Editor's Note: This is a complimentary piece of content we share from our Core Intel platform. RANE’s community-based solutions help address a range of enterprise risks covering Safety + Security, Cyber + Information, Geopolitical, and Legal, Regulatory + Compliance. Contact us to learn more.

RANE's Network Intelligence Report incorporates our analysts' diverse expertise to assess risks and opportunities pertinent to our clients across our taxonomy's four areas of focus: geopolitics; legal, regulatory and compliance; cyber and information; and physical safety and security.

Although we only began conceptualizing this special Navigating Multipolarity issue of the Network Intelligence Report towards the end of 2022, it has been clear for several years that the era of unchallenged U.S. hegemony – and of the broader Western-led global order – is over. The Russian invasion of Ukraine is only the most recent and acute demonstration of this, but more broadly the rise of China and the emergence of multiple small and middle powers have introduced a great deal of uncertainty into the global environment. Even a more integrated Europe, though still close to the United States, has created new challenges as Washington and Brussels pursue divergent policies in many areas, such as tech and environmental regulation.

Our Network Intelligence Report begins with an overview of what this emerging multipolar world looks like and the implications for organizations trying to navigate it. As we are keenly aware, business leaders across industries and company sizes have identified geopolitical risk as a key concern in 2023. Our analysts examine five key areas of this new world order that are highly relevant to our clients.

One of the defining characteristics of the emerging global environment is a decline in the relevance and effectiveness of the Western-led multilateral political, economic and security institutions that emerged in the wake of World War II. In particular, the rise of alternative lending institutions and business norms, many of which are championed by China, creates new legal, reputational, financial and operational risks to organizations.

Just as new multilateral institutions are increasingly dividing the physical world, so too are countries increasingly resorting to nationalism in cyberspace. What was once a global commons is increasingly split along national or regional lines. This is creating a much more complex and protectionist digital landscape for organizations to maneuver and protect their data.

Countries are also growing more protectionist in their environmental policies as they seek to pair action on climate change with state-led economic intervention. While China has long done this, it is the United States that has more recently and unexpectedly led this charge, forcing Europe to respond. This is already creating compliance challenges, which are set to only grow in the coming years, for multinational businesses.

If these challenges are not enough, legal and compliance teams are also facing a growing array of sanctions requirements. Though most immediately focused on Russia, Western nations are expanding and in some cases wholly redesigning their sanctions architecture in ways that will make it crucial for all organizations to improve their due diligence practices to avoid legal or reputational blowback, especially as regulators turn their focus toward China.

Finally, a shifting and more uncertain world will make it more important than ever that organizations have a model and tools to evaluate and mitigate the various risks future crises may bring, especially for physical security. Applying a framework from the U.S. Intelligence Community that leverages the proliferation of open-source intelligence for a corporate context offers one well-developed way forward.

We strongly believe that you will find this special Navigating Multipolarity issue of the Network Intelligence Report a useful guide to this emerging multipolar world order. As always, we are indebted to the work of our talented analysts and expert contributors, whose observations and guidance frame each advisory.

Sincerely,

Sam Lichtenstein, Director of Analysis, RANE

Geopolitical Disruptions: The Return of Multipolarity

The reemergence of a multipolar world and rising peer competition is changing the global security and business landscape. Defense budgets are climbing. National security considerations are driving geo-economic competition. Global norms and expectations that have held for decades are in flux. Complex supply chains woven since the end of the Cold War are fraying. Adapting to this shifting global landscape will require rethinking longstanding assumptions, but also understanding the geopolitical forces driving change.

Multipolarity is not new – in fact, it may be the norm of the modern globalized world. With the exception of the Cold War and a brief period of re-adjustment following the collapse of the Soviet Union, modern global history has been characterized by a multipolar world system. No power was able to hold sway over the rest singularly. Even at the height of British imperialism, the UK was not the clear global hegemon, as seen in its continued struggles to manage competing powers on the European continent as well as Russian advances in Central Asia toward South and Southeast Asia – the so-called "Great Game." No truly global bloc formation emerged until after World War II. Instead, the global balance of power was fluid.

From Globalization to Liberal Economics

From a geopolitical perspective, which seeks to take the long, structural view, the "modern" world began sometime in the early 16th century, when Europe "discovered" the rest of the globe. Before this time, there were empires rising and falling, cultures emerging and developing, and science and technology advancing, all over the globe. And there were connections moving people, goods and ideas across Europe, Asia and Africa. But distance remained a major constraint on global connectivity, and it took the combined advances in shipbuilding, navigation technologies and economic resources to bring the globe into clear focus and integration.

By the 19th century, global trade, strategic competition and shifting technology meant that the world was a closed political system. As British geographer Sir Halford Mackinder assessed in 1904, "every explosion of social forces, instead of being dissipated in a surrounding circuit of unknown space and barbaric chaos, will be sharply re-echoed from the far side of the globe, and weak elements in the political and economic organism of the world will be shattered in consequence." In other words, what happened on one continent had repercussions for those on other distant continents and vice versa. Thus the American Revolution had significant implications for Britain's security in India (and affected London's dispersion of force and decision-making), and the expansion of European sea trade to the Far East degraded the economic viability of Central Asian trading routes (and the fortunes of the Italian city-states).

With the integration of the world into a single system, fully cognizant of itself, we can trace the origins of today's globalization to the early 1500s, with sporadic maturation over the succeeding centuries. But it is only after World War II that the modern framework for globalization emerged. At the end of the war, the United States stood as one of the few strong economic powers, and Washington used this heft to rebuild Europe and establish a new global economic and philosophical framework. Modern liberal economic policies may have their origins in older eras and theorists, but it was the widespread destruction of World War II that allowed the construction of a new liberal economic framework, which took on more importance as the world quickly moved into the Cold War architecture.

The Cold War was both a strategic and ideological competition. The United States and Western Europe promoted a liberal ideology that linked personal freedoms, private industry and democracy as the fundamental (and universal) conditions for economic growth and success. This challenged Soviet collectivism and statism, but it also challenged other traditional forms of economic and social collectivism that characterized much of the developing world. When the collapse of the Soviet Union "proved" the superiority of Western liberal economics, the West could demand adherence to its norms amid the rapid expansion of global trade, trade agreements and economic interactions. Thus, one abnormal period (the bipolar Cold War) gave way to another oddity, the "hegemonic" moment of U.S. power that lasted until the early 2000s. This was a transitory period where the rest of the world sought balance, particularly the rapidly growing China.

Challenging the Status Quo

China stands in stark contrast to the universal assertions of Western liberal economic norms. While China made some economic progress through the 1980s, it was the 1990s and early 2000s that saw the real surge in Chinese economic growth and global importance. China was well positioned to take advantage of its massive low-cost labor pool to draw industrial investment and link into the rapidly expanding containerized shipping. Global norms and trade agreements facilitated the growth and complexity of global supply chains, allowing corporations to move goods at various stages of completion to different countries, with products at times crossing oceans several times before reaching their final destinations. China played within this system when it was beneficial, but Beijing never gave up state involvement in the economy or Communist Party control over the government and people.

As China's economic power rose, and its importance to global trade flows increased, Beijing grew more confident in beginning to challenge aspects of the global (i.e. Western) norms, highlighting its own successes in economic growth without the same political or personal freedoms the West asserted were necessary co-requisites. Beijing's message resonates with much of the world. The Western liberal economic and political ideas are not inherently universal, but rather come from a particular strand of philosophy and were codified at a unique moment in history. But the North Atlantic no longer comprises the bulk of global economic activity and heft. Thus, China argues, the West's mores should not necessarily dictate the political, economic and social choices of other countries.

China is not alone in challenging the status quo. As U.S. power seemed to grow unchecked following the collapse of the Soviet Union, the rest of the world sought balance. Freed of the Soviet threat, Europe accelerated its own integration, creating a massive single market that gave Brussels power in asserting global norms on issues ranging from the environment to human rights. Russia perceived unchecked U.S. power, and the expansion of NATO, as a direct threat to its own strategic position, and by the early 2000s began its own push against the global order. As these four poles of power became clearer, small and middle powers like Turkey, India and Japan saw the opportunity to begin exploiting the differences between the big powers, finding their own advantages where they may, but also introducing uncertainty into political and economic policies as they bucked against U.S., European, Chinese and Russian interests, or saw local politics swing between different big power influence.

Challenges and Opportunities of a Multipolar System

The United States and China sit at the core of the new multipolar system, with Europe and Russia as similar but not fully aligned poles – and an array of small and middle powers shifting throughout this new ecosystem. But despite growing U.S.-China strategic competition, it is unlikely the world returns to another Cold War-like architecture. Unlike at the end of World War II, there is no massive dislocation of global trade and peoples that can allow the formation of a new competing set of economic and political blocs. Rather, no single power has the ability to either dominate the international system alone or force other countries to fully choose a side. This has strategic and economic implications not only for government policies and international relations but for internationally engaged and exposed businesses and organizations.

- Uncertainty in international relations: Multipolarity provides space for many small and middle-tier countries to decline "choosing a side" between big powers, leading to more flexible alignments rather than expanding strong alliances. In the Indo-Pacific, for example, many countries are finding themselves largely aligned economically with China while militarily with the United States. This may make them more susceptible to economic coercion from big powers, and economic impacts are often based less on the economic fundamentals in a specific smaller country than on the political actions of the larger powers. Thus, unexpected economic disruptions may become more common, requiring not only adept political risk awareness that draws on the expanding amount of open-source intelligence but an understanding of the broader geopolitical balance as well.

