainty and financial market volatility, most acutely harming financially weak, net energy-importing economies with low per capita incomes whose governments will face painful financial trade-offs, higher import and financing costs, and heightened unrest risks. On April 14, the International Monetary Fund (IMF) released an update to its biannual World Economic Outlook. Against the backdrop of the Iran war, the fund modestly downgraded its global growth forecast but also highlighted the risk of a global recession in the case of a prolonged conflict and long-lasting higher oil prices. The IMF's warning was the latest in a series of similar downgrades from multinational financial institutions, global banks and national authorities. The war has substantially increased global energy and fertilizer prices amid Iran's attacks on Gulf energy infrastructure and the effective closure of the Strait of Hormuz, which previously handled 20-25% of global oil exports, 20% of global liquefied natural gas (LNG) exports and 20-30% of global fertilizer exports.

- On April 14, the IMF downgraded global real GDP growth for 2026 from 3.3% in January to 3.1% due to the negative impact of higher energy prices. Real GDP growth in emerging and developing economies is forecast at 3.9%, down from 4.2% in January.

- From a pre-war level of $70 per barrel, Brent crude reached $110 per barrel in early April. Following the announcement of the U.S.-Iran ceasefire on April 7, prices fell to the mid-nineties before increasing again above $100 following the announcement of the U.S. blockade of the Strait of Hormuz on April 12. Even at their early April peak, oil prices remained well below the $147 levels seen in 2008, and even more so in real terms. While energy prices have risen significantly, nominal oil prices remain below the levels reached in 2010-11 and 2022.

- An Iranian strike on Qatar's Ras Laffan complex in mid-March knocked out 17% of the country's LNG export capacity. This caused Asian LNG spot prices to increase by more than 100%. Initial estimates suggest that repairing the facility could take three-to-five years.

- OPEC oil production declined more than 25% in volume terms during March compared to the previous month. This constituted the largest monthly drop in OPEC history. The fall in production was largely due to many Gulf OPEC members being unable to ship oil, which filled their storage and forced them to reduce output.

Global financial markets sold off following the onset of the conflict, but the selloff has not been extreme by historical standards, and prices have largely recovered following the ceasefire announcement. In March, investors curtailed their exposure to risk assets, notably equities and junk bonds, as well as the currencies of net energy importers, such as Japan, Korea and India. While financial market volatility increased, it remained well below the levels observed in April 2025 when the administration of U.S. President Donald Trump announced sweeping reciprocal tariffs. The U.S. dollar experienced a modest rally amid heightened geopolitical-driven risk aversion, and U.S. long-term interest rates rose amid higher energy-price-related inflation expectations. Long-term interest rates also moved higher in Germany, the United Kingdom and Japan, but not dramatically so. Since the ceasefire announcement on April 7, many asset prices have recovered a significant share of their initial losses, but they remain below pre-conflict levels.

- By late March, global financial markets reached their lowest levels, with U.S. and European equity markets down 4-5%. At their peak on March 27, ten-year government bond yields were up 40 basis points in the United States, Japan and Germany. The dollar was up less than 2% in trade-weighted terms. The VIX index, a measure of investor uncertainty, peaked at just above 30 on March 27, which was far below the above-50 levels seen in April 2025 when the Trump administration announced its global tariffs. Emerging economies reliant on energy imports have seen the largest equity market declines, with India's Sensex dropping by more than 7% at one point. On the other hand, some net oil exporters, such as Brazil, have seen their stock indices make gains.

- Since the ceasefire announcement, financial markets have recovered significantly. As of April 13, the S&P 500 is slightly above the levels seen on Feb. 27 (the day before the outbreak of the conflict). U.S., German and Japanese ten-year government bond yields have narrowed somewhat, but as of April 14, they remain around 30 basis points above pre-war levels.

