Editor's Note: This is a complimentary piece of content we share from our Core Intelligence platform. RANE’s foundational intelligence product covers four major categories of risk: cybersecurity, physical safety, geopolitics, and compliance. Core Intel allows our clients to view risk through a unique, integrated lens, providing situational awareness across multiple risk categories. Contact us to learn more.

Labeled derisively by the political right as "woke capitalism" and championed by the left as a vital component of sustainable business, environmental, social and governance (ESG) issues feature prominently in the national political conversation ahead of the 2024 U.S. presidential election. Companies seemingly face the prospect of an uncertain business environment full of competing regulatory and political priorities, as well as reputational risk stemming from the divide. Despite the uncertainty, however, ESG will remain a prominent feature of the business environment. Developing defensible ESG programs will, therefore, assist organizations in managing risk and realizing opportunities regardless of the election outcome. RANE spoke with Ashley Walter, Partner-in-Charge of the ESG practice at Orrick Herrington & Sutcliffe LLP, to help organizations chart ESG strategies that will withstand clashing political will.

The Politicization of ESG at Both a Federal and State Level

Public discourse about ESG programs and demand for ESG-related data has grown in recent years. Stakeholders such as employees, customers, investors, regulators, legislators and communities now expect transparency around ESG corporate action and rigor behind ESG disclosure. As the concept has grown, so have efforts to thwart it. Critics of ESG argue that basing business decisions like investments, capital allocation or board composition on ESG paradigms prevents companies from reaching their potential. Critics also describe some ESG requirements as onerous and distracting; subjectivity and poorly defined criteria contribute to these critiques. Further, critics of ESG contend that ESG-based decisions may breach fiduciary requirements to maximize shareholder value in favor of a social agenda. By contrast, ESG proponents argue that companies should incorporate ESG into their business strategy as part of an emphasis on corporate responsibility that extends beyond profits. These opposing forces are reflected in the diametric policy positions presidential candidates have adopted in campaign rhetoric. Despite the opposing positions incumbent Joe Biden and candidate Donald Trump have taken with regard to ESG issues, Walter anticipates that regardless of who is elected president, ESG as a corporate objective will not be pared back, as there are too many ESG drivers outside of regulation that are exerting pressure on companies.

Although ESG as a corporate objective will likely not diminish in importance, the clash of views being heightened by the polarized political atmosphere ahead of the next presidential election does mean that ESG is in the spotlight, and tensions surrounding ESG matters will result in a higher degree of scrutiny and challenge by stakeholders. Republicans like then-presidential candidates Vivek Ramaswamy and Florida Governor Ron DeSantis capitalized on the divisive nature of ESG by making ESG opposition a key issue during the Republican primary debates throughout 2023. In response to their anti-ESG positions, presidential candidate Trump published a campaign video in which he called those who promote ESG-themed investments "sick." In the video, he promised, if elected, to sign an executive order "to support a law to keep politics away from Americans' retirement accounts forever." By conflating ESG with socialism, these critics portray ESG as anti-capitalist and anti-American. This aggressive rhetoric reflects Republican fears that ESG funds are an attempt to smuggle progressive political priorities into corporate boardrooms. Although noisy, the impact of anti-ESG rhetoric, as described here, according to Walter, will likely be limited due to the fact that corporate executives do assign value to ESG and, if anything, will likely increase investment going forward. Still, the impact of the anti-ESG sentiment will be felt through pressure on organizations from right-leaning constituents, as well as pressure from politicians at the state level.

Republican opposition to ESG stands in contrast to President Biden's efforts; on Aug. 16, 2022, he signed the Inflation Reduction Act (IRA), billed as the largest piece of climate legislation in U.S. history. The IRA includes tax incentives and other provisions intended to help companies tackle climate change, increase investments in renewable energy, promote the adoption of electric vehicles and enhance energy efficiency, advancing a trend that has been growing steadily. Democratic governors in states like Massachusetts and Washington have capitalized on unified control of state legislatures, moving ESG legislation forward and investing state funds with asset managers who incorporate ESG criteria. Governor Whitmer of Michigan, a battleground state in presidential elections, was able to ratify climate legislation in November 2023.