- Emergence of miniblocs: While traditional large-scale complex alliances may be waning, the multipolar system encourages the frequent formation of smaller mini-blocs, attempts by like-minded countries to pool their relative power to better maneuver between the big powers. These may be driven by the big powers, as seen in groupings like the QUAD or AUKUS, or be regionally focused, as with the closer cooperation emerging among the Baltic countries and Poland, or the renewed collaboration within the core of ASEAN. This will force businesses to navigate increasingly diverse – and at times opposed – political and economic blocs, posing new compliance, supply chain, data security and other risks.

- Rising nationalism: The challenges to assertions of universal norms (such as Western liberal economics) and the impact of re-emerging great power competition drive renewed nationalism and protectionist tendencies, even on topics like climate change that are truly global challenges. As the global trade system undergoes structural realignment, big powers employ geo-economic tools against one another and ideas of economic security as a key component of national security are revived, protectionist actions and greater state involvement in economics and industry become both more normal and more acceptable. And this moves well beyond the issue of trade, or ideas of near-shoring and friend-shoring. It is also rapidly expanding into new territories, such as information and cyber-sovereignty, and expansion of traditional ideas of air sovereignty to now include space.

- Fraying of global financial architecture: While there is little likelihood of a near-term replacement of the U.S. dollar as the global reserve currency, its dominance and the global financial architecture give Washington disproportionate power to use economic tools to shape global political and security environments. China, Russia and many other countries are actively seeking alternatives to the dollar and existing financial infrastructure to soften Washington’s ability to punish and coerce. But this is not limited to just direct competitors to the United States. Even nominal partners, such as Middle Eastern oil suppliers, are making arrangements for alternative currency exchanges, and both China and the European Union have developed regulations that can counteract U.S. sanctions, leaving businesses in the difficult position of choosing which set of regulations to adhere to.

- More localized conflict: As nationalism rises, so does sub-nationalism, and many ethnic or regional groups within countries are asserting their own right to self-determination. At the same time, as the big powers step up strategic competition, more localized competition within and among smaller powers may devolve into military conflict. With the focus on China and Russia, the United States and Europe may be less likely to intervene in moderate localized conflict, suggesting that the threshold for intervention is shifting.

- Uncoordinated responses to broader global issues: Multipolarity makes collaborative global action more difficult. Nationalism and economic security will often take precedence over global issues, and while this doesn’t end the momentum for addressing things like climate change or illegal fishing, it may lead to more regional and local responses or actions by big powers more focused on their particular location than on the overall globe. This may be particularly notable in places like South America and the Pacific Islands – the former where we are seeing a New Left harness environmentalism as part of its challenge to outside economic exploitation, the latter where their very survival is already being challenged by climate change.

- Restructured supply chains: Organizations and corporations that have very complex multi-company supply chains, and those that have very narrow, single-source supply lines, are highly vulnerable to disruptions in the multipolar world. Resilience may require redundancy, which is costly, or more flexibility in identifying and being able to rapidly shift to alternatives in times of localized stress. This impacts not only physical goods but services and information-based products as well. Increasingly, companies will also need to develop their own foreign policy, particularly if they have heavy exposure to more than one of the big powers, or wide-ranging supply chains. Understanding multiple layers of supply, at times down to the initial minerals, will also become an important component in managing geopolitical risk and trade. This will only increase the need for organizations to have robust frameworks to proactively collect, analyze and mitigate various risks.

China's Challenges to Bretton Woods: Implications for Businesses

The rise of non-Bretton Woods institutions (BWIs) in an increasingly multipolar world has significant implications for global business opportunities and demonstrates the need for firms to modify their operational strategies to mitigate potential geopolitical, legal and financial risks. Since the founding of institutions such as the New Development Bank (NDB) in 2015 and the Asian Infrastructure Investment Bank (AIIB) in 2016, both of which are headquartered in China and guided and resourced to a significant extent by Beijing, concerns have grown that infrastructure development investment projects that these new institutions underwrite, are accompanied by a different set of rules and norms for business and investment that may diverge from the values affirmed during the Bretton Woods era. As part of Chinese President Xi Jinping's vision of the "Chinese Dream," China seeks to challenge the Western-centric global order through such projects as the Belt and Road Initiative (BRI), the new Maritime Silk Road and new multilateral development institutions that offer loan packages that appeal to developing countries and deprioritize transparency, anti-corruption and safeguards for workers, among other things. Close observers of the Chinese influence on multilateral lending by the AIIB and NDB point also to the potential linkages between lending decisions and China's geopolitical objectives. In order to better understand the legal, reputational, financial and operational risks to businesses likely to emerge as competition from non-Western multilateral lending institutions challenges the norms and practices enshrined in the values of BWIs, RANE spoke with Nathan Picarsic and Emily de la Bruyère, Co-Founders of Horizon Advisory.