The longer energy prices remain elevated, the more severe and longer-lasting the financial market impact will be due to higher inflation, higher interest rates and lower economic growth. If the Iran war turns into a low-intensity conflict characterized by repeated interruptions of oil and gas shipments through the Strait of Hormuz, elevated oil prices will increase inflation and slow economic growth, particularly if oil prices remain around $100 per barrel. Even in a more optimistic scenario in which the recently announced ceasefire leads to the rapid opening of Gulf energy exports through the Strait, oil prices will fall, but only gradually, and are likely to remain above pre-conflict levels of $60-70 per barrel until the end of the year. In the first case, the potential for stagflation reminiscent of the 1970s, characterized by a confluence of stagnant economic growth and elevated inflation, will become more likely. Higher inflation, set against an uncertain trajectory for energy prices, has already prompted markets to recalibrate monetary policy expectations, specifically by reducing anticipated interest rate cuts in the United States and increasing expected rate hikes in the European Union and the United Kingdom. The policy response of central banks will depend heavily on how long energy prices remain elevated and the extent to which those prices affect long-term inflation expectations, thereby translating into higher goods and services inflation. Even in a more optimistic scenario, where the Strait of Hormuz largely opens and remains open, central banks will likely still remain in a wait-and-see mode, and the U.S. Federal Reserve and the European Central Bank may end up keeping their policy rates unchanged in 2026. While financial asset prices would continue to recover, they would receive no support from significantly easier monetary conditions.

- In its most recent Economic Outlook update, published on March 17, the OECD forecast U.S. inflation to reach 4.2% in 2026, compared to 2.9% in Germany, 2.4% in Italy and 1.8% in France.

- Inflation in the United States continues to run above the Fed's 2% target. In February, U.S. consumer price inflation reached 2.4%, while core inflation stood at 2.5%. U.S. headline inflation jumped to 3.3% in March, compared to 2.4% in February on higher oil prices. Core inflation reached 2.6% in March, compared to 2.5% in February. In its Summary of Economic Projections, released on March 18, the Fed forecast one 25-basis-point interest rate cut.