Under President Biden, anti-ESG initiatives are out of line with the federal government's stance and would likely continue to be so if Biden is re-elected. Biden touted the IRA in his 2024 State of the Union, suggesting his administration would continue to prioritize ESG-related policy. However, should Trump return to the White House in 2025, he could offer a degree of political cover by aligning the federal agencies with some of the more conservative elements of ESG pushback or amplifying aggressive rhetoric. In fact, conservative organizations have developed a roadmap for a potential Trump presidency entitled Project 2025, which aims to roll back ESG-related policies –especially those that are climate-related – and government research related to ESG topics. The potential shifting state-federal alignment on ESG, particularly in areas with disclosure implications, would create additional pressure on those who have prioritized ESG in their business decisions.

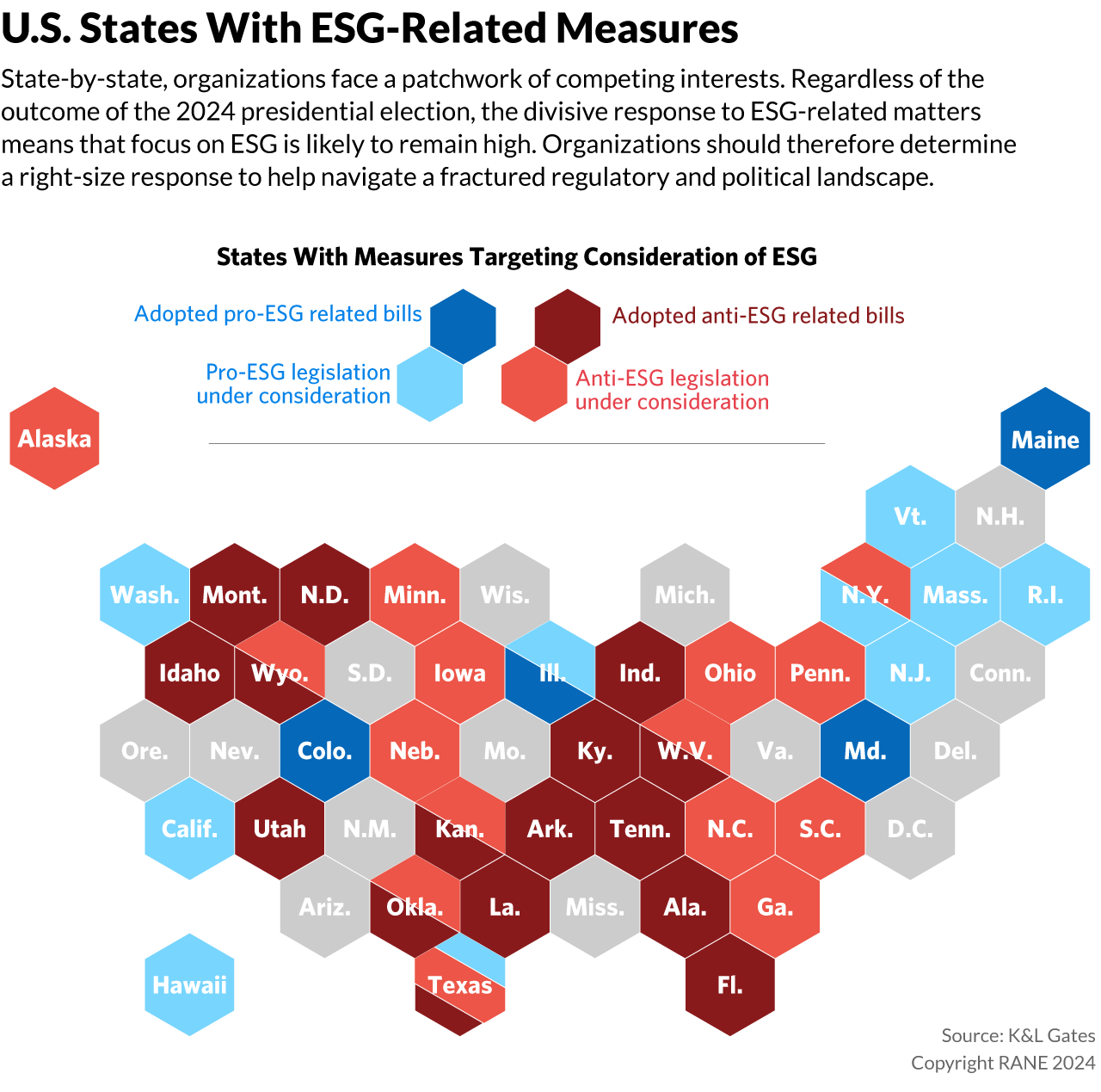

Further highlighting the political challenges facing corporations, New York, California, Texas and Florida are engaged in a fierce battle to make ESG a prominent feature of state policy (NY and CA) or remove it from consideration completely (TX and FL). These states are significant because of their unique combination of economic power (they are the four largest state contributors to GDP, according to the most recent data in 2022) and population (they are the four most populated states in the United States). Governors and legislators in all four states have investment policies and rhetoric that have subsequently been exported to other states around the country; doing business in one jurisdiction has compliance and reputational implications in another. Governor DeSantis of Florida, for example, released an "Economic Declaration of Independence" during his unsuccessful campaign for the presidency; the declaration was an attempt to remove any ESG-related ideologies from the marketplace. Governor Abbott of Texas' legislative approach had similar aims; more than a dozen other states joined the effort.

While ESG-related legislation will likely follow a predictable path in deep blue and deep red states, it is on the side of enforcement where companies can glean valuable intelligence. With the volume of anti-ESG legislation steadily rising (for example, Utah passed five such bills in 2023), enforcement actions could be expected to increase. However, enforcement actions are