The Rise of Bretton Woods and China's Recent Challenge

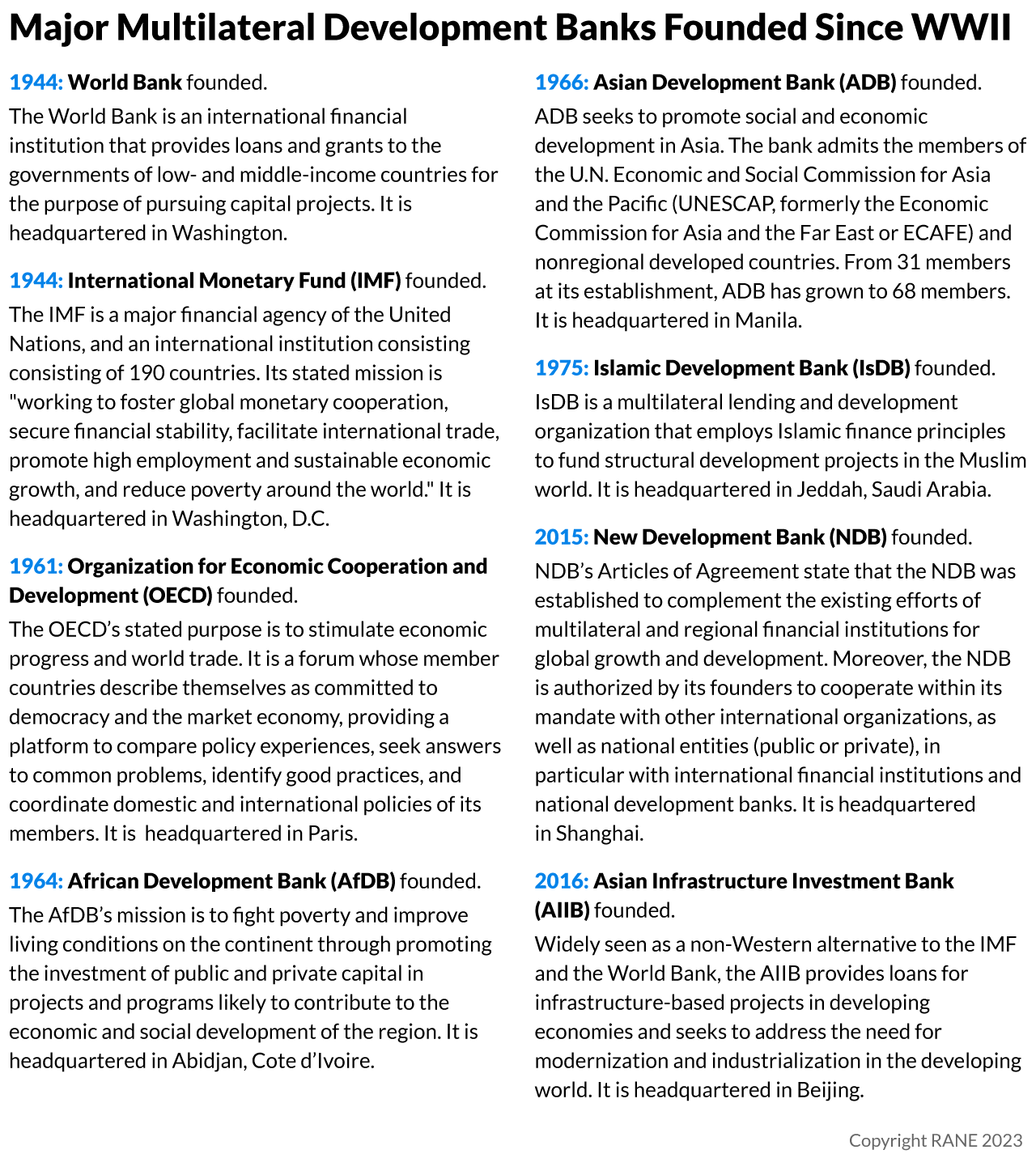

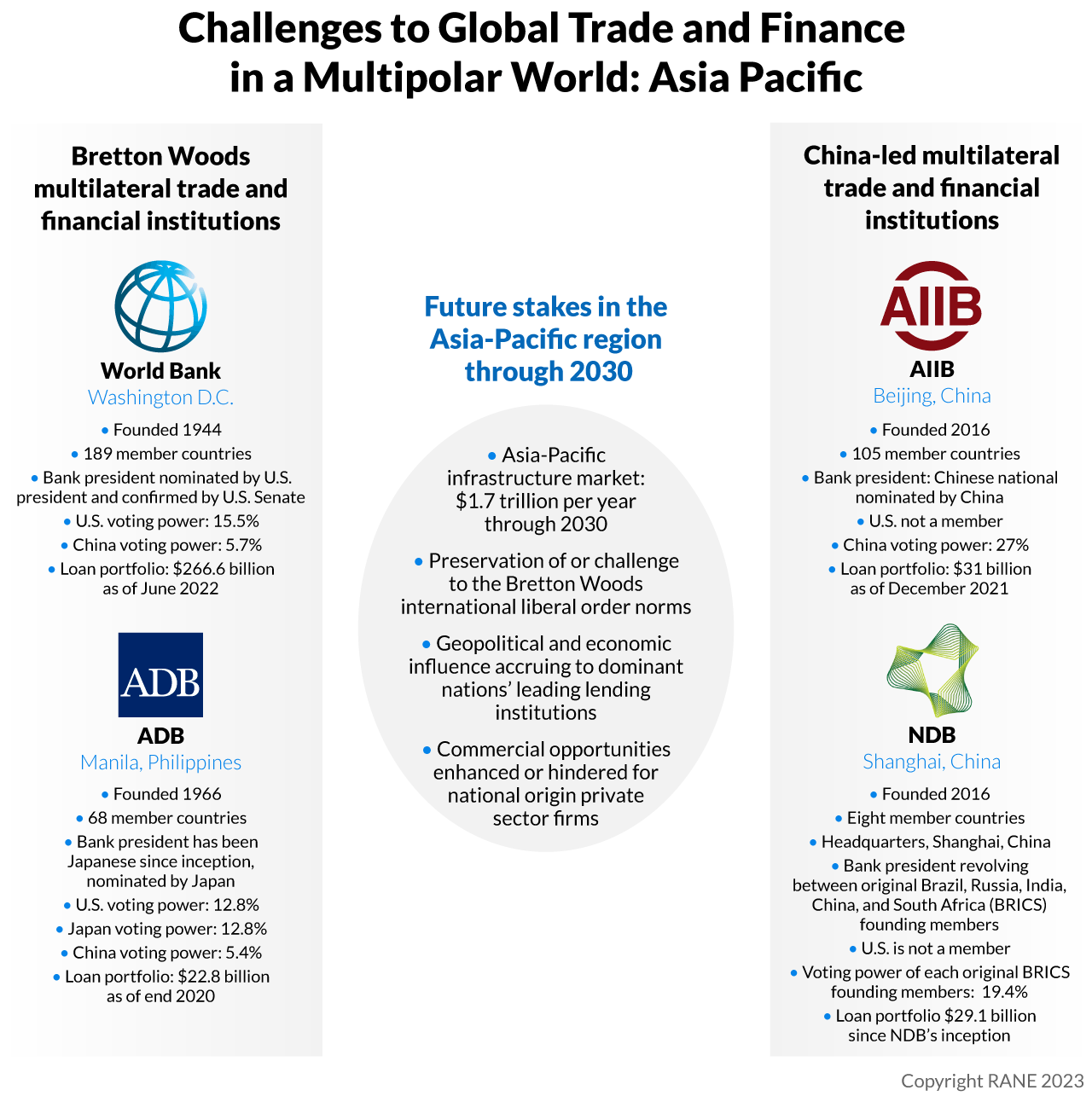

In December 1944, 44 delegates representing the Allied Powers met in Bretton Woods, New Hampshire, to discuss the formation of an international organization to finance the reconstruction of Europe following the conclusion of World War II. The primary lending institution that emerged from the conference is the World Bank Group (WBG). Composed of the International Bank for Reconstruction and Development, the International Development Association, the International Finance Corporation, the Multilateral Investment Guarantee Agency and the International Centre for Settlement of Investment Disputes, the WBG's primary mandate is to provide financing to low- and middle-income countries for development projects. The International Monetary Fund (IMF) was founded alongside the WBG with a mandate to resolve international financial crises and to correct balance of payment issues.

The BWI ecosystem has given rise to a number of multilateral development banks (MDB) focused on regional lending, such as the African Development Bank (1964) and the Asian Development Bank (1966). These MDBs have largely been organized and capitalized in a manner similar to the WBG and have adopted the same terms, practices and norms, and have participated in coordination with other WBG entities in lending activities. To supplement the activities of these MDBs at the regional level in Europe, the Organization for Economic Cooperation and Development (OECD) was established in 1961. Headquartered in Paris, the OECD's stated purpose is to stimulate economic progress and world trade. It is a forum whose member countries describe themselves as committed to democracy and the market economy, providing a platform to compare policy experiences, seek answers to common problems, identify good practices, and coordinate the domestic and international policies of its members. A brief synopsis of relevant multilateral institutions and their mandates that comprise the BWI ecosystem can be found below:

In general, the norms and behaviors of these multilateral lenders reflect those of the international liberal order established by the United States and its allies at the Bretton Woods Conference. Since the 1990s, this "international liberal order" has come to be defined by the Washington Consensus. The Washington Consensus features policy prescriptions such as fiscal discipline, pro-growth spending, market-based interest rates, free trade, privatization of state-owned enterprises, deregulation of business and basic property rights. Furthermore, integrating the Washington Consensus into its loan packages, the WBG began to require that aid recipients implement structural adjustment programs if they wished to receive new loans or adjust the interest rates on existing loans. Conceived in the aftermath of economic crises in Latin America throughout the 1980s, structural adjustment programs often require recipients to curtail social spending and implement fiscal austerity plans, leading to allegations of neocolonialism and the undermining of national sovereignty. As a result of such policies, the WBG, IMF and their affiliated institutions have been criticized by various groups and opposition leaders in recipient states as examples of Western hegemony.

As global development accelerated, the drumbeat of criticism by emerging and developing economies, most particularly China, became louder. China insisted that the governance structure of the BWIs is too tightly controlled by the United States and its Western allies, and that the investment decisions and economic support provided by the BWIs are inextricably linked to the Washington Consensus. In line with recurring geopolitical tensions between Washington and Beijing, China came to believe that it did not have appropriate voting power and influence in the BWIs to reflect its own growing economic size and geopolitical influence. The leadership of the World Bank is traditionally reserved for a U.S. representative. The IMF is run by a representative chosen from Western Europe. Even the most relevant regional MDB, the Asian Development Bank (ADB), works in concert with BWI norms and practices and is always headed by a Japanese representative.

In 2016, to correct this perceived imbalance, China established the AIIB, headquartered in Beijing, and coordinated with other emerging and developing economies countries — Brazil, Russia, India, China and South Africa (BRICS) — to establish the BRICS Development Bank, which was subsequently rebranded as the NDB, and headquartered in Shanghai. As of 2021, the five BRICS countries represented 41% of the world's population and 24% of global GDP. Furthermore, as of 2022, China alone represented nearly 18.5% of the global population and the equivalent percentage of global GDP.

The governance of the new institutions is illustrative: China controls a 26.5% voting share in AIIB decision-making, whereas the next largest vote holder is India, with 7.6% voting rights. China can control the governance of AIIB given that its voting power is greater than the 25% required to block decisions made even by a supermajority of AIIB voting members (which would require 75% of the vote by two-thirds of the Bank's members). China holds a 20% share of voting rights in the NDB, along with 20% held by each of the other four original BRICS founding members. China is the largest capital provider to the Contingent Reserve Arrangement (CRA), instituted in the same year as the NDB, which provides balance of payments assistance to BRICS countries. China has committed $41 billion to CRA, the largest contribution from the five BRICS countries, giving it 39.5% of the voting power. Although the United States is not a member of the AIIB, NDB or the BRICS-controlled CRA, Western nations such as Australia, France, Germany, Italy and the UK have joined AIIB (with a combined voting power of 13.2%), demonstrating the rise of the AIIB and NDB as viable, multilateral alternatives to the BWIs.

Unpacking the Challenges

The challenge of these China-centric institutions comes at a time of staggering investment opportunity and need throughout the world's emerging and developing economies. In its 2017 report, Meeting Asia's Infrastructure Needs, the ADB estimated that in the Asia-Pacific region alone, the investment need is approximately $1.7 trillion per year through 2030, "if the region is to maintain its growth momentum, eradicate poverty, and respond to climate change." However, the rise of China-centric multilateral institutions such as the AIIB and the NDB challenge the BWIs and their affiliates and create myriad geopolitical, reputational and economic risks, particularly with respect to the rise of a "Beijing Consensus," divergent positions on human rights, corruption and business transparency, and increasing friction in the Western alliance on shared values and competing commercial interests between the United States and Europe.

The Beijing Consensus

Picarsic and de la Bruyère both note that China appears to view the AIIB, NDB and related infrastructure initiatives as opportunities to rewrite global norms surrounding lending and economic growth in the developing world. Emblematic of this perspective is the "Beijing Consensus." Defined as a development framework that prioritizes infrastructure, active state intervention in markets and gradual market reform vs. "shock therapy," the Beijing Consensus is an extension of the policy prescriptions that have enabled the Chinese economy to lift over 300 million citizens from poverty since the beginning of the "Reform and Opening Up" period in 1978. Indeed, since 2012, China has leveraged international partnerships and the Belt and Road Initiative, a cornerstone of President Xi's development policy that seeks to provide infrastructure funding in the developing world, to provide training to over 10,000 bureaucrats in the developing world, using the sessions to extol the virtues of state capitalism and infrastructure-led development. Commenting on China's export of new norms, de la Bruyère states that "Beijing is increasing its footprint and that of its institutions and organizations internationally," suggesting that China is likely to continue this practice as it seeks to supplant the U.S.-led unipolar order. For de la Bruyère, this ideological conflict between China and the West is likely to intensify, particularly to the extent that China strengthens its "no-limits friendship" with Russia amid Russia's war in Ukraine.

