According to the bureau's figures, the August influx of cash did not prompt Chinese companies to increase their investments in kind. Instead, growth in investment remained sluggish; private sector investment, which accounts for more than 60 percent of the national total, rose just 2.1 percent year-on-year in August. Meanwhile, investment in real estate construction increased by only 5.4 percent. (By comparison, these figures seldom dipped below 20 percent in the 2000s.)

On their own, these numbers are not surprising. Though Chinese lending and financing were markedly higher in August than in July, they were still well within the government's normal range. Moreover, August figures were far more modest than those seen in June, March and January, when financing topped 3.5 trillion yuan. Investment growth likewise has been steadily declining since late 2013 as China's property sector ground to a halt. Signs of the industry's recovery, however fleeting, have only begun to emerge this year.

Looser Lending Rules

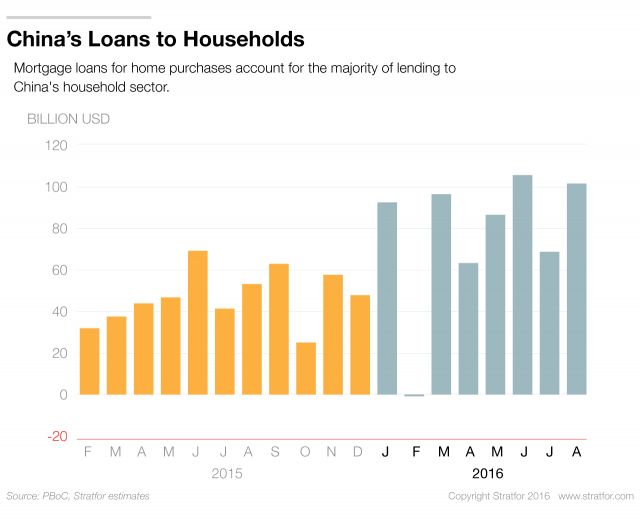

Beneath this unexceptional surface, however, noteworthy developments are underway. Of the 948.7 billion yuan in loans issued by banks in August, 71 percent (worth 675.5 billion yuan) were in the form of household loans, the majority of which were put toward home mortgages. This represents a hike of nearly 50 percent compared with July. If the share of Chinese bank loans for mortgages continues to rise, it will signal a radical departure from the way China's housing sector has historically been financed.

In the past, the bulk of credit in the housing sector was granted to developers seeking investment for their construction activities; most Chinese households funded home purchases with personal and family savings rather than loans. Until recently, this practice was reinforced by relatively tight down payment restrictions in most major Chinese cities. But over the past two years, central and local governments have begun to lower the minimum down payments required of first-time homebuyers. As a result, Chinese homeowners are now beginning to rely more and more on loans to purchase houses. Should this dependence continue to grow in the years ahead, China could become more vulnerable to the type of financial crisis that hit the United States in 2007-2008, when a housing bubble popped and left many U.S. citizens weighed down by loans worth more than their homes. Alternatively, if the Chinese economy continues to slow, and if corporate bankruptcies give way to higher unemployment, Chinese citizens could find themselves out of jobs and unable to pay back their housing loans.

Companies, meanwhile, may be getting easier access to credit. The issuance of bankers acceptances — an informal lending tool in which banks endorse bills issued by companies that the firms then use as payment to third parties — has been sharply declining over the past two years as Beijing cracks down on shadow lending. But in August, the value of bankers acceptances dropped by only 38 billion yuan, well below the 512 billion-yuan dip seen in July (not to mention the cutbacks that took place from April to June).

Of course, lending is often volatile in China, and sharp swings from month to month in one form of financing or another are not uncommon, especially in the country's notoriously erratic shadow banking sector. Nevertheless, the slowing fall of bankers acceptances could indicate that Beijing is relaxing some of its restrictions on informal lending in an effort to boost certain sectors of the economy. Anecdotal evidence indicates that bankers acceptances are particularly popular among Chinese manufacturers, many of which are private enterprises.

Financing Old Debts Over New Projects

Despite the new money flowing into corporate coffers, investment — which fuels the Chinese economy and is often a primary destination of Chinese financing — has continued to grow at a sluggish pace. Coupled with the sharp decline in new loan maturity periods over the past few years, this suggests that Chinese companies rely on credit less to buoy investment than they do to pay off old debts. This explains, at least in part, why Beijing is currently trying to boost corporate debt-to-equity swaps, which are intended to ease companies' financial burdens by converting outstanding debt to equity, thereby lowering their debt-servicing costs.

Together, the lending hike and flagging investment growth herald substantial changes ahead for China's financial system. Some, if properly managed, could be welcome: Corporate debt swap programs and the expansion of legal infrastructure to handle bankruptcies are necessary steps in China's path toward a market-oriented model of economic growth. At the same time, though, rising homeowner loans could pose a new and dangerous risk — one that Beijing will struggle to manage effectively.