OPEC's logo is seen at the organization's headquarters on Sept. 26, 2019. The killing of Qassem Soleimani didn't especially hit oil prices, but unresolved U.S.-Iranian tensions could.

The recent flare-up in the Middle East between the United States and Iran highlights a structural shift in how the oil market reacts to political risks. The market has shifted to a baseline with a modestly bearish outlook and a reluctance to price in risk in the manner it previously has. But even so, the potential exists for a massive price move in the less probable (but still very plausible) event of a major and lasting disruption.

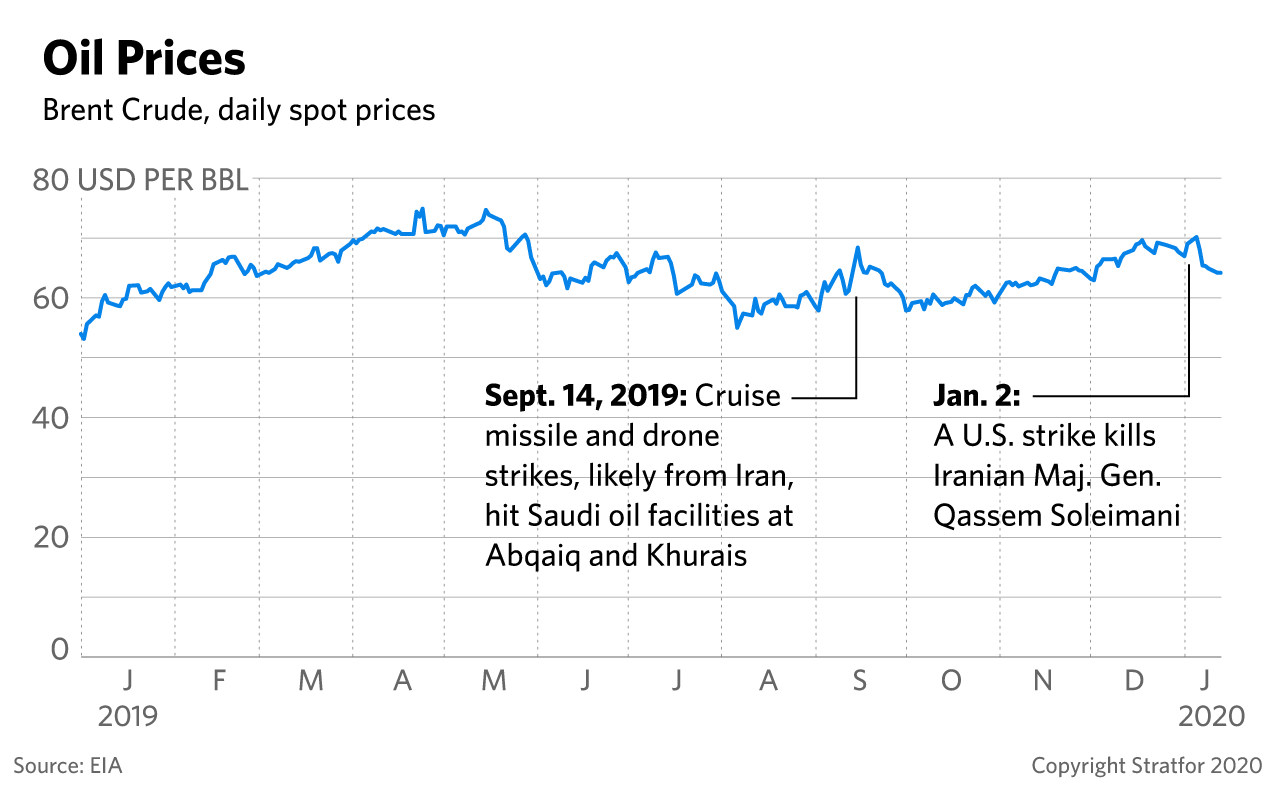

Crude oil is now trading below its price immediately before the Jan. 3 U.S. strike on Islamic Revolutionary Guard Corps Maj. Gen. Qassem Soleimani, with Brent crude oil prices now standing at around $64 per barrel — 9 percent below its high during the elevated Iran-U.S. tensions that followed Soleimani's killing. Even before the Jan. 8 Iranian retaliation against Iraqi military bases hosting U.S. forces, Brent crude oil had begun to pull back from its high of slightly above $70 per barrel due to Iran's signals that it would focus its retaliation on U.S. military targets rather than regional oil infrastructure. The recent price moves once more validate our view that it is difficult for crude oil to maintain a risk premium, or pricing higher than physical market fundamentals would otherwise justify, without an actual loss of supply.