According to Picarsic, this trend demonstrates how China has learned from the mistakes of the "Washington Consensus" and now seeks to use its lending power in a more appealing formula when engaging the developing world. A primary criticism of the BWIs and structural adjustment programs is that they undermine national sovereignty and breed popular resentment as people chafe at austerity measures required in exchange for financial support. Picarsic theorizes that China has "watched what the United States did since World War Two and throughout the Cold War. And I think they have updated and learned from it." By avoiding overt conflict with aid recipients in favor of an approach that champions active state intervention in markets, he believes that Beijing Consensus policies will likely continue to serve as an attractive alternative to the BWI-led order.

Picarsic also notes that Beijing may be more likely, given its close reading of the history of BWI-led investment and pushback from recipient countries, to position its own geopolitical interests more carefully as commercial and civilian engagements. This approach "won't spur the same kind of wake up call" in the West, Picarsic notes. It may give China the opportunity to present itself in a manner that does not show signs of overt military or undue geopolitical influence while behind the scenes engaging in renegotiations of lending and other financial interactions to increase China's control and influence. For example, in 2022 under the BRI, China's Export-Import Bank extended a $4.7 billion loan to Kenya to finance the country's railway system. Notably, the loan does not feature any expectations for structural adjustment programs and has drawn significant media attention for its questionable terms, portrayed as secretive and exploitative by transparency activists in Kenya. Picarsic adds that using some of the leverage China has in the global financial system through its lending will be part of Beijing's geopolitical playbook, stating that "It won't be the same sort of blunt, in your face mode." Picarsic and de la Bruyère also see China managing its economic policy to further a geopolitical goal of dividing the US relationship with Western Europe. Both comment that there is an "underrecognition of this problem" in which China appears to use economic levers in a manner that creates friction between the United States and its European allies by selectively favoring European companies over U.S. companies. In a more fractured trans-Atlantic alliance, U.S. firms may face stiffer competition in a less fair geopolitical environment and have the added responsibility of managing differing sets of compliance requirements between Europe and the United States.

Human Rights, Corruption and Norms

Within the BWI lending framework, loans are often conditioned on the adoption of policy prescriptions that protect basic human rights such as the freedoms of religion, assembly and expression. In addition, recipients of loans from the IMF and WBG must also commit to anti-corruption measures, particularly on how aid money is spent and allocated, as well as sign on to other good governance initiatives like protecting workers' rights. However, many recipient countries chafe at these restrictions and view them as neocolonial attempts to interfere in domestic governance. Recognizing this opportunity to provide condition-free financing that forges linkages with leaders in developing states, loan agreements from the AIIB and NDB omit language around human rights, anti-corruption and other good governance standards in favor of "resource for infrastructure" loan programs that are often seen as corrupt. As just one of many examples, as of 2020, Angola had received $42 billion in loans from China in exchange for access to Angolan oil.

Indeed, commenting on the deprioritization of anti-corruption in non-BWI institutions, de la Bruyère states that U.S. and Western firms that seek to bid on contracts for major development projects can become "immensely frustrated" because they cannot compete given what she calls the "corruption of the Chinese approach" and the "high degree of bribery." Therefore, as Western firms continue to seek business in the developing world, particularly in primary and raw goods markets, or as participants in the infrastructure development activities financed by these new MDBs, firms will have to be mindful of the constraints on their ability to do business given the anti-corruption and business practice norms and behaviors to which they are held accountable by their home governments.

Reputational Risk and Potential Sanctions

De la Bruyère believes that firms bidding for contracts as part of projects funded by the Bretton Woods institutions, AIIB or NDB investments will have to be mindful of "major reputational and regulatory risk." Because Chinese firms may not be held to the same regulatory and ethical standards as Western firms, consortia led by China could make decisions that run afoul of Western sanctions or other regulations. De la Bruyère suggests that firms should adopt a holistic view of reputational risks throughout the lifecycle of a deal and pursue rigorous due diligence before making agreements and continue to monitor the transaction closely. Picarsic notes that if a Chinese firm becomes aware that a competitor is doing anything that can somehow be construed as cutting corners or seeking ex parte, non-competitive support or assistance on a transaction, "the Chinese side has shown that they're able to weaponize that type of information and use it against the international competitor." The Chinese competitor may have access to Chinese government resources — including classified intelligence or surveillance technology — to potentially compromise and manipulate the international competitor via intellectual property (IP) theft, hack-and-leak cyberattacks and/or reputational attacks.

Picarsic notes the significant reputational risk faced by Western companies that have an on-the-ground local market presence and compete with Chinese firms in the kinds of project development investments that the AIIB finances. He notes "I think those risks are probably going to flow to parent entities in ways that existing compliance and oversight mechanisms probably aren't prepared to handle at the corporate level." He also points out that business activities involving Chinese entities are attracting greater scrutiny from Western politicians and regulators. For example, Disney's continued engagement with China has led to public boycotts by human rights activists such as Hong Kong democracy activist Joshua Wong. Picarsic also notes that capital markets regulators and other watchdogs will be increasingly focused on business that involves China in order to assess and mitigate sectoral exposure to human rights abuses, sanctions violations and other unethical business practices.

Related to environmental, social, and governance (ESG) standards, de la Bruyère notes that human rights issues are the first line of investigation when assessing ESG and reputational risks. For example, in July 2022, the U.S. Treasury Department's Office of Foreign Assets Control sanctioned five Chinese government officials for involvement in human rights violations against ethnic minorities in the Xinjiang Uyghur Autonomous Region. The move by the Treasury followed the publication of an advisory earlier the same month by the Treasury and the U.S. Departments of State, Commerce and Homeland Security warning companies of the reputational and legal risks of doing business with entities involved in human rights violations in Xinjiang. This followed the Department of Commerce in 2019-2020 added 37 entities to its Entity List, which flags entities with which U.S. companies are prohibited from engaging in commercial activity, or must do so under specific licenses and approvals from Commerce. De la Bruyère adds that as the incentives and abilities for official governmental watchdogs and non-state monitoring groups to uncover human rights abuses grow, this ESG risk will surface and be a bigger concern that companies will need to monitor and manage.

Picarsic adds that Western firms need to monitor closely for poor environmental performance by the Chinese firms with which they participate in development investment activities. For example, project finance agreements may have content requirements or other stipulations by Chinese finance providers that Chinese solar panels or batteries be used. The production of these materials is often done in an environmentally harmful manner. Picarsic suggests that with more global scrutiny of China-related business, and better watchdog tracking of supply chain realities, the issue of ESG compliance may become "a battleground where you see a reckoning and increasing tension between the reality of Chinese projects and the normative ambitions of ESG friendly capital and corporates."

Geopolitical Risk: Companies on the Frontline and Frayed Alliances

The relationship between China and the West has grown increasingly strained at the same time that China has assumed a more aggressive role in global finance and commerce. The COVID pandemic and the perception by some that China covered up or moved too slowly to combat the possible origin of the virus, as well as increasing concerns over Chinese intentions over Taiwan and China's crackdown on domestic dissent, have complicated China's relationship with Western countries. Even more recently, China's unwillingness to take a hard line opposing Russia's invasion of Ukraine has also been a major concern for the Western alliance. As a result of increasing tension, and the political significance that the U.S. relationship with China plays in U.S. economic and geopolitical decision-making and policy, on Jan. 10, 2023, the new Republican-led House of Representatives established, with broad consensus, a House Select Committee on China. The new committee will likely focus on Chinese threats to U.S. cybersecurity and the IP of U.S. entities, the perceived overdependence of U.S. firms on supply chains originating in China and the risk that some investments by U.S. firms in China may contribute to Chinese human rights violations or the modernization of the Chinese military. In addition, the Committee may investigate activities by Beijing to support and influence the academic study of China in the United States — namely, the use of Confucius Institutes — which it believes shape student perceptions in a manner that favors China over U.S. values and interests. Opposition to China appears to be one of the few bipartisan areas of agreement; there is every indication that U.S. relations with China will assume more politicized attention as the country moves toward the presidential election in November 2024.

De la Bruyère makes the point that China's industrial policy focuses on prioritizing Chinese companies in key strategic value chains. A continuing market risk for non-Chinese firms is the assumption that, if they are operating at a more sophisticated point on the value chain and if significant competition from China is not yet evident, they are immune to competition from Chinese firms. She says it is a mistake to ignore the preferential treatment China provides its companies or how it works to make them more competitive. De la Bruyère comments that "China's approach to international competition and power projection and as geopolitical tension escalates, is to use the private sector as a tool. China puts pressure on U.S. companies so they in turn put pressure on the U.S. government. China inflicts costs on the U.S. for the sake of geopolitical competition."

China is not only targeting the developing world but also states that have been supporters of the international liberal order and the norms captured by the BWIs. "China reaches out to other Western countries about American 'unilateralism,' and presents Beijing's approach as one that actually gives everybody a voice," de la Bruyère comments. She adds that Beijing emphasizes the economic costs of siding with Washington and suggests giving sweetheart-type deals to Western countries with the objective of isolating the United States and driving a wedge over China issues between Washington and its traditional allies. Picarsic agrees, emphasizing that one of China's objectives is to divide the United States from its allies. "In terms of Alliance maintenance and cooperation," he notes, "whether it's international trade or social and cultural trends, the Chinese are farther ahead than we give them credit for, and some of that is that we've just been looking at the wrong things." Picarsic continues to say that while the West may not see clear examples of Chinese military encroachment in areas with immediate geopolitical implications to current conflicts — such as a Chinese presence in the Black Sea, for example — there are examples in recent years of Chinese commercial and financial activities giving Beijing possible dual-use commercial and military influence over other geostrategic locations. High degrees of indebtedness to Chinese commercial lending, such as the Chinese acquisition of a 99-year lease to operate the Hambantota Port in Sri Lanka — could lead to an influx of other Yuan-denominated debt transactions that tip a sovereign nation into conceding port access, valuable raw materials or some other geostrategic asset to Chinese control.

