Portugal was supposed to have presented its budget to the European Union in late 2015, but inconclusive general elections in October and a traumatic process to form a government forced Lisbon to request a postponement. Portugal sent a draft budget to the EU Commission in January, but officials in Brussels warned that the proposed plan to reduce Portugal's structural deficit was inadequate. Lisbon intended a reduction of around 0.2 percent of gross domestic product in 2016, but the Commission wanted a drop of at least 0.6 percent. The Commission also argues that the Portuguese budget is based on an overly optimistic forecast of the country's GDP growth for this year.

These additional demands are creating problems for the administration in Lisbon. Costa's Socialist Party leads a minority government that relies on parliamentary support from three small left-wing parties (the Communist Party, the Greens and the Left Bloc) to pass legislation. The Socialists have agreements with each party individually, forcing the government to constantly negotiate every decision with multiple partners, each with their own priorities.

The Socialists campaigned on reversing some of the austerity measures that were introduced by the previous conservative administration. Moreover, the party promised its allies that they would raise the country's monthly minimum wage, reduce the income tax and introduce benefits for poor households. But Brussels is forcing Costa to look for ways to reduce Portugal's deficit without losing popular support and without irritating the disparate group of lawmakers that back his government.

For Lisbon, another round of painful spending cuts is not an option. Should it, for example, announce new cuts in public-sector salaries, the government's allies would withdraw their support, and it would fall. Lisbon could instead focus on increasing levies such as the value-added tax, but this would go against the Socialists' plan to generate economic growth by boosting domestic consumption. As a result, the Portuguese government will try an intermediate option: mild spending cuts and higher taxes on activities such as banking operations. Portuguese media reported that Lisbon is also considering new fuel and car taxes.

The Socialists will present a budget to parliament on Feb. 5, hoping to receive support first from lawmakers and then from the EU Commission. Also on Feb. 5, Costa will meet German Chancellor Angela Merkel in Berlin. While the official reason of the meeting is the refugee crisis, Costa will probably ask for Merkel's support in his negotiations with Brussels. Italian Prime Minister Matteo Renzi also met with Merkel in the context of his negotiations with Brussels on Jan. 29. Like Portugal, Italy is asking for flexibility with its structural deficit. It is notable that both Portugal and Italy have sought Germany's assistance — during the height of the financial crisis, Germany was the strongest defender of fiscal consolidation measures. But now that Germany is having its own domestic problems because of the immigration crisis, countries in Southern Europe are betting that Germany wants to avoid new conflicts in the eurozone, becoming more open to relaxing EU budgetary rules.

A Fragile Recovery

After years of recession and high unemployment, the Portuguese economy started growing in 2014, and it is projected to continue expanding in the next two years. Unemployment is also around 12 percent, considerably lower than the 18 percent peak it reached in early 2013. Specifically, domestic reforms that were implemented at the beginning of the crisis, low oil prices and the bond-purchasing program by the European Central Bank have supported this growth.

