An image depicting the global economy.

With international negotiations stalled, many governments are choosing to unilaterally implement digital services taxes (DSTs). The United States — which is home to the majority of tech giants that would be subject to such taxes, including Amazon, Apple and Google — is using the threat of tariffs to both limit the global expansion of DSTs and push international negotiations toward the proposed reforms it backs. But with so many countries against Washington's preferred outcome, which critics say would allow U.S. tech companies to opt out of tax obligations in international markets, the risk of negotiations failing to reach an agreement this year is high, as is the risk of the United States implementing tariffs on its growing number of trade partners implementing DSTs.

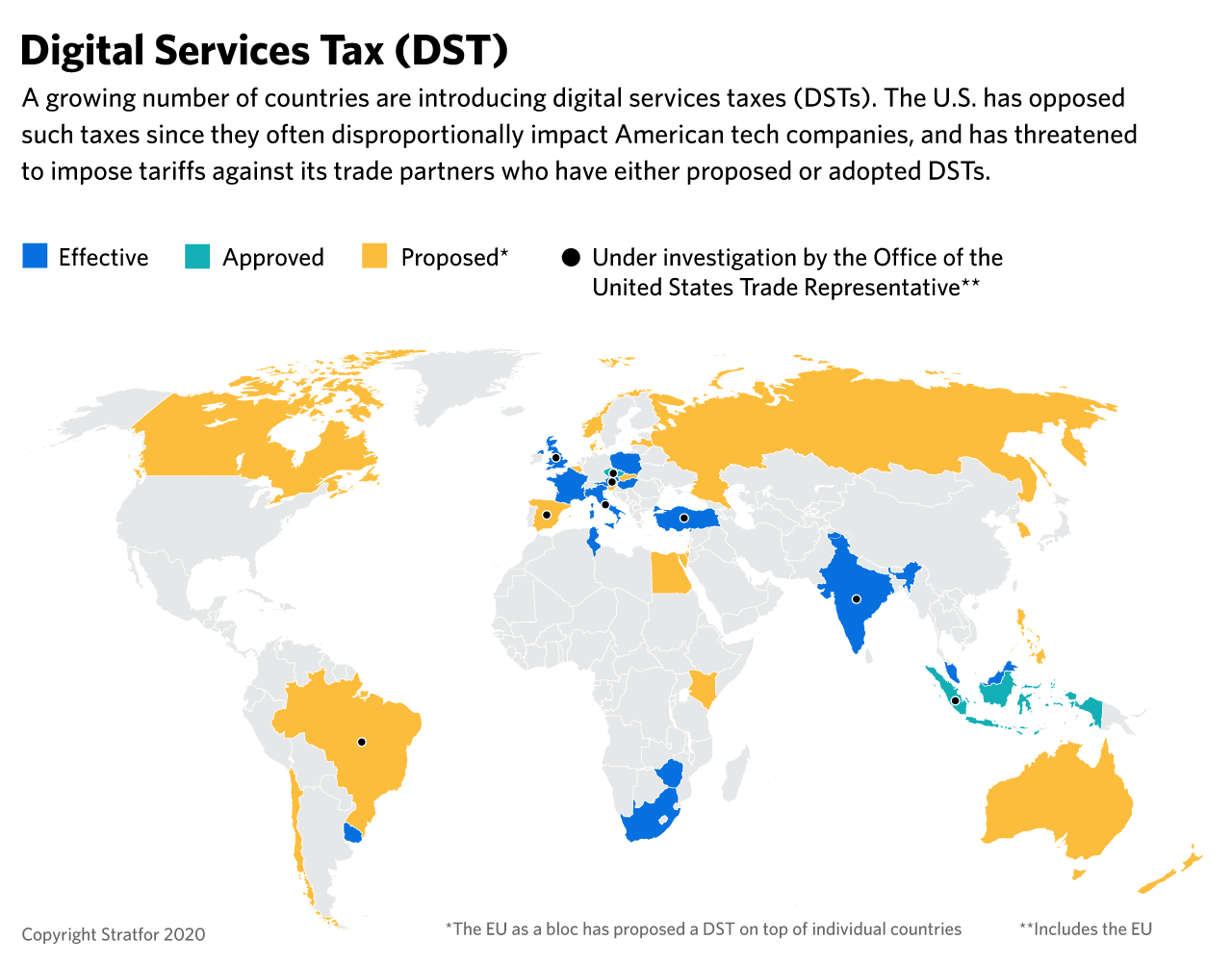

Washington vs. the World

On June 2, the administration of U.S. President Donald Trump announced it was launching investigations into the European Union and nine countries that have implemented or are considering implementing DSTs to determine whether or not they unfairly target U.S. tech companies.

- The targeted countries include Austria, Brazil, the Czech Republic, India, Indonesia, Italy, Spain, Turkey and the United Kingdom.

- The investigations will be conducted under Section 301 of the Trade Act of 1974, which gives the White House the ability to impose significant tariffs on imported goods (the tariffs deployed by the Trump administration in its trade war with China are also reliant on Section 301).