In evaluating the trajectory of U.S.-European unity regarding China, Picarsic references the United Kingdom as a key country to track. He recalls that during the Trump administration, London aligned closely with Washington on the geopolitical threat posed by China, specifically the national security risks of allowing Chinese telecommunications company Huawei access to commercial procurement transactions that could put the privacy of communications at risk of penetration by Beijing. Picarsic points to the UK National Security and Investment Act, which came into law in January 2022. London has used the law to unwind the 2021 purchase of Newport Wafer Fab, the United Kingdom's largest microchip assembly facility, by Nexperia Holding, the Dutch subsidiary of Chinese company Wingtech Technology Co. Picarsic suggests the Newport example is illustrative and worth tracking. He believes that, if the UK continues to scrutinize Chinese investment and use the National Security and Investment Act to roll back transactions as necessary, that would bode well for the trans-Atlantic alliance with respect to working together to blunt the geopolitical threats from China coming via commercial transactions. But if the unwinding of the Newport transaction is appealed and if the United Kingdom is not able to show the resolve to use the Act to prevent Chinese commercially directed interests from accessing strategic and emerging industries, there will be cause for greater concern.

Furthermore, Picarsic raises a current test case of how China may seek to exploit the fault lines of Western alliances: the manner in which the United States and its Western allies address the discovery and recent media coverage of overseas police stations linked to the Chinese intelligence services. Various media reports have shown that China uses overseas police stations to monitor the activities of Chinese nationals abroad, harass dissidents and in some cases even forcibly repatriate them. While Picarcic acknowledges that governments' public condemnation has been fairly consistent throughout the Western world, he notes that an "interesting early indicator in the months ahead" will be the degree to which countries are willing to confront this Chinese encroachment. He poses a hypothetical question: if the response by some countries is tepid, to avoid the opprobrium of China, will that suggest that they are more concerned about losing access to Chinese markets and deals arranged through Chinese financing, such as AIIB project loan activities than such an affront to national sovereignty?

How to Respond: Practical Guidance

To limit their risk profile to these threats, there are numerous best practices organizations can implement. The primary obstacle to mitigating the legal and reputational risks of participation in potentially corrupt development projects is to obtain clarity regarding potential business partners and develop a thorough understanding of all firms involved in the life cycle of a deal. To that end, Picarsic stresses the importance of conducting robust due diligence when bidding on contracts, noting that strong due diligence can help firms "execute their compliance mandates." He further states that effective due diligence can "help with governance issues if a firm is publicly listed on an exchange." By conducting appropriate due diligence when evaluating whether to participate in a deal funded by a non-BWI institution or a Chinese-influenced firm, companies will be able to reduce their legal exposure and preempt potential sanctions if the project engages entities on a sanctions list. In particular, effective due diligence should include a thorough investigation of corporate ownership (as Chinese authorities at all levels of government have significant financial holdings in many nominally private firms) and state influence on corporate decision-making. Given that firms in China are required to host Communist Party cells if the firm employs three or more Party members, the Party-state could influence business strategy and potentially implicate partner firms in rights violations.

Moreover, in the context of reputational risk associated with non-BWI-funded development projects, firms can mitigate the fallout of frayed alliances among Western states by maintaining a low profile and avoiding direct engagement with politically-charged discussions. In practice, this means that firms must give more thought to a carefully balanced PR strategy that avoids statements or actions that could be perceived as overtly partisan or political. This approach will enable the firm to focus on business and avoid entanglement with great power competition. To complement this approach, firms can also develop a proactive media policy that assures investors and government regulators that they seek business free from bribery or impropriety. As de la Bruyère notes, because the Western world "is reluctant to engage in what rings of a return to a bipolar world," firms will have to be careful in their messaging on China-centric issues.

Both Picarsic and de la Bruyère note that ESG watchdog specialists, particularly in the human rights, corruption and environmental categories, are increasing their scrutiny of Chinese business activities, looking at the long tail of supply chains and the ecosystem of business participants in a large business transaction like complex, multiyear project finance activities. Companies may need to devote additional resources and develop more comprehensive reviews and documentation of their own ESG targets across their business as a whole, calibrating the differing expectations for ESG between the United States and Europe as necessary, and with due consideration for the ESG performance of the Chinese and other companies with which they partner or who provide business services for them.

Corporate security officers at companies with significant global business activity, particularly involving Greater China, may also need to enhance their understanding of the ongoing risk that managers and employees in their firms face with Chinese competitors that have the advantage of using government resources to monitor and manipulate those individuals. Chinese companies can use information collected about the personal lives and activities of managers and employees, as well as information about their pre-transaction activities and preliminary marketing discussions, to manipulate and create a distorted narrative that may make it difficult for these firms to continue to compete against Chinese firms for participation in transactions. Legal and compliance teams may need to create additional company processes to require structured documentation of the manner in which transactions originate and to record that compliance steps are being undertaken. This documentation also makes sense given the increasing level of scrutiny Western firms may face from home government regulators and public interest organizations.

In addition, maintaining the integrity of proprietary company plans and data is crucial, as is protecting company employees from the risks of being targeted and involved in efforts to suborn their cooperation — both of which point to a need for corporate security teams to prepare for both increased cyber and physical security threats to their data and personnel. On this point, Picarsic points out the ability of Chinese firms to "weaponize" information and use it against their competitors. The overseas police stations previously cited by Picarsic are likely designed to monitor overseas Chinese students and dissidents, but the blatant disregard for national sovereignty they represent suggests that China is capable of taking steps to secure interests that go far beyond the Western liberal order's respect for individual rights, rule of law and territorial integrity of other countries. The drumbeat of attention on all things China is likely to increase; while not engaging in fear-mongering or ignoring the very real and rewarding opportunities to participate in selective transactions with Chinese counterparts, corporate security officers may need to increase the messaging about general best practices and encourage strong internal reporting of threats and concerns regarding the company's China business given the heightened risk environment.

Navigating Growing Nationalization of Cyberspace in a Multipolar World

As the international system has become increasingly multipolar, geopolitical and national security concerns have begun to shape the boundaries of the internet, heightening compliance risks for companies seeking to navigate these competing regulatory frameworks. Some regions, such as Europe, have created a comprehensive and detailed legal framework for its citizens' data rights, in the form of the General Data Protection Regulation (GDPR), while other countries such as the United States have still not adopted a federal legal framework to address data privacy regulations. Outside of the West, other major powers like China have pursued radically different approaches to cyber regulations, reflecting a much higher level of security, evidenced by China's so-called "Great Firewall." In between, emerging powers such as India are only just beginning to bolster and revise cybersecurity policies within their respective cyberspaces amid growing foreign commercial investment in India's markets. As a result of the broad variation between different regions' approaches to regulating cyberspace and as geopolitical tensions rise, businesses will have to grapple with a number of compliance requirements, heightening their reputational and financial risks as a result of the shifting regulatory landscape. To better understand how the internet is changing and which forces are driving this fragmentation, RANE spoke with Ronald Marks, President at ZPN National Security and Cyber Strategies; John Wunderlich, Senior Advisor at Privacy Pro; Michael Morrissey, Chief Information Security Officer at PrivacyEngine; and Andrea Little Limbago, Senior Vice President of Research and Analysis at Interos.

The Move Toward Securitizing Cyberspace

As the digital revolution over the past few decades has grown to encompass most aspects of daily life, many governments have realized the vulnerabilities posed by the open nature of the internet. While digital communication has vastly improved the convenience of sharing information, the internet has also had major implications for national security, individual user privacy, and commercial and economic interests. These realizations have resulted in many governments pursuing different strategies to better protect digital information within their respective cyberspace.

- Marks first points to the infrastructure of the internet, as it was originally designed, highlighting the fact that the way it was built did not prioritize security. He notes that "It wasn't built to regulate … in fact it was deliberately built the other way — so you could just put whatever out there you wanted to. And that of course has run into the kinds of problems of any mature industry where it was nice when everyone was playing nice but now we have unexpected challenges with it."

- Wunderlich further elaborates on how this natural insecurity has heightened nations' awareness of the dangers posed by an unregulated internet, stating that "A lot of countries — irrespective of left, right, center, up, down, sideways in terms of the orientation of the government — are reexamining, for a number of reasons, why free flows of data turned out to be a bad idea." To many experts, the internet has already begun to fracture. In fact, from Marks' point of view, "There's already a Balkanization of the internet … The question is how far it goes."

- In addition to the internet's lack of natural privacy protections, Wunderlich further highlights that data has increased rapidly in commercial value. As he explains, "The more significant data becomes economically, the more it intrudes on the stage of geopolitics and therefore national interests are engaged." Geopolitical tensions, especially between the United States and China, have increasingly included an economic component as both countries seek to advance ahead of the other in a number of strategically important sectors. The heightened value of digitized information, including proprietary data, personally identifiable information (PII) and other sensitive data has added another rationale for governments to try to take greater control of cyberspace.