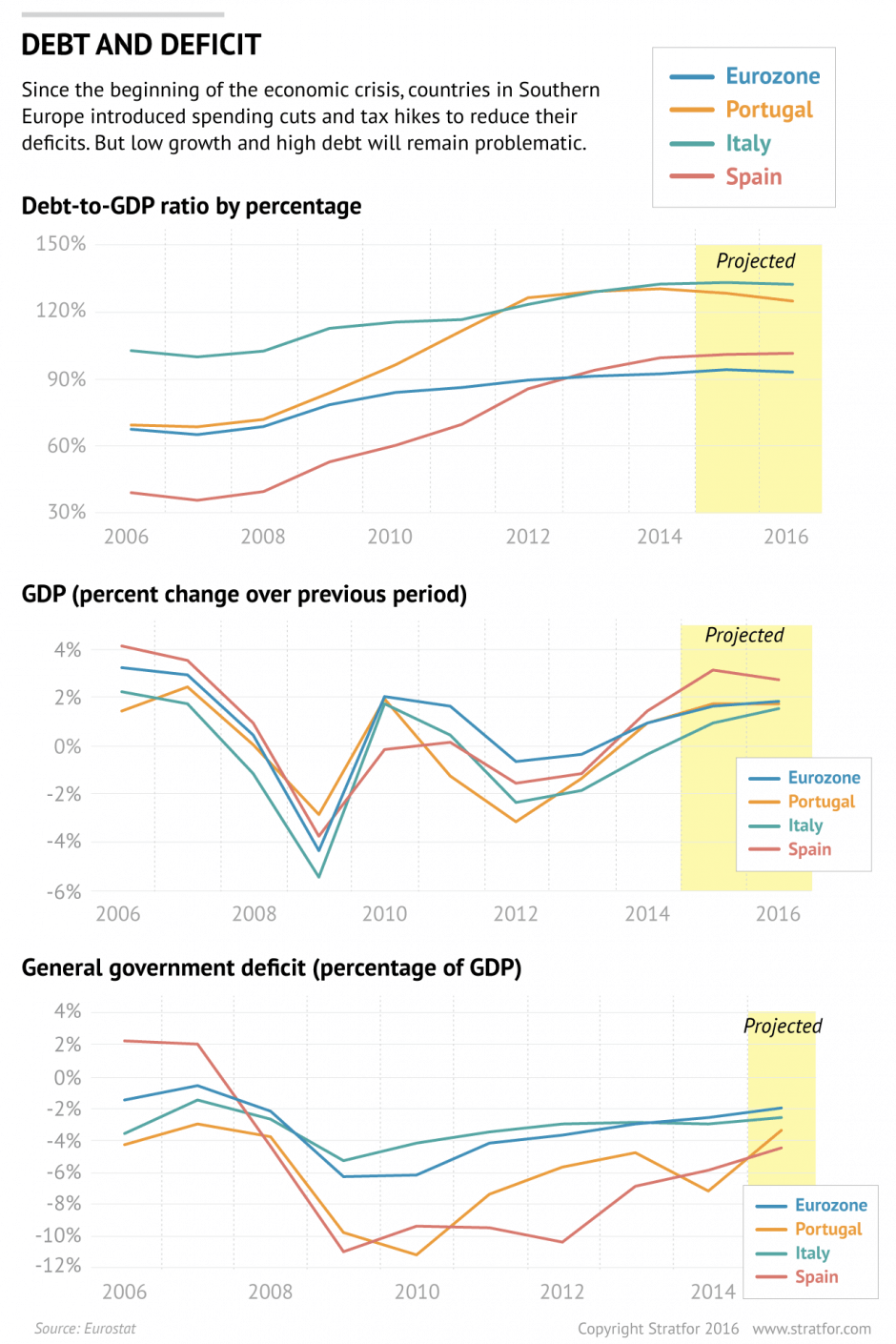

However, Portugal's recovery is still fragile. To finance its plans to reverse austerity measures, Lisbon will have to issue more debt. Higher bond yields, which already have risen recently, could make the process more expensive for Lisbon. According to Portugal's Technical Unit for Budget Support, the slowdown in fiscal consolidation will also require taking on a further 11 billion euros ($12.2 billion) in debt by 2019. Portugal's debt is already at 130 percent of GDP, the third-highest proportion in the eurozone after Greece and Italy.

If corporate and household debt is included, Portugal has more debt in total than any other eurozone country. When an economy and government are stable, this is not a problem. But in Portugal's case, lingering friction with Brussels and domestic political instability could be detrimental. In addition, the country would need to grow by at least 3 percent for an extended period to reduce its debt burden. Yet the EU Commission expects Portugal to grow by only half that figure in the next two years. The main danger for Portugal is that foreign holders of Portuguese debt could decide to simply write it off and start selling en masse. A government that backtracks on economic reforms or starts to fracture politically could trigger that.

Portugal's banking problems are not completely finished, either. Only weeks after taking over the government, the Socialists had to rescue Banco Internacional de Funchal (Banif) with state funds, growing Portugal's deficit. In late December, the Portuguese central bank also had to cover a 1.4 billion-euro shortfall at Novo Banco, an institution that was created after the collapse of Banco Espirito Santo in 2014.

Of course, the EU Commission has been flexible on fiscal targets in the past, and officials recently suggested they would seek a compromise with Italy. However, the Commission is also interested in preventing an avalanche of demands for budget flexibility from other eurozone countries, such as Spain. Political parties are still struggling to form a coalition in Madrid, but once there is a government in place, it will probably join Portugal and Italy in the request to ease austerity. Brussels would like to avoid this, explaining its toughness with Lisbon. Lisbon will probably reach a compromise with Brussels, and punitive measures are unlikely, but Costa will have to make some difficult decisions before a final agreement is reached. Such negotiations could hurt the Portuguese government and cause uncertainty to linger.

During the height of the eurozone crisis, countries in the Iberian Peninsula had fragile economies but relatively stable governments. In the coming months, it will be political volatility that directly threatens Portugal's financial security.