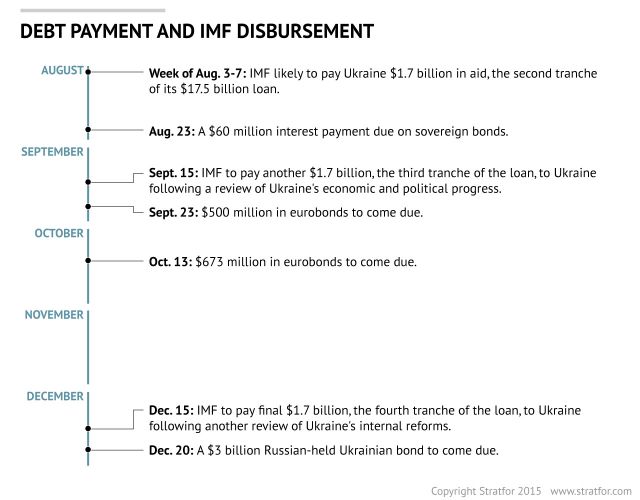

The Ukrainian government will probably use its next tranche of aid to replenish the National Bank's international reserves as well as to make payments for natural gas debts. In the meantime, the country is making considerable progress in the eyes of the international community. IMF Director Christine Lagarde recently praised Ukraine for "aggressively undertaking long-needed reforms," even as the IMF board reviews the next bailout dispersal.

There has also been progress in ongoing discussions between the Ukrainian government and its main bondholders on restructuring the country's debt. On Aug. 4, Ukraine's Finance Ministry sent a proposal to the ad hoc creditor committee — which includes the country's main bondholders of Franklin Templeton Investments, T. Rowe Price, TCW Group and BTG Pactual Europe and collectively holds about $9 billion of Ukraine's outstanding debt — for a meeting on Aug. 6 in London to discuss details on restructuring the country's sovereign and sovereign guaranteed debt.

The negotiations have until now focused on haircuts to Ukraine's debt, and Stratfor has received indications that a compromise agreement could entail a debt haircut between 10-25 percent for Ukraine, to be balanced with GDP-linked bonds to make the deal more acceptable to creditors. If the haircut is higher, there could be a coupon over a 3.5-year period and vice versa. The Ukrainian Finance Ministry has set a deadline for the end of the week to reach a preliminary deal, as it could take weeks to prepare and finalize a deal before a large maturity payment is due in late September. Therefore, the Aug. 6 meeting could be a decisive one.

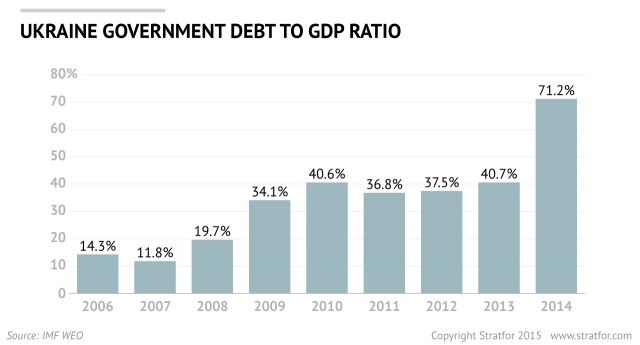

A debt restructuring agreement would offer significant relief for a cash-strapped Ukraine still struggling to turn its economy around and still embroiled in a costly conflict in its eastern territories. However, a deal would not solve one of Ukraine's primary economic challenges: natural gas pricing negotiations with Russia. Nor will it be enough to help Ukraine fulfill its $3 billion debt payment to Russia, which is due at the end of December. Current debt talks do not address these Russian-held Ukrainian bonds, and Moscow insists they should not be included in Ukraine's sovereign restructuring on the grounds that the bonds are direct state aid.

However, there are legal ambiguities surrounding the status of Russia's loan, and if Ukraine refuses to repay the loan at the time scheduled, the dispute could turn into a drawn-out legal battle. Therefore Ukraine is likely to avoid default in the short term, but it will nevertheless have difficult financial problems to address with Russia just as the conflict in eastern Ukraine shows no current signs of dissipating.