The European Union, the GDPR and the United Kingdom

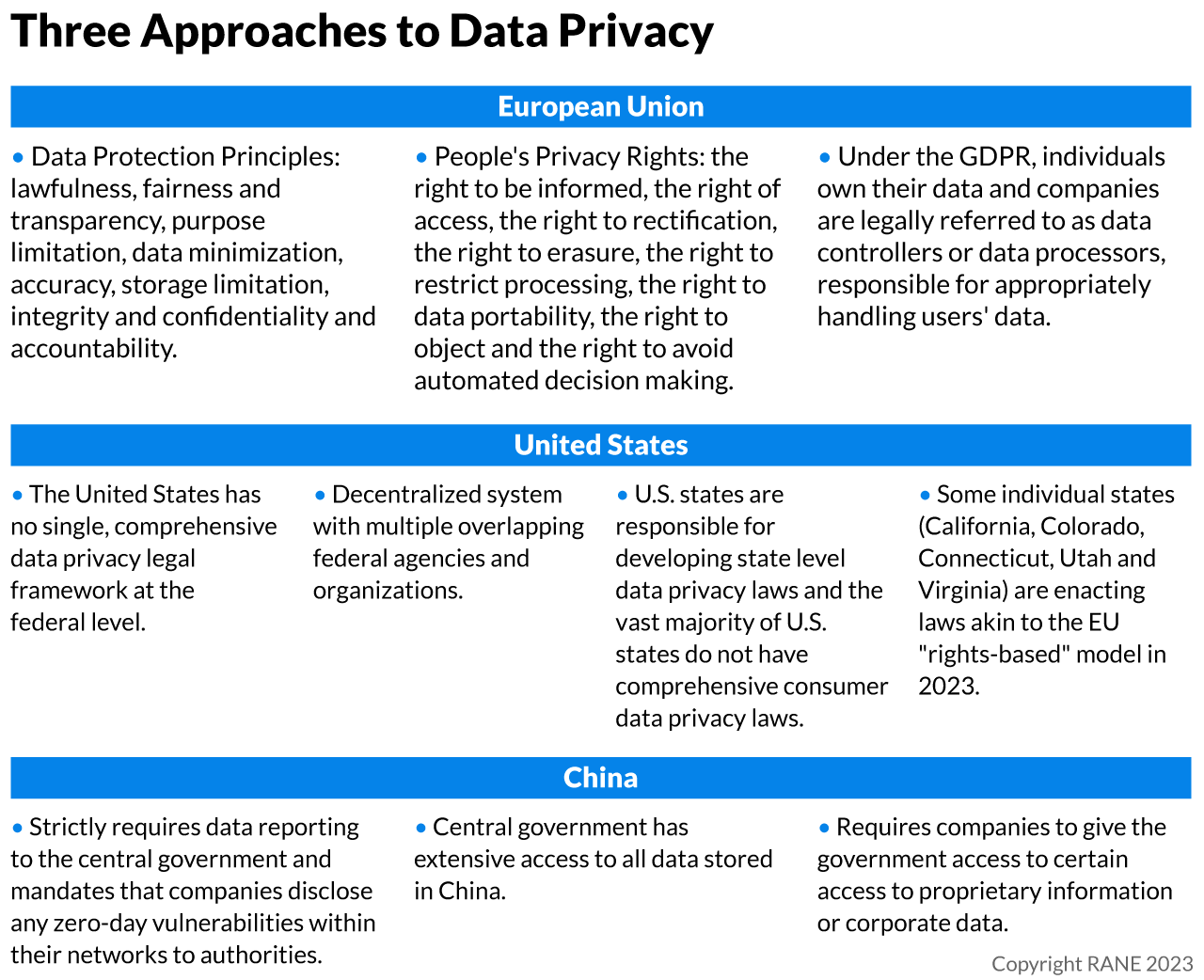

The European Union paved the way for a rights-based, comprehensive legal framework under the GDPR. The GDPR, which took effect in 2018, includes extensive and stringent requirements for how PII is defined and used, as well as how data is collected, stored and processed by domestic and foreign companies. Among the GDPR's provisions, the legislation upholds EU citizens' data rights, including that data is collected and processed for only its articulated use, limitations on how long clients' data can be stored and various requirements for reporting data breaches. Additionally, the GDPR requires companies to uphold EU citizens' data rights, including their right to be informed on how their data is being used, the right to access their data, the right of data portability, and the right to data rectification and erasure. The extensive compliance requirements that the GDPR enforces pose a number of legal and regulatory challenges for both Europe-based companies and foreign companies operating in European markets. Following Brexit, companies must now also navigate the added challenges of complying with emerging data privacy legislation in the United Kingdom that will likely differ from the GDPR in many ways.

- Morrissey first explains the primary differences in how Europe approaches data security compared to other locations like the United States. He notes that "In Europe, personal data is owned by the living individual. It's legally their data, so a company doesn't own it. The latter are called a data controller. They control it on behalf of the individual, and the GDPR defines specific legal obligations on how controllers process such data. So that's an important legal difference between the United States and EU." This foundational difference in how the European Union shapes data privacy and security protections and puts extensive responsibility on companies to uphold this framework, heightening their legal, financial and reputational risks for not complying with the GDPR's high standards.

- Failure to comply with the GDPR has resulted in many companies being fined or otherwise penalized, including many U.S. companies operating in Europe. For example, in 2022 alone, a number of companies were fined for noncompliance with various GDPR provisions. These included Meta, which was fined $405 million in September 2022 over how the company handled minors' data and Google, which was fined $57 million in December 2022 for failing to obtain users' consent before using their data for ad personalization purposes.

In addition to the GDPR's rigorous compliance requirements, the British decision to withdraw from the European Union has also complicated the overall European cyber landscape. Since the Brexit process first began, the United Kingdom has sought to enact new domestic legislation in a number of policy areas, including cyber and data regulations. Morrissey explains that Brexit has had a direct impact on any business operating between the United Kingdom and the Continent. He further explains that the United Kingdom is looking to replace the U.K. Data Protection Act of 2018, based on the GDPR, with new legislation in the coming year, which will likely create a number of digital divisions between London and Brussels.

- Morrissey highlights the special attention that Europe will likely be paying to the United Kingdom as it pursues new data protections in the coming year. He says, "I think there's a bigger concern about European data going into the U.K. into the future and making sure that there's some degree of alignment between these two pieces of legislation that allows data to continue to flow. He elaborates that "The EU is the U.K.'s biggest trading market, and vice versa. Something has to be figured out that allows business and commerce to continue to operate normally regarding digital data, which is more and more important every day in terms of its intrinsic value."

- Morrissey also outlines the challenges that companies will have to face in operating in both the European Union and the United Kingdom under different legislation. He states that "In reality for businesses, if you're an organization in the U.K. and you're trading into the European Union, you're going to have to comply with two pieces of legislation ... So it's going to create an operational headache for companies in the U.K. because they're going to have a double set of legislative standards that they will have to comply with." He explains further, "It's a very concerning problem for them because it's magnifying the complexity at a technical level where they have to segregate data potentially into silos based upon these geo-national restrictions which are coming down the line and that's a headache because it's both an additional operational and capital expenditure cost, as you are potentially duplicating technology across multiple geographical locations, in order to offset compliance risk."

The Fragmented U.S. Approach to Cyberspace

The United States contrasts with the broad and comprehensive EU legal framework with a more disjointed approach to its cyberspace. With no single federal data privacy regulation framework, the United States operates in a decentralized system with multiple overlapping federal agencies and organizations that oversee U.S. cyber practices, leaving states largely to decide data privacy regulations. While this fragmentation may be more attractive for some companies wishing to bypass strict regulation found in other jurisdictions like the European Union, it also poses risks because the lack of a federal data breach reporting requirement, for example, leaves businesses more vulnerable to losses if impacted by a cyberattack or if data is otherwise compromised. Though many states still do not have a comprehensive regulatory framework in place, this is changing, as several states are beginning to adopt data regulation practices modeled after the European Union.

- Although federal lawmakers have made some efforts to create a more explicit data privacy framework, each has subsequently fallen through. Without a single federal framework, U.S.-based companies have freer rein and an expanded scope for data collection practices. Limbago notes that, as a result of the growing nationalization of cyberspace, many companies are reshoring to the United States. Though partially due to the extended leeway many are granted in terms of regulation, she claims that it is mostly because of a greater stability and rule of law that provides a better business environment. Nonetheless, Limbago argues that much of the reason for a lack of a federal data framework is due to lobbying by U.S. companies, saying "that's probably why we don't have a data privacy law in the U.S. yet. Instead, we've got a very big patchwork. We have 54 different data breach notification laws because, you know, some core industries have helped limit our ability to have a data privacy law."

- Following in the footsteps of the EU GDPR, a handful of states have started enacting more stringent data protection laws using the EU "rights-based" model. In 2023, five states California, Colorado, Connecticut, Utah and Virginia — will begin enforcing these EU-like data privacy laws. Other states — including Michigan, New Jersey, Ohio and Pennsylvania — are also considering data privacy revisions, demonstrating a state-based trend to bolster cybersecurity protocol even in the absence of a federal mandate. While these changes will enhance cybersecurity regulations within these states, they will also pose more compliance risks to companies that will have to navigate data regulations from state to state.

U.S. cyberspace regulations are not only still being formed through various means, both at a federal and a state level, but also through international cooperation. Despite the absence of a single federal framework to govern data, the United States has participated in a great deal of international collaboration in this field. In fact, Limbago notes that although cross-data border flows are becoming more closed as a result of this growing trend toward the nationalization of cyberspace, in some ways they are also becoming more open — at least between certain jurisdictions. Indeed, agreements that allow for cross-border data flows may make it easier for companies based in the United States to straddle multiple cyberspheres, either to collaborate or work with others outside of this digital sphere or to expand their business scope beyond U.S. borders.

