On Feb. 4, Italian newspaper Il Messaggero reported that the Italian government would establish a so-called bad bank to absorb some of the non-performing loans in the country's banking sector. According to the newspaper, the European Central Bank was notified of the project and Italy would send a formal plan to Brussels once it had been completed. Later the same day, the Italian government said the plan Il Messaggero was referring to was no longer under consideration but that Rome was indeed studying ways to address unpaid loans. The statement confirmed comments made on several occasions by Italian Finance Minister Pier Carlo Padoan that his ministry was considering the creation of a bad bank.

According to Il Messaggero, Rome is considering two options for the bad bank's ownership structure. The first option would give the Italian state control of 49 percent of the institution; private investors would own 32 percent and banks would own 19 percent. The second option would exclude private investors, giving the state 81 percent of the institution and banks 19 percent.

The reports follow Italian Prime Minister Matteo Renzi's Feb. 3 announcement that he was ready for a confidence vote on his decree to reform the voting structure of cooperative banks, which are small and medium-sized savings banks closely tied to local governments. The decree was issued in late January and needs to be ratified by the Italian Parliament. It gives the 10 largest cooperative banks in Italy 18 months to become joint-stock companies and introduce a new voting system. The system would require shareholders to vote based on their percentage of ownership; currently each shareholder has one vote. This would make it easier for cooperatives to be sold to larger banks.

Why Now?

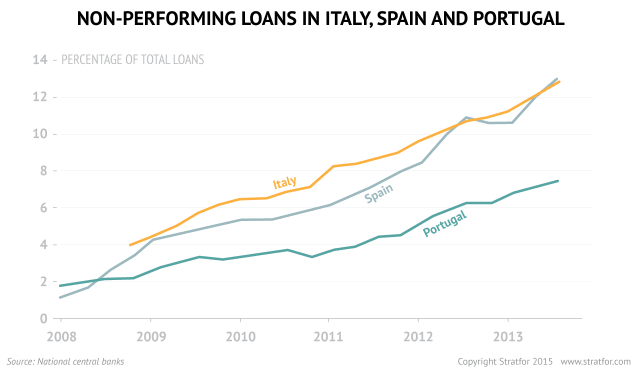

Because of the economic crisis, bad loans in Italian banks increased from 45 billion euros (about $51.5 billion) in 2006 to 181 billion euros in 2014. The asset quality review and the stress tests recently performed by the European Central Bank highlighted the vulnerability of the Italian banking sector, especially among cooperative banks.

Nine of the 25 banks shown to have capital shortfalls under the European Central Bank's review were in Italy, including Banca Monte dei Paschi di Siena and Banco Popolare, Italy's third- and fourth-biggest lenders. The Italian banking sector is oversized, both in terms of the number of players and the excessive number of branches and offices. Official EU data shows that Italy has 54 bank branches per 100,000 people, while the EU average is only 39 bank branches per 100,000 people.

The Italian government hopes that banks will be more willing to lend to households and businesses after risky loans are taken off their books. Banks hope that the creation of a bad bank will allow them to sell their bad loans at higher prices. Some banks have been selling bad loans to private investors at 10 to 15 percent of their original value. If Italy creates a bad bank similar to Spain's Sareb, the institution created to address Spain's banking problems, banks could benefit from better deals. Italy's largest banks, Intesa and Unicredit, have already sold packages of bad debt to private investors, but it is unclear whether these large banks would participate in a potential bad bank.

The Spanish Model

Spain sets a precedent for Italy: The Spanish government owns 45 percent of Sareb, while 27 private entities (including two of the largest banking groups in Spain, Santander and Caixa) own the remaining 55 percent. BBVA decided not to participate. The key difference here is that Sareb was partially created with EU money as part of Spain's 2012 bailout, which came with strings attached. It would be difficult for the Italian government to receive EU money without a formal agreement, which would involve demands for economic reform.

According to rumors in the Italian press, the new bad bank would have initial capital of 3 billion euros. Italy could try to finance the bad bank with its own money, but Rome would ultimately need to reach an agreement with the European Union. Creating a bad bank would involve more spending at a time when Rome is under pressure to keep its deficit under control. Rome and Brussels would need to agree on a mechanism to exempt the amount spent for the creation of the bad bank from Italy's deficit calculation. In January, La Repubblica newspaper reported that Rome was considering a plan to pack bad loans into state-guaranteed asset-backed securities to sell them to the European Central Bank as part of its repurchasing program.

In Spain's case, the results of the bad bank were mixed. In January, the Bank of Spain announced that non-performing loans fell for the third month in a row in November, accounting for 12.7 percent of all loans. The figure is lower than the historical record of 13.6 percent registered in December 2013 but still quite high for a developed economy.

Spain's banking sector was significantly consolidated, resulting in a dramatic reduction in the number of financial entities. Spanish banks performed well in the 2014 stress tests; of the 15 Spanish banks examined by the European Central Bank, only one, the small lender Liberbank, was shown to have capital deficit. Bankia, which was at the heart of the Spanish banking crisis and required half of Spain's 41 billion-euro bailout, became profitable again in 2013 after cutting staff and selling assets. Despite a spate of legal problems, the bank is no longer considered a threat to the country's financial sector. However, credit conditions in Spain remain tight. The Bank of Spain recently reported that credit to households and companies fell in 2014 for the sixth year in a row. Spain faces dual challenges: Banks are not lending, but households and companies are not borrowing either.

Italy faces similar challenges. The status of the economy remains a key factor in the profitability of banks, and credit is intimately related to the economic cycle. Reports show that credit to small and medium-sized companies has fallen steadily since 2010, a pattern that is seriously undermining the chances for economic recovery. The Italian economy has been in and out of recession since the beginning of the crisis, and only tepid growth is expected for this year. As long as Italy does not see substantial improvements in employment and a recovery of economic activity, credit conditions will not significantly improve.