In 2002, Mercosur states and Mexico signed the Accord of Economic Complementation, which reduced tariffs on vehicles and auto parts in an effort to encourage automotive trade among the custom union's five members. For Mexico and Brazil, the deal was mutually beneficial because it allowed Mexico to concentrate on producing larger, higher-end vehicles, while Brazil focused on making smaller, less expensive cars. In the first seven years of the agreement's implementation, Brazil ran a trade surplus with Mexico in the automotive sector. But between 2010 and 2012, as incomes rose and Brazilians gained easier access to credit, Mexico's higher-end vehicles became more attractive to Brazilian consumers than their own country's lower-end models, thus producing a trade deficit.

In response to this deficit, Mexico City and Brasilia reached a deal in 2012 to limit the value of assembled vehicle exports from Mexico to Brazil to $1.55 billion per year until 2015. Once this provision expires on March 18, the free trade framework established under the original Accord of Economic Complementation will be reinstated.

In the current talks, the Mexican government is seeking an immediate return to free trade, but Brazilian leaders want to extend the restrictive automotive sector quota for up to five years. Their diverging interests underscore the differences in the two countries' economic policies: Mexico is aiming to open up its market amid a boom in car production, while Brazil is trying to protect its struggling auto industry amid the country's broader problems with industrial competitiveness.

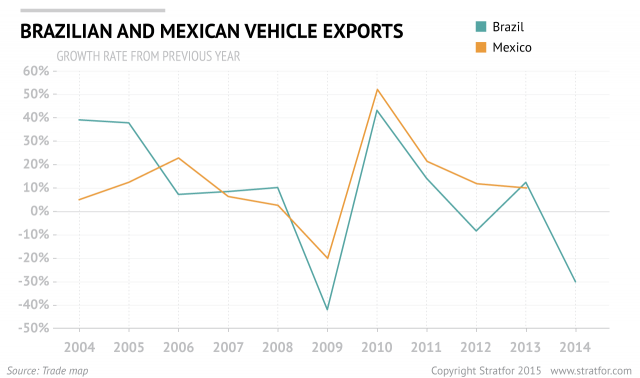

Mexico's automotive sector has a significant advantage over its Brazilian counterpart: the United States. Because Mexico is a signatory to the North American Free Trade Agreement, car manufacturers from countries that do not have a free trade agreement with the United States — Toyota, Mazda, BMW and Audi, to name a few — can skirt U.S. import tariffs on their vehicles by manufacturing them in Mexico. The Mexican automotive sector is thus angled toward its two northern export markets, the United States and Canada, rather than Mexican consumers. Brazil's auto industry, on the other hand, developed as international car manufacturers set up shop in the country to avoid its own protective import tariffs. As a result, Brazil's automotive industry is largely geared toward a domestic market, with exports accounting for only 15 percent of total production (the bulk of which go to Argentina, not the United States). The structural differences between the two countries' industries have led to dramatically different results: In the past year alone, Mexico's auto production rose nearly 10 percent to a record-high 3.22 million vehicles, while its exports rose 9.1 percent to reach a historic peak of 2.64 million vehicles. Meanwhile, Brazil's auto production dropped 15 percent to 3.15 million vehicles. The country's exports took an even bigger hit, falling by 30 percent in 2014.

Broader Economic Differences

The gap between the performance of Mexico's and Brazil's automotive sectors reflects the larger differences in the two countries' economic models that stem from their contrasting geopolitical imperatives. Because of its proximity to the United States and its location in the strategic Caribbean Basin, Mexico has opened its economy by signing dozens of free trade agreements over the past two decades. Through NAFTA, it has shifted toward a full integration with the U.S. economy. By contrast, Brazil — which maintains its economic core in the Southern Cone of South America — has adopted a more protectionist approach to safeguard its domestic industries and job markets. It has avoided large-scale economic integration with the United States.

The two countries' diverging economic paths extend beyond national policies. They also lead two distinct Latin American trade blocs — the Pacific Alliance and Mercosur — that have very different economic philosophies and trade policies. The Pacific Alliance, comprised of Mexico, Colombia, Peru and Chile, unites its member states in a free trade partnership and limits the role of individual governments in multilateral trade by lowering tariff barriers and harmonizing regulations. Mercosur, on the other hand, has been used by its member states (Brazil, Argentina, Uruguay, Paraguay and Venezuela) as a mechanism with which to periodically negotiate mutually beneficial trade arrangements while otherwise relying on heavy state intervention to shield members from outside competition.

The recent fall in global oil prices has hurt both Mexico and Brazil economically, and a new automotive trade agreement would help mitigate the damage. Mexico's leaders may want a free trade agreement, but they understand that any deal is better than no deal at all, since Mexico's automotive industry relies heavily on exports. Brazil, for its part, has threatened to drop out of the trade agreement altogether if a quota system is not imposed to protect its domestic industry. Thus, although Mexico and Brazil will likely compromise, the inherent geopolitical constraints that both countries face will continue to block a full-scale free trade agreement for the foreseeable future.