- In March 2022, U.S. President Joe Biden and European Commission President Ursula von der Leyen announced an EU-U.S. Data Privacy Framework to facilitate trans-Atlantic data flows. Since the European Union is a major trading partner for the United States, the framework, which is still under review in the European Union, is designed to provide a legal mechanism to transfer EU personal data to the United States that addresses privacy concerns and is compatible with EU law. Washington and Brussels frame the deal as benefiting companies in both geographic regions, allowing for a continued flow of data that enables trans-Atlantic trade amounting to more than $1 trillion annually.

- Additionally, Limbago highlights the "NAFTA 2.0" agreement that addresses not only cross-border physical trade, but also data flows across Canada, the United States and Mexico. In July 2020, the new U.S.-Mexico-Canada Agreement, colloquially known as NAFTA 2.0, entered force; it essentially serves as an updated version of the 1994 NAFTA. Among other provisions, the new agreement addresses technological advancements that have occurred since the original document was enacted, including clauses on digital trade rules and the promotion of cross-border data flows.

China and Digital Authoritarianism

While current U.S. data practices are relatively loose and decentralized, and the European Union is characterized by rigorous protections for its citizens, China represents a different type of stringency that moves away from individual data and privacy protections and more toward strict data reporting to the government, which has extensive reach into citizens' and companies' private data. This poses challenges for companies operating in China, as they balance the risks of keeping their data locally in a country known for its corporate espionage and intellectual property theft. Limbago explains that the motivations behind China's laws governing its cyberspace are to create a system that helps the government stay in power — one that gives it access to information and the ability to manipulate data and access as it sees fit.

- The cyber regime in China is characterized by strict reporting requirements to the ruling party and heavy government involvement in many industries. Within the country, Limbago notes that "digital authoritarianism also includes an aspect of domestic company favoritism. And so you also see companies starting to get pushed out of some markets because of that and so it kind of all goes hand in hand as far as a broader strategy … because many of the domestic companies in these countries are very much used to those kind of data policies and aren't necessarily as concerned because there's such a tight link between the estate and enterprise than government anyway." This highlights risks for companies moving into China, not only because of the stringency of the existing data privacy framework, but also because it is more difficult for foreign companies to succeed in a Chinese market that shows favoritism to domestic companies.

- Morrissey points out that Beijing's nationalization of cyberspace is not a new phenomenon that companies are dealing with when considering moving into China. He describes China as "the progenitor of this nationalization of data" and that "for the longest time now every U.S. corporation could write the book about what the experience is like going into China where you are segregated straight away. So everything you do in China stays in China. And that's the reality, the Great Firewall of China, as they call it ... Any businesses that are looking to move into the Chinese market inevitably are going to have to align with those national laws, both privacy and others."

- Limbago elaborates on this by explaining that historically, "for many countries ... that was almost a Faustian bargain. In exchange for having access to that market they understood there would be some sort of risk as far as access to data and so forth." Nonetheless, as cyberspaces continue to fragment and follow this trend of nationalization, "in many cases, [companies are] starting to realize that the balance of risk reward is starting to tilt away from the reward being as big as it was. And that's where we see so many companies either thinking about reshoring away from specifically China or already have started that process." For companies that are thinking about reshoring back to the United States, or just starting to think about operating in China, it is important to weigh priorities and implement the diversification suggested by Limbago.

When companies outside China that may not be accustomed to the culture of digital authoritarianism are thinking about operating within China's cyberspace, Limbago highlights that it is important to remember that any data that resides on China's sovereign territories must be stored there and adhere to its data laws, potentially allowing the government to access and manipulate data. She says that, in contrast with the EU's "rights-based" protections, in China, "instead of having data protected … the government can access that data under the claim of national security or really in many cases, just because they want to. But that's legal." As Limbago highlights, under digital authoritarianism, the government, under the auspices of national security, can formulate reasons for accessing data that would not be legal elsewhere, thereby creating higher data risks for companies operating in this cyberspace. This is important for companies to keep in mind when operating in China's cyberspace. If there is sensitive data being handled, it is crucial that companies weigh their options in terms of segmenting where certain data is located.

- Limbago elaborates on this point, calling for data segmentation and diversification, the process of separating and storing various data in different locations depending on the perceived risks of keeping data in different regions. When talking about concerns with China, she says, "Some aspect is just having the access to their data. Other aspects are really thinking about where your data centers are and making sure those are diversified and having to also focus on data segmentation for companies ... really making sure you do have the data segmentation becomes huge. So because you have to store the data in China and in various countries, making sure that as little is stored there as possible."

India and Emerging Powers

Outside of Europe, the United States and China, other countries have pursued a mix of data regulation frameworks in line with varying degrees of liberalization or authoritarianism. Some countries, such as India, have become increasingly attractive for foreign companies looking to expand into emerging markets with high commercial potential. Emerging powers like India are also becoming more attractive alternatives to other countries like China, which has historically attracted many Western companies looking for cheaper manufacturing and labor options. As geopolitical tensions have risen between China and the West, companies are seeking to minimize their political risk by investing in other countries, including India. While India is one of the fastest growing major economies in the world, it has also experienced significant political gridlock in its efforts to create a national cybersecurity framework. Partisanship and concerns from domestic and foreign companies have repeatedly prevented the Indian government from passing updated data privacy directives, creating an uncertain legal and regulatory environment for companies operating in India.

- Morrissey underscores the importance of India for Western businesses, stating "I don't know any company here in Europe or in the United States that does not have some commercial relationship and outsourcing arrangement with India. They're critically important in a lot of this because in many contexts Indian companies have significant access to data in the EU and North America."

- To mitigate compliance risks posed by operating in emerging powers' markets like India, Morrissey recommends that, "if you're using Indian companies to process your data, such as in technical support and other service-driven type roles, then it's going to come down, like it always is, to good practice in terms of cybersecurity. You need to really make sure you're extending your scope of cybersecurity best practice out to those partners in India so that they are aligned with your own standards which you have implemented, and that you have the necessary visibility on how they are using your data as well." By maintaining strong internal cybersecurity standards and by staying aware of India's regulatory developments, companies can still benefit from the economic opportunities that India offers while limiting their exposure to inadvertent compliance risks.

Best Practices for Companies

The current international cyber landscape and trends toward further nationalization in 2023 will pose significant challenges for companies. Aside from the specific actions companies can take in each of the aforementioned jurisdictions, there are a number of general best practices.

- Of paramount importance, Wunderlich emphasizes the need for companies to have a holistic and critical risk management plan when operating across different cyberspaces. According to him, companies first "need a clear-eyed enterprise risk management view of your data … Start from a risk management approach, understand what your data is and make sure you have an up-to-date and reasonably commercially viable security program." Specifically, Wunderlich emphasizes that companies need to think critically about how their data is protected in higher risk economic environments and developing markets, for example, by sharding or partitioning data into different secure databases. He suggests that companies ask themselves, "'Can I share my data in such a way that I have reasonable resilience and redundancy and still address the possibility that various jurisdictions that I operate in will require data localization that I have to demonstrate?'"

- Outside of internal cyber infrastructure, Wunderlich also emphasizes the importance of data minimization. He advises that companies make sure they "collect the minimum amount of data because data is opportunity and risk … You make money off of data but the more revenue you can generate off of data, the higher the risk that it's breached or misused." By minimizing data collection, companies can proactively mitigate any potential reputational or financial fallout in the case of a data breach, especially as such cyber breach incidents continue to evolve as a primary cyber threat. In the same vein, companies can also maintain clear data retention and destruction policies to ensure data is being properly handled internally and is at the least risk of being directly or indirectly compromised in a data breach.

- Limbago puts particular emphasis on data diversification and segmentation, specifically, separating aspects of your data and minimizing which locations you keep your proprietary data locally stored. As Limbago highlights, "having all of your eggs and basket turns out to be quite risky." When talking about China, she notes that "it doesn't have to be all or nothing. You can still keep some footprint in China, but it's more than diversification." Though China is a clear example of why companies may need to segment and diversify their data, this recommendation can be applied more generally for companies operating in multiple cyber realms — not just in China.

- Additionally, as Morrissey previously mentioned specifically in the context of India, it is broadly in companies' best interests to expand their scope of cybersecurity best practices, not only for their own cyber protections, but also to ensure their foreign partners are aligned with their company's internal standards. Maintaining a common framework across international partnerships, in addition to staying abreast of the local regulatory environment, can also help companies mitigate the risks of operating in a multipolar landscape. For example, for companies operating within the United States, it will be useful for compliance teams to ensure they are aware of changing U.S. state and federal privacy and security legislation, in order to anticipate any changes that may impact their operations. Increasingly, compliance plays an important role in informing capital and operational investment, in particular for technology. Morrissey notes that digital advertising is an excellent example of this, where changes in global privacy law have created a major need for institutional change at the technical level for that sector.

In spite of the myriad and growing risks within the cyber realm, Wunderlich also encourages companies to nevertheless investigate ways to capitalize upon the increasingly multipolar international system. He urges corporate leaders to ask themselves, "If we're coming out of a period of globalization and we're getting into a multipolar commercial world, not just a multipolar geopolitical world, how do you position yourself to take advantage of that? What's the business model that allows you to take advantage of that? How can you pivot and take advantage of where you think things are going?" To do so, Wunderlich references the importance of having a clear-eyed enterprise risk management view to enable a company to make an informed, analytical decision about the costs and benefits of operating in foreign markets.