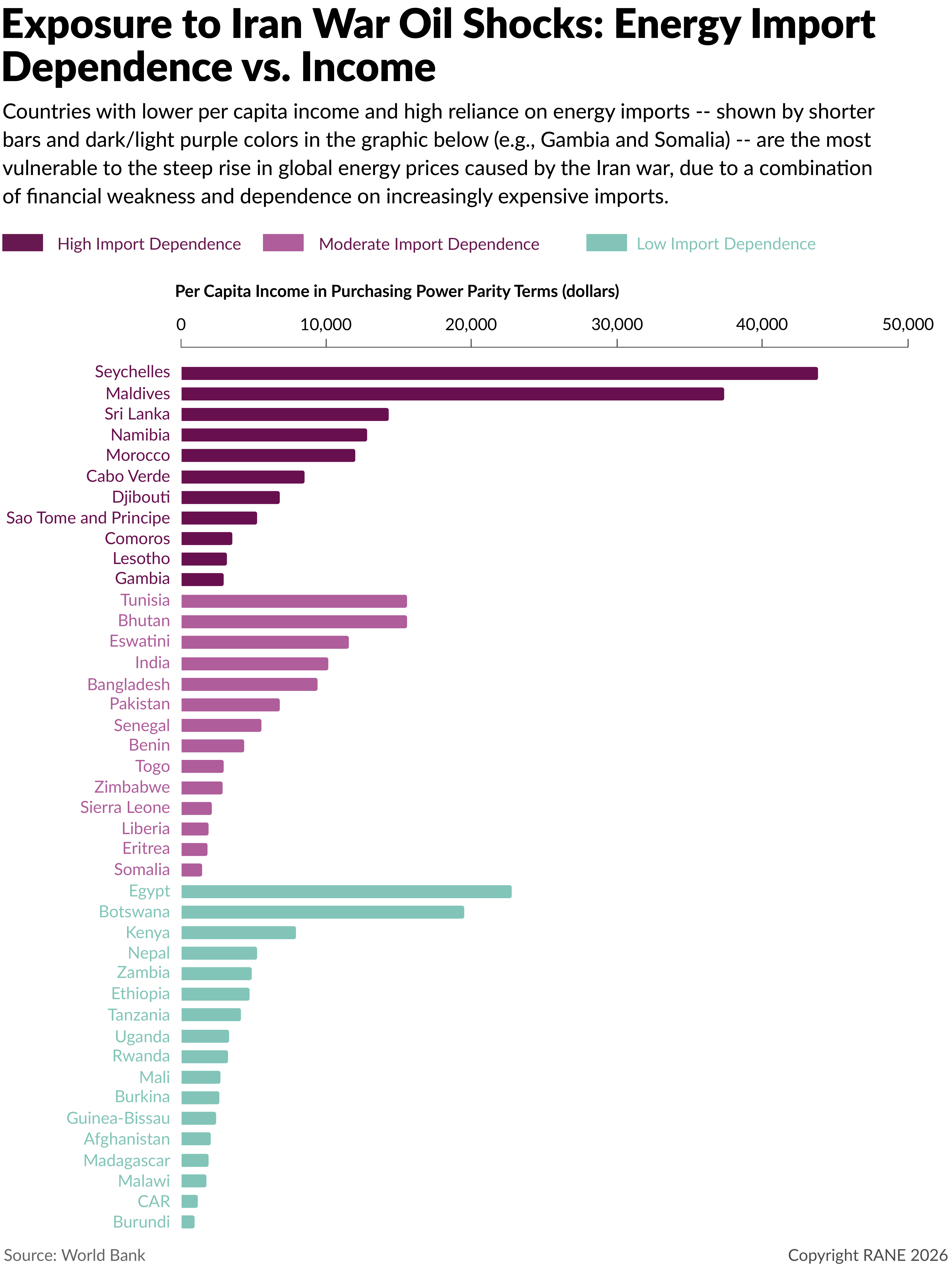

The precise economic impact of the Iran war will remain uncertain until there is greater clarity about the medium-term trajectory of global energy prices, but financially weak countries with significant net energy importers and a low per capita income will be most adversely affected in terms of balance-of-payments financing, inflation, household incomes and political stability. At the macro level, elevated energy prices will translate into higher inflation and reduced household incomes, unless governments intervene to limit price increases (though such measures, like subsidies, risk worsening governments' balance sheets). This means that governments will face a difficult choice: provide fiscal support to soften the impact of higher prices on household incomes and risk financial destabilization, or maintain financial discipline at the risk of socio-economic discontent and political unrest. Generally, traditional net energy exporters outside the Gulf will benefit from higher export revenues, while net energy importers face higher imports and concomitant pressure on their balance of payments and exchange rates. Countries with high net energy import needs will face additional inflationary pressures from a weaker exchange rate and higher imported inflation if they lack sufficient foreign-exchange reserves to stabilize their currencies. Financially weak countries will find this difficult and will be forced to choose between a balance-of-payments crisis and higher inflation. Therefore, the impact of higher energy prices will be substantially more pronounced, both economically and politically, in financially vulnerable countries that are significant net energy importers and characterized by low per capita income levels, a group that includes many countries in South Asia and sub-Saharan Africa. Finally, the closure of the Strait of Hormuz has increased the cost and reduced the availability of fertilizers, which will lead to lower crop yields and, in turn, higher food prices later in the year following the current planting season in the Northern Hemisphere. Higher food prices will raise the risk of social unrest and protests, especially if financially weak governments are also forced to implement unpopular austerity measures, like spending cuts, to maintain fiscal discipline and reassure investors. This inflationary pressure will be particularly severe in countries with low per capita income, where food accounts for a larger share of household spending.

- Among African countries that import over half of their energy supplies, the Gambia, Lesotho and the Comoros are particularly vulnerable to higher prices due to their low per capita income. Among African countries that import 25-50% of their energy supplies, low-income Somalia and Eritrea will be hit the hardest. In South Asia, Sri Lanka is highly dependent on energy imports, but benefits from upper-middle-income levels. Similarly, India, Pakistan and Bangladesh are sensitive to higher oil prices due to their combination of medium energy dependence and medium income levels. Finally, Afghanistan's energy dependence is low, but it also has a very low per capita income.