The U.S. investigations are open-ended and may take months to complete, but will almost certainly find that each national DST treats American tech companies unfairly. The vast majority of the DSTs that are being introduced only target internet and digital services companies with a large global and domestic revenue. France’s new DST, for example, only applies to companies that generate at least 750 million euro ($850 million) and 25 million euro ($28.3 million) a year in global revenue. Washington’s 2019 investigation into the French tax already found that it unfairly targeted the U.S. companies, noting that of 27 companies that would be subject to France’s DST, 17 were American while just one was French. Many of the other countries introducing DSTs are using revenue benchmarks similar to France, meaning their taxes will disproportionately target U.S. tech companies as well, and will thus similarly risk drawing Trump’s ire.

Over the last decade, however, most countries have realized that existing global norms around corporate taxes are inadequate in taxing the digital economy and allocating profits between different jurisdictions. Today's international tax system is rooted in policies established long before the existence of a "digital" economy. It focuses heavily on a company's physical presence in order to allocate profit margins between different jurisdictions for tax purposes. But while it works well for physical goods, this view is outdated for DST proponents because many digital companies create "value" from the data that they collect from their online user base. Thus, their user base itself plays a role in adding value to the corporation and therefore the jurisdiction(s) where the user base is located should have the ability to tax that the value added by their citizens.

The different views on how to tax tech companies have created a sharp divide between the United States — which is home to the majority of the world's tech giants — and the rest of the world. Amid the rising global political backlash against major tech companies due to issues such as privacy, it should be no surprise that most countries without large tech companies of their own have supported adopting a DST, as it increases their tax base. Equally, it should be no surprise that the United States has taken a more narrow view on the matter in an effort to protect both U.S. companies from unilateral taxes overseas, as well as the size of the U.S. government’s tax base through limiting foreign tax credits. After President Emmanual Macron signed France’s DST into law in 2019, U.S. President Donald Trump famously tweeted that, "France just put a digital tax on our great American technology companies” and that if “anybody taxes [those companies], it should be their home country, the [United States].”

Fighting Taxes With Tariffs

The United States hopes that the threat of tariffs will force countries to wait until international negotiations before moving forward with unilateral DSTs. France and other countries have all argued that their national DSTs are meant to be temporary and will be repealed as soon as an international agreement is reached. But the protracted negotiations to reach such an agreement means that these DSTs may remain in place for several years — thus resulting in higher taxes for U.S. companies in the meantime, as well as an inefficient system where U.S. companies are taxed multiple times for the same activities. The United States has also expressed concerns that these national digital taxes may still become permanent regardless of whether an international agreement is reached, since many countries’ DSTs lack sunset clauses that would allow them to expire.

The split between the United States and virtually every other country over how to tax the digital economy — and in particular, how to handle the allocation of profits — means reaching a new global consensus on the matter by the end of the year is highly unlikely. Negotiations are being led by the Group of 20 (G-20) and the Organization for Economic Cooperation and Development (OECD)’s 137-member Inclusive Framework on Base Erosion and Profit Shifting (BEPS). The Inclusive Framework aims to meet one final time in October before sending over a proposed framework for approval at this year’s G-20 leaders summit in November.

Current negotiations are centered around two pillars:

- Pillar 1: A unified global approach on defining a global reallocation of digital profits and what types of activities are subject to such taxes.

- Pillar 2: A global minimum tax for digital companies.

To protect U.S. companies from having their revenue disproportionately targeted, the United States has proposed that multinational companies opt-in, on a global basis, to be subject to Pillar 1. Opponents of Washington’s approach, however, have argued that if given the choice, most companies would simply avoid taxes. But to that end, the United States has argued that companies would still, in fact, opt-in to Pillar 1 because it gives them tax certainty as opposed to the uncertainty that the current system has created.

While the approval of both pillars is unlikely, it is entirely possible that the Inclusive Framework and the G-20 are able to make limited progress by the end of the year. Pillar 2 is far less controversial to the United States conceptually, as it is similar to tax reforms for global multinationals that the United States introduced in its 2017 tax reform to limit tax avoidance overseas. But international negotiations thus far have focused more on Pillar 1 and the proposals for Pillar 2 are less concrete. To ensure companies can continue to implement DSTs without prompting the United States to impose tariffs, the Inclusive Framework may back a narrow proposal for Pillar 1 that largely leaves the details unresolved and up for continued negotiations in order to have something G-20 members can sign in November. But countries will likely continue to move forward with unilateral DSTs, regardless of whether or not progress is made on Pillar 1 in the next six months. France, for example, has already announced that it will move forward with implementing its DST as planned at the end of 2020 if an international agreement is not reached.

The Battle Continues

If an international agreement over Pillar 1 is delayed and talks continue into 2021, and if Trump is re-elected in November, the United States will likely move forward with its threatened tariffs. Countries that agree to delay implementing their DSTs or the tax payments tech companies have to make beyond 2021 may be spared of the Trump administration’s economic wrath. But the willingness of countries to make such a compromise in order to avoid U.S. tariffs will likely vary.

If former Vice President and Democratic candidate Joe Biden wins the U.S. presidential election, it would reduce the immediate threat of tariffs, though the impasse in international negotiations would likely still continue. Trump would be far more willing to impose retaliatory tariffs against DSTs than Biden. Given his campaign pledge to reassert the United States’ status as the overseer of international order, Biden may also be more open to compromise. At the end of the day, however, a Biden administration would still steek to protect U.S. interests in international tax negotiations. But instead of deploying tariffs, he’s more likely to challenge national DSTs that have already been implemented through WTO and other dispute mechanisms.