Forecast

- The Irish economy will see strong growth in 2015 and 2016, but private and public debt will remain problematic.

- After years of spending cuts and tax hikes, the current and future Irish governments will be under pressure to increase salaries in the public sector and to restore spending in the country's welfare system.

- Dublin will support the United Kingdom's push for reform in the European Union, hoping to preserve London's membership in the Continental bloc.

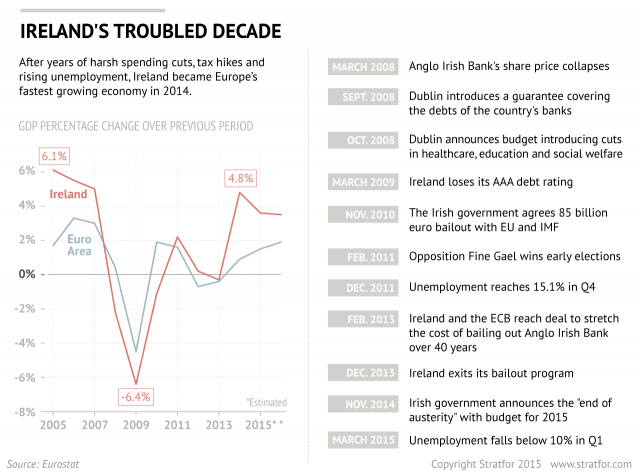

Ireland has not featured prominently in the news since the collapse of its banking and real estate sectors in the late 2000s, but now it is making headlines and for positive reasons. After spending most of the past decade in a deep financial crisis, with early signs of recovery in 2014, the Irish economy is now growing again in earnest. But even as unemployment drops and Ireland's prospects for growth improve, its large public and private debt could still threaten the country's economic future, and its recovery has yet to be equally felt across the country. Dublin will also have to deal with threats to European unity in the coming months and years, since a Greek or British exit from the union could hurt the country's incipient growth.

The past decade has been a roller coaster ride for Ireland. The country was once praised for the rapid economic growth it experienced between the late 1990s and early 2000s. With the start of the fiscal crisis in 2008, its status changed. Ireland transitioned from the promising "Celtic Tiger" to a member of the PIIGS — a notorious group of highly indebted and economically weak countries that also included Portugal, Italy, Greece and Spain.

As Ireland's banking and real estate bubbles of the early 2000s burst, Dublin made the controversial decision to rescue its own financial sector without external assistance. Shortly after that, the Irish government was forced to request a bailout from the European Union and International Monetary Fund. Ireland set out to reduce its budget deficit by enacting austerity measures, and the country endured five years of harsh spending cuts and tax hikes while unemployment rose and economic activity contracted.

Those years finally seem to be over. Ireland became Europe's fastest-growing economy in 2014, when its gross domestic product expanded by 4.8 percent, and it expects to see even more growth over the next two years. (According to European Commission predictions, Ireland's GDP will expand by 3.6 percent in 2015 and 3.5 percent the following year.) This trajectory would set Ireland up to grow twice as much as the eurozone as a whole; the same report predicts eurozone growth of a mere 1.5 and 1.9 percent over the same period.

According to Ireland's official statistics office, the country's unemployment rate fell to 9.8 percent in May from last year's 11.7 percent, one of the fastest improvements in the European Union. In addition, Ireland's average wage rose by 5 percent in 2014, and its domestic spending is slowly improving.

Austerity Policies Are Not Entirely Responsible

Because the Irish government was quick to enact budgetary cuts and tax hikes in response to the crisis, the European Union has tried to use Ireland as a poster child for austerity. Its economic recovery, some say, proves that Brussels' policies are effective at reversing economic decline. According to this view, the fact that the policies have worked in Ireland but not in Greece only reflects Dublin's greater commitment to reform.

While there is some truth to this argument, Ireland's crisis was substantially different from the situation in Greece. Before Ireland's banking and real estate bubbles burst, the country had already spent two decades building a real economy based on exports, foreign investment, pharmaceuticals, technology and agriculture. Because of its export-driven economy, Ireland was able to mitigate much of the impact austerity measures had on domestic demand by simply increasing its exports, while the country's low corporate tax rates continued to make it an attractive destination for foreign companies. Dublin suffered a "classic" banking crisis, and its fundamentally stable economy recovered relatively quickly. Greece, on the other hand, experienced more than a banking collapse — it suffered a structural crisis, and its entire economic model proved unviable.

Differences in pre-collapse economies aside, Ireland also had the advantage of securing access to outside help: first, the European Central Bank's promise of intervention on debt markets, then the introduction of quantitative easing. Together, these factors created enough stability to enable Dublin to borrow at record-low interest rates while at the same time making credit cheaper for Irish companies and households. On top of that, the decline in the value of the euro has made Ireland more competitive, and Ireland has benefited from the economic recovery of its main trade partner, the United Kingdom.