From Tax Credits to Subsidies and Green Technology, The New Protectionism

The United States and Europe are embracing climate-focused protectionism for political, economic and climate-related reasons, and consequently upending aspects of their free trade environment that have existed for decades as they increase trans-Atlantic trade barriers. The U.S. Inflation Reduction Act of 2022 included some of Washington's most significant protectionist measures for its industrial sector in recent years, triggering tension with its European allies due to stringent requirements for electric vehicles qualifying for tax credits. The EU is now preparing to introduce its own subsidies in response. To discuss what is driving their respective policies and the implications for multinational corporations, RANE spoke to Jason Cherish, Founder of Atlas|Bear; Marc A. Ross, Chief Communications Strategist of Caracal; and Robert Ludke, Founder of Ludke Consulting.

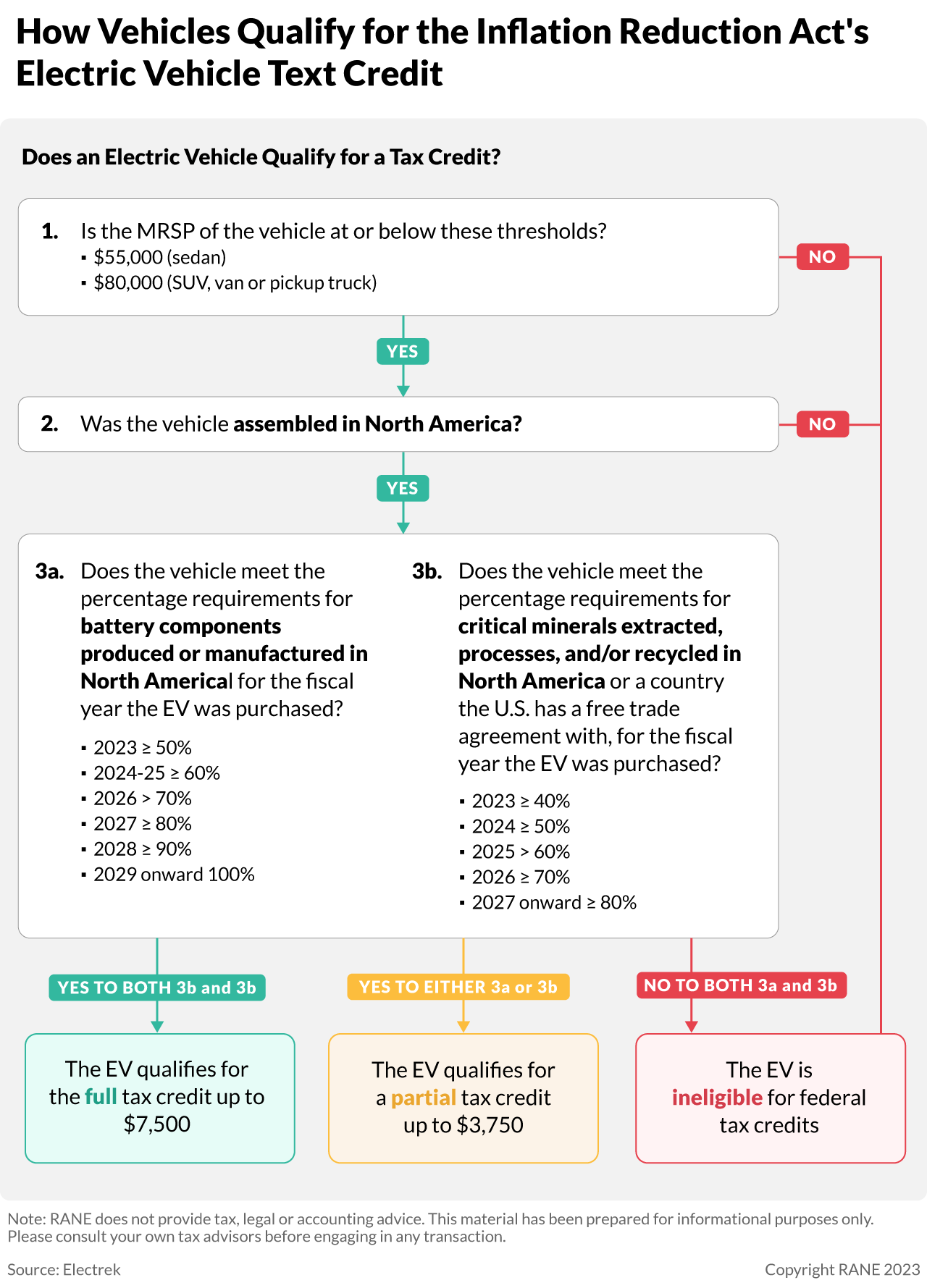

The Inflation Reduction Act Aims to Boost U.S. Jobs

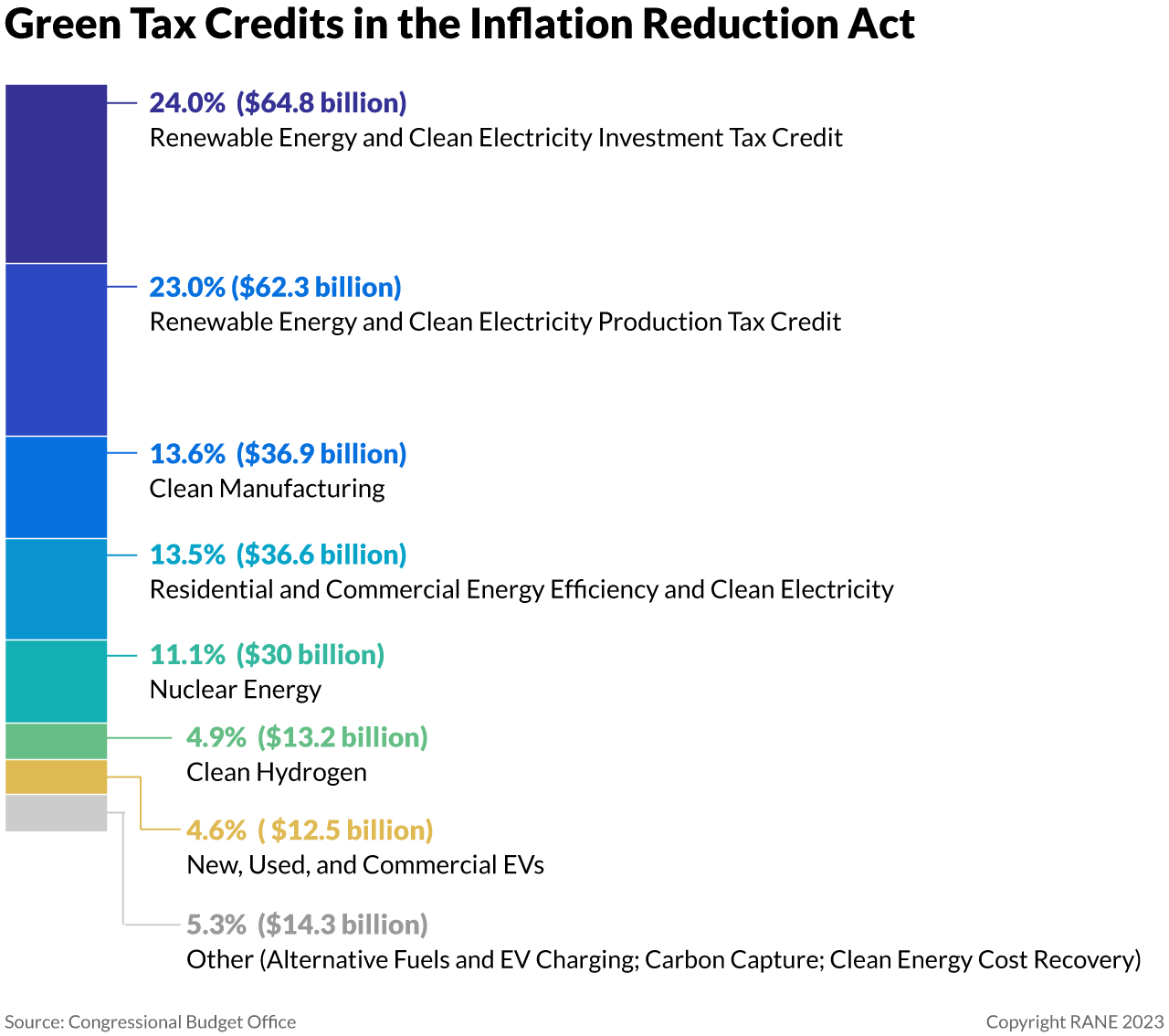

The Inflation Reduction Act (IRA), signed into law on Aug. 15, 2022, includes a raft of support measures for the U.S. green sector and electric vehicles (EVs), with total financial assistance reaching an estimated $396 billion. Although the IRA includes a number of corporate and consumer tax credits beyond the automotive sector, the clean vehicle tax credit has proven the most controversial due to the fact that some of its provisions, critics argue, discriminate against foreign companies and inhibit competition in favor of supporting the U.S. industrial base. In order to be eligible for a newly purchased EV to qualify for a full $7,500 tax credit, the vehicle must have its final assembly occur in North America, with a certain percentage, from less than 50% in 2023 to 100% in 2029 and beyond, of its battery components being manufactured in North America and a certain percentage, increasing from 40% in 2024 to 80% in 2026, of its critical minerals processed in North America or a country with which the United States enjoys a free trade agreement (FTA). Critics argue that the first two conditions – the location of final assembly and the percentage of battery components being manufactured in North America, provisions designed to support U.S. jobs – discriminate against EU, Japanese and South Korean automakers that have not shifted their final assembly to the United States or rely on battery and battery component manufacturers based outside of North America.