Much of the media narrative has wrongly described the price reaction as stemming from complacency in the market about geopolitical risk. But while perceptions of immediate risk have indeed ebbed, they have not receded to normal, noncrisis levels. The short duration of the spike reflected a surge in producer hedging by companies eager to lock in modest profits and ensure their ability to make debt payments amid what, for them, are damagingly low oil prices.

This is not to say that future flare-ups between the United States and Iran will not raise oil prices. They will, but probably less so than in the past now that there have been two cycles — the attacks on the critical Saudi oil infrastructure at Abqaiq and Khurais, as well as the Soleimani killing — that quickly receded. This is a major structural change in how the oil market works. Speculative traders are likely to adjust their behavior based on this new reality to avoid losses. The new dynamic would not, however, reduce the impact of an actual, large-scale disruption in oil production or transportation that lacked a clear timeframe for resolution.

OPEC+ Struggles to Cut Production

With prices having tapered off in the absence of a disruption, fundamentals like the U.S.-China trade deal and supply cuts by OPEC and other producers — who are collaborating as OPEC+ — will largely determine where the market goes. Much of the rise in prices since early last month has been driven by the conclusion of a phase one trade agreement between China and the United States, which has reduced market fears of a sharp economic slowdown in 2020 and the concomitant impact on oil demand. It has also been driven by the surprise deal on Dec. 6, 2019, in which OPEC+ agreed to an additional 500,000 barrels per day in headline production cuts.

It appears OPEC+ will fall short of this goal. Russia will take advantage of new definitions surrounding condensates to avoid incremental production cuts, while the two other producers that have fallen short, Iraq and Nigeria, are still not in compliance. Iraq did manage a 60,000 bpd reduction in supply last month, but this was partially due to protests that impacted an oil field that produces 30,000 bpd, and Baghdad remains unlikely to fully implement its quota of the cut. Nigeria, meanwhile, recently claimed that it was already in compliance with the new target as of December 2019 despite data from secondary sources showing it was producing well above the agreed-upon target. So while formal obligations to make cuts did not kick in until January 2020, nothing indicates that full compliance from OPEC+ members is likely. Recent speculation that the next OPEC+ ministerial meeting could be postponed from March until June strengthens this forecast, as a delay would postpone any naming and shaming of producers who fail to meet their targets. By contrast, the Saudis, as expected, have overperformed on their cuts, with Saudi production currently standing at 9.744 million bpd, according to Saudi Energy Minister Prince Abdelaziz bin Salman.

With growth in U.S. supply surging to 12.9 million bpd (even if it is expected to slow sharply in 2020) and the early startup of the Johan Sverdrup offshore field in Norway, it is now becoming clearer that inventories will build in the first half of 2020 regardless of genuine reductions by OPEC+. Combined with the structural change in how the market reacts to unrealized disruption risks, this is likely to lead to a slight decrease in prices, though by no means a collapse.

Oil Prices in a Year of Potential Escalation With Iran

While the immediate crisis following the Soleimani strike has passed, no sharp reduction in overall risks related to Iran has occurred. As we have written, 2020 could be a year of escalation with Tehran.

Widely expected moves by Iran and its regional proxies could touch off an uncontrolled escalation. Iran also continues to accelerate its production of low-enriched uranium, and as its nuclear "breakout time," or the time it needs to produce enough highly enriched uranium for a nuclear weapon, grows shorter, U.S. and Israeli policymakers may face a critical decision as to how to stop it by this summer — something that could even involve military strikes. Meanwhile, a tweet from U.S. President Donald Trump on Jan. 11 indicating indifference to negotiations with Iran marked a significant tone shift, possibly suggesting he expects sanctions pressure may produce regime change before then, although that it is not particularly likely.

Meanwhile, in a new and worrying development for oil markets, The New York Times reported Jan. 11 that Trump approved cyberattacks to damage and disable Iranian oil infrastructure in the event that Iran struck back more forcefully and inflicted U.S. casualties in response to Soleimani's killing. That didn't happen, but if it does in the future, Iran could overcome its apparent reluctance to strike Saudi or Emirati oil infrastructure in response.