Social, Political and Economic Challenges Ahead

Despite the recent optimism, Ireland still faces challenges, not least of which is its substantial accumulation of public debt. As a result of Ireland's efforts to rescue its financial sector, its debt skyrocketed from 24 percent of GDP in 2007 to 123.2 percent in 2013. Private debt is also a source of concern: According to Eurostat, Ireland's private sector debt is at around 300 percent of GDP, the third-highest rate in the European Union. Rapid economic growth and weak inflation will help mitigate these problems, but debt will remain problematic for Ireland's government as well as its private households and corporations.

Ireland's recovery, while promising, has also been uneven. Dublin and its surrounding areas are growing faster than the rest of the country. While unemployment in eastern Ireland is below the national average, the jobless rate in the west is at around 12 percent. Many of Ireland's rural towns and villages are not feeling the effects of economic recovery at all.

Even if Ireland is able to spread its gains more equitably, mere economic improvement cannot fully address the social impact the crisis had on Ireland. The country was a magnet for immigration in the early 2000s, when the economy was growing rapidly and unemployment was low. But the crisis led to massive emigration, first by foreigners who had arrived during years of prosperity and then by Irish nationals. In the immediate term, the loss of some of its population actually helped Ireland reduce its unemployment problem somewhat; a smaller workforce meant fewer people competing for jobs. But in the long run, the loss of a large number of workers will create fiscal and labor problems for Ireland. The country will have to find ways to attract immigrants again to cover its employment needs and to alleviate the economic impact of its shrinking and aging population. Ireland's demographic profile is somewhat healthier than that of most European countries, but falling birthrates will still strain the country's health and pension system.

Dealing With Challenges to European Unity

As it confronts its domestic challenges, Ireland will also have to respond to political events taking place outside its borders. Greece's fiscal troubles are particularly salient for Irish politicians, since Greece's left-wing government is attempting to implement the kinds of expansionary policies that Ireland rejected in favor of austerity measures. For this reason, Dublin has been critical of Greek Prime Minister Alexis Tsipras' administration.

At the same time, negotiations between Athens, its creditors and the European Union have implications for Ireland's own relationship with the bloc. If Greece's push for debt relief is successful, Dublin will be under significant domestic pressure to request similar treatment, given its own debt challenges. And should negotiations collapse, the ripple effects of a disorderly Grexit would end the calm in financial markets and threaten Ireland's prospects for growth.

Closer to home, Britain is re-examining its own relationship with the European Union. Ireland's close economic ties with the United Kingdom mean it will actively work against a British exit from the union. Though Ireland has diversified its export markets since it joined the European Union in the early 1970s, the United Kingdom remains its most important export destination, receiving roughly 16 percent of Irish exports.

If the United Kingdom does choose to pull away from the eurozone, Ireland will attempt to at least secure its existing trade deals. The United Kingdom could leave the union but enter a free trade deal with the bloc similar to the European Union's deals with Norway or Iceland. But should the United Kingdom leave the union without a free trade agreement, the introduction of new tariffs on trade would harm the Irish economy immensely.

However, preventing a British exit from the union could prove challenging for Dublin. If the United Kingdom is unable to renegotiate the bloc's governing treaties, its departure will become more likely. And since EU treaties must be ratified by referendum, the Irish government would have to vote to approve those treaty changes. Depending on the new terms, and given Ireland's poor track record when it comes to ratifying treaties (it took two separate votes before the Irish ratified the Treaty of Nice in 2000), Irish politicians could have a hard time convincing voters to support a new treaty.

An Election Year

Times of economic stagnation are difficult, but times of recovery can be equally problematic. As its economy grows, Ireland will probably enter a new phase of spending increases and tax cuts, for both political and economic reasons. The country will hold general elections no later than April 2016, and both the government and the opposition are seeking votes by promising more generous public spending and benefits for different social groups.

The money for such programs has to come from somewhere, and it will not be from tax increases. Neither the center-right nor the center-left will dare propose new taxes at a time when the public favors lower taxes and higher spending, as demonstrated by recent popular resistance to a proposed tax on water.

The current and the future Irish government will be under pressure to increase salaries in the public sector and to restore spending in the country's damaged welfare system. The challenge will be to find a way to follow through on its promises to the Irish voters while also achieving a more balanced budget. In short, signs of recovery hint at a hopeful future ahead for the Emerald Isle. But a hope is not a promise; Ireland will have to find a way to maintain its newfound economic growth without repeating its past mistakes.