relatively rare. Lagging enforcement suggests that legislation is more about political posturing than preventing violations of the law. It also could indicate that, in keeping with RANE's discussion with Walter, ESG remains well-embedded in the business ecosystem. Walter's observations are also reflected in a 2023 Deloitte poll of executives, which found that more organizations are adding ESG-related personnel to oversee governance and control; the personnel decisions reflect an acknowledgment of ESG's role in business strategy, even in the current political environment.

Stakeholders Learning to Navigate Competing Political Priorities

Consideration of ESG's role in business strategy is not a new development. A 2004 report from the United Nations titled "Who Cares Wins" encouraged all business stakeholders to embrace ESG long-term, and over the past decade, pressure from stakeholders has grown dramatically. Customers and consumers have increased their sustainability and social expectations of companies, and, in response, investors have increasingly sought opportunities to make commitments to funds with an ESG focus. However, after years of growth, sustainable funds in the United States suffered their first calendar year of outflows in a decade, as sustainable investing has been critically scrutinized by some Republican politicians, and accusations of greenwashing have drawn the attention of investors and regulators.

Between 2020 and 2022, data collected by Morningstar Direct indicates that there was an average annual introduction of nearly 100 new launches of U.S. funds touting ESG characteristics. This activity led to some new or existing funds adding "sustainable" to the fund name in order to take advantage of the interest surrounding and money flowing into sustainable strategies. As these deceptive or misleading marketing practices by U.S. investment funds came to light, regulators were compelled to crack down on the rampant greenwashing in the asset management industry. On Sept. 20, 2023, the U.S. Securities and Exchange Commission (SEC) changed its "Name Rule" to require more funds to adopt an 80% investment policy –i.e., that 80% of a fund's portfolio matches the asset advertised by its name – including funds with names that reference a thematic investment focus, such as the incorporation of one or more ESG factors. This rule change follows several years of SEC focus on prosecuting ESG-related misconduct and greenwashing via enforcement actions and fines.

In addition to efforts by the SEC to combat greenwashing, by the end of 2023, 18 states had introduced some form of legislation restricting the inclusion of ESG as investment criteria, leading some major asset managers to remove "ESG" and "sustainability" labels from some fund names. In early 2024, Republican state legislators made attempts to go further; if passed, a pending bill would criminalize investing public funds with an asset manager who gives "any regard" to ESG criteria. Pushback on ESG has at least partially resulted in downplaying ESG during official company communication. For example, on earnings calls, mentions of ESG rose steadily until 2021 and have declined since, according to a FactSet analysis. In the fourth quarter of 2021,155 companies in the S&P 500 mentioned ESG initiatives; by the second quarter of 2023, that had fallen to 61.

In light of critical attention from regulators and politicians, just 66 new sustainable funds were launched in 2023. While the slowing of fund launches, in combination with net outflows, can partly be attributed to legitimate pushback on greenwashing and investors' outlook on markets generally, in the United States, and particularly in "red states" where some of the large fund managers are based, anti-ESG sentiment and political backlash has greatly impacted appetite for ESG exposure. In March 2023, a group of Republican attorneys general sent a letter to 53 of the largest U.S. fund firms, questioning them about their membership in the industry groups and describing what it called "potential unlawful coordination" with Climate Action 100+ (CA100+), a global investor coalition pushing companies to reduce emissions. On Feb. 15, 2024, the investment arms of JPMorgan Chase and State Street decided not to renew their memberships of CA100+, and BlackRock transferred membership to its international arm. On March 1, 2024, Invesco and bond giant Pimco withdrew from the coalition.

Despite the quieting of major asset managers in response to political pressure, interest in ESG remains high. According to survey findings in the "Sustainable Signals" report by Morgan Stanley Wealth Management, published in January 2024, more than three quarters (77%) of individual investors globally say they are interested in investing in companies or funds that aim to achieve market-rate financial returns while also considering positive social and/or environmental impact. In addition, 57% say their interest has increased in the last two years, while 54% say they anticipate boosting allocations to sustainable investments in the next year. A March 2024 survey from business data and reporting solutions provider Workiva found that despite the recent political backlash against ESG and sustainability reporting initiatives in the United States, more than 80% of North American investors say that they have not changed how they make investment decisions, and an even larger majority appear to be in favor of new and emerging ESG disclosure regulations. Approximately nine out of 10 investors believe that new sustainability reporting regulations – specifically the European Union's Corporate Sustainability Reporting Directive, the SEC's (now-finalized) climate disclosure rule and California's climate disclosure laws – will help them make more informed investment decisions. This aligns with Walter's belief, derived from his experience with clients that from a corporate perspective, companies are still highly focused on ESG issues and understand that ESG is often critically important to key stakeholders.

Even though he has worked as an ESG lawyer for over a decade, Walter says that only recently has he seen a proliferation of ESG efforts driven by non-government stakeholders. To illustrate this, he notes that during the Trump administration, ESG interest and initiative adoption increased among the companies he worked with. Walter indicates this was partly due to the fact that companies were receiving pressure from customers. Those priorities flowed down to suppliers and vendors, creating a business ecosystem that powered the ESG movement despite an ESG-unfriendly administration from 2017 to 2021. In another illustration of this point, former Vice-President Al Gore noted in a February 2024 interview with Bloomberg that green investment and progress towards net zero continued even during Donald Trump's presidency.

Walter adds that if the next administration puts in place additional ESG-related laws, such as climate regulations, such a development would likely accelerate the pace of adoption of ESG programs, but that he does not believe there will be a material decrease in corporate ESG initiatives or focus no matter who is elected. One notable example of a continued push towards ESG-themed regulation is the March 6, 2024 finalization of the SEC's long-expected climate disclosure rule mandating publicly traded companies to report greenhouse gas emissions, carbon commitments, climate-related risks and transition plans –– even if the final regulations were significantly scaled-back. Companies could, therefore, be empowered to act independently on ESG matters.

Walter also notes that anti-ESG sentiment from Republican-led governments on both a state and federal level has actually spurred pro-ESG activity from public and private players, so even if Donald Trump is elected in 2024, Walter notes the possibility of increased pro-ESG pressure.

How to Develop a Right-Sized Strategy

While Republican-led efforts at the state and federal levels are challenging aspects of ESG, regulators, large investors, customers, employees and other stakeholders are still asking for or demanding information and responses on ESG-related issues. It is this convergence of opposing sentiment in the United States that Walter believes has created an opportunity for a healthy assessment by organizations on how to develop a plan for clear and consistent communication to key stakeholders around ESG efforts. This begins by defining the company's ESG goals and providing specific information about the 'why' and 'how'; once defined, organizations should proactively and consistently share progress, regardless of where they are in their journey. Demonstrating tangible progress is important when communicating ESG impact, and communications should include clear metrics that are relevant to a company's specific business, industry and approach. Updates on progress and commitments also help organizations avoid 'greenwashing' accusations. It is also important to continue to revisit ESG goals and ensure they are still aligned with the overall goals of the business and its long-term plans. If the goals no longer serve the business best, organizations need to clearly communicate the metrics that informed the decision to increase or reduce those efforts.

One thing that the anti-ESG movement has done, which Walter considers healthy, is create a discourse that has forced organizations to think critically about how ESG intersects with their business strategy. The salutary thing for organizations to do in light of a contentious environment, Walter advises – if a company is not already operating in this manner – is to right-size ESG for their operations in order to avoid overreach and ensure resources are effectively deployed. Having meaningful conversations to determine what is strategically appropriate will help organizations confirm or change what they are doing with regard to ESG issues.

Walter recommends identifying opportunities to scale up investments or determine that a shift in focus or resources is needed. Companies should evaluate and select an ESG maturity model as a framework that can be "used to ensure that ESG programs advance in a way that is consistent with core strategy, value generation and the specific characteristics of the business." Walter sees such a model as a tool for implementing ESG objectives and evaluating their effectiveness for the purposes of improvement. Walter stresses that, above all, ESG must align with both the company's strategy and the company's culture. A thoughtful and well-designed ESG program will have appropriately tailored and defensible ESG strategies. Committing time and resources to develop specialized, evidence-based ESG solutions will better prepare organizations to withstand criticism and litigation. An ESG program designed and built around defensible principles will be well-positioned to play a meaningful role in securing new customers, unlocking cost efficiencies, attracting and retaining talent, reducing risk, enhancing reputation, and, importantly, withstanding anti-ESG criticism.

Walter does not advise taking a "wait and see" approach when it comes to structuring ESG programs around the president's political agenda. Walter says that anti-ESG efforts have already forced companies to be more rigorous about their programs. The result is that most are well-positioned for what comes, no matter who wins the election.

Although, as discussed, there has yet to be jurisdictional alignment on ESG requirements or standards, both mandatory and voluntary, Walter believes there is a convergence of standards that will help organizations manage complexity. Despite the political uncertainty, he says, organizations can start to work on a key set of work streams guided by internationally recognized standards that are already being incorporated into many different laws and regulations, such as California's SB 261 and the SEC's now-finalized climate rules. Regardless of who is elected U.S. president in the upcoming election, Walter suggests that it is a good idea for companies to begin to structure the environmental aspects of their ESG programs and disclosures using internationally recognized frameworks.

About the Expert:

Ashley Walter, (Partner-in-Charge, ESG) Orrick Herrington & Sutcliffe LLP, advises technology and life sciences companies on strategy, oversight and compliance with respect to ESG measures. He frequently assists companies in launching and advancing ESG programs by advising on the formation of management-level ESG Steering Committees and ESG Working Groups, serving as a facilitator at meetings and supporting reporting to executive management, the board and external stakeholders. Ashley is a co-founder and past chair of the Corporate Social Responsibility Law Committee of the ABA Business Law Section, has taught the course "Corporate Social Responsibility" as a Lecturer in Law at Stanford Law School and is a co-editor of The Lawyer's Corporate Social Responsibility Deskbook, a resource for legal departments and outside counsel. He has co-chaired the Practicing Law Institute's annual full-day ESG